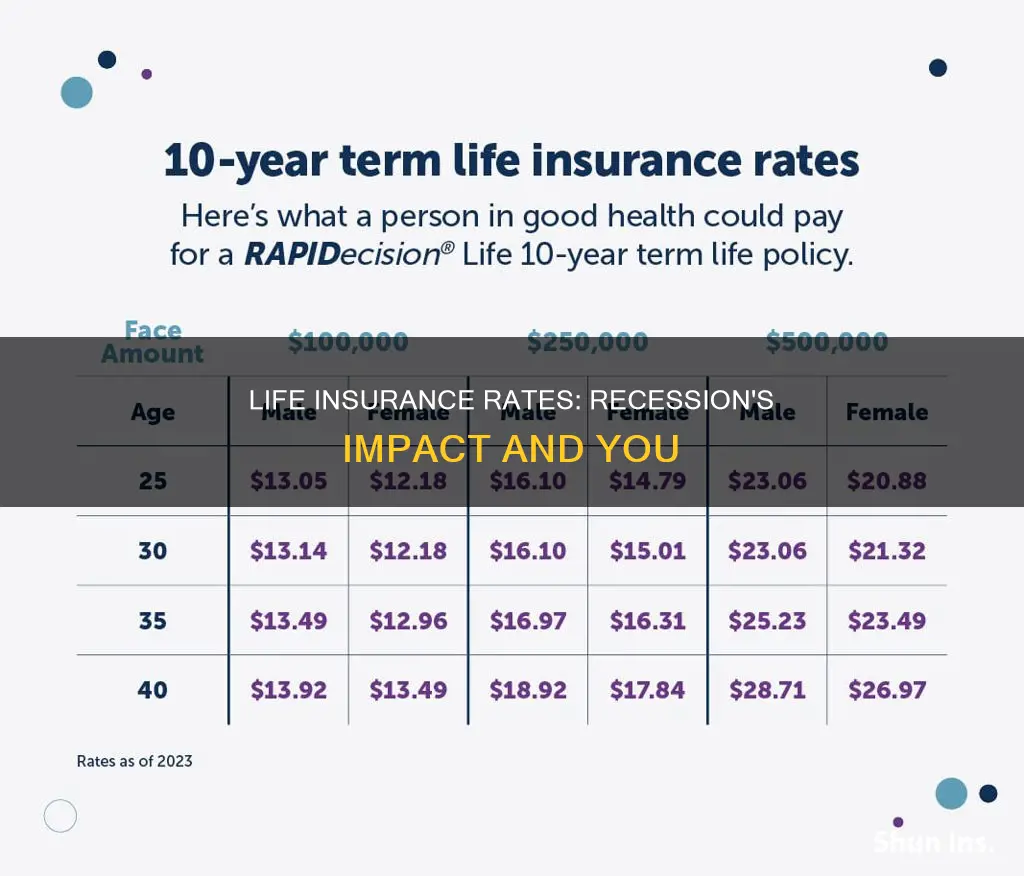

Life insurance is a crucial financial safety net for families, especially during a recession. But do life insurance rates drop during a recession? The short answer is no. While life insurance companies are not significantly impacted by market volatility, they may incrementally increase rates on permanent policies for new business if a recession lasts longer than expected. However, these changes are expected to be minimal, and factors like age and health history play a more significant role in determining rates. Term life insurance rates tend to remain stable even during financial crises due to their shorter coverage periods. In contrast, whole life insurance rates may be higher if purchased during economic instability, as they are tied to the previous year's performance. Ultimately, life insurance is essential during a recession to protect your loved ones financially.

| Characteristics | Values |

|---|---|

| Are life insurance rates impacted by a recession? | No, life insurance companies are not greatly impacted by market volatility. |

| What about long-term economic volatility? | Short-term economic volatility doesn't affect life insurance policy rates. If a recession lasts longer, life insurance companies might increase rates to maintain profitability. |

| What about term life insurance? | Term life insurance rates tend to remain stable even during periods of financial crisis. |

| What about whole life insurance? | Whole life insurance rates may be higher if purchased during a time of economic instability. |

| What about existing whole life insurance policies? | Whole life insurance rates won't change for existing policyholders. |

Explore related products

What You'll Learn

![]()

Term life insurance rates remain stable during a recession

Term life insurance rates tend to remain stable during a recession. This is because term life insurance policies cover individuals for a short period of time, usually 10, 15, 20 or 30 years, depending on the coverage chosen. Permanent policies, on the other hand, last a lifetime.

These shorter term lengths protect both the consumer and the life insurance company from economic fluctuations. Term life insurance policies are less impacted by low-interest-rate environments than permanent life insurance policies. This is because permanent life insurance policies offer long-term cash value guarantees, which can be costly for insurance companies in a low-interest-rate environment.

Since term life insurance policies provide coverage for a defined period, the insurer isn't taking on as much risk of losing money if the economy declines in the long term. This means that insurance companies are comfortable offering affordable term life insurance policies during recessions and when people are unemployed.

Term life insurance is also less affected by economic fluctuations because it does not accumulate cash value over time. Whole life insurance, a type of permanent life insurance, accumulates interest over time, and the premiums may be higher if you purchase the policy during a time of economic instability.

When you buy level premium term life insurance, you lock in your premium rate for the length of the term. This is called a "guaranteed level premium". For example, if you buy a 10-year term life insurance policy, you pay the same monthly premium for the full 10 years, no matter what happens to the economy during that period.

Term life insurance is designed to fit into nearly every budget and provide peace of mind that your premiums won't increase due to economic issues. It is a good idea to purchase term life insurance early, when you are young and healthy, to secure the lowest possible monthly premium.

Life Insurance with an ICD: Is It Possible?

You may want to see also

Explore related products

![]()

Whole life insurance rates may increase during a recession

Whole life insurance, a type of permanent life insurance, covers you for your entire life. The policy accumulates interest over time and the premiums remain constant. However, if you purchase a whole life insurance policy during a recession, you may face higher premiums as these rates are determined by the previous year's performance.

When a recession hits, the economy suffers. This includes higher unemployment, inflation, and business failure. With the prices of many goods and services rising, life insurance rates may also be impacted.

There are two main types of life insurance: term and whole life. Term life insurance offers coverage for a set number of years, after which the policy expires and must be renewed. This type of insurance holds no cash value.

On the other hand, whole life insurance lasts your entire life. While the premiums will remain constant, they may be higher if purchased during a recession or period of economic instability. This is because whole life insurance rates are determined by the previous year's performance.

When a recession lasts longer than expected, insurers can incrementally increase rates on permanent policies for new business. However, these changes are usually minimal, and factors like health history and age play a larger role in determining rates. It's important to note that if you already have whole life insurance, your rates are locked in and will not change.

Genetic Testing: Insurance Coverage and Life Insurance Applications

You may want to see also

Explore related products

![]()

Life insurance is one of the most recession-proof industries

During a recession, insurance companies may experience a decline in premium collections as clients cut back on expenses. However, this does not seem to affect the life insurance sector as much as other types of insurance. This is likely because life insurance is seen as a more essential form of protection. While someone might consider car or home insurance to be a luxury they can go without, life insurance is often viewed as a necessity to ensure financial security for their family.

Life insurance provides a financial safety net, helping loved ones cover funeral costs, pay off debts, and maintain their standard of living in the event of the policyholder's death. This becomes even more important during a recession when household incomes may be lower and budgets are tighter. An affordable term life insurance policy can be a great way to protect your dependents during an economic downturn.

While short-term economic volatility typically does not affect life insurance policy rates, if a recession is prolonged, life insurance companies may incrementally increase rates on permanent policies for new business. However, these changes are usually minimal, and factors like health history and age play a much larger role in determining rates.

In summary, life insurance is a crucial form of protection, especially during economic downturns when financial security is more vulnerable. Its recession-proof nature makes it a stable industry, even during times of market fluctuation.

Life Insurance and Motorcycle Accidents: What's Covered?

You may want to see also

Explore related products

![]()

Life insurance provides a financial safety net

Life insurance is a crucial financial safety net for your loved ones, providing much-needed financial security in the event of your death. This becomes even more important during a recession when budgets are tight and job losses are common. Here's how life insurance acts as a financial safety net:

Funeral Expenses

Life insurance can help cover the cost of your funeral, ensuring your loved ones don't have to worry about finances during their time of grief.

Paying Off Debts and Bills

Life insurance can be used to pay off any outstanding debts and bills, such as credit card debt or student loans. This is especially important during a recession when job losses and reduced incomes may lead to higher debt.

Living Expenses

Life insurance can help your family continue to pay their living expenses, including rent or mortgage payments. This is crucial when household incomes may be lower during a recession.

Stock Market Volatility

Life insurance provides a guaranteed payout that isn't affected by stock market fluctuations. This can be reassuring during a bear market when investment portfolios and retirement funds may be at risk.

Peace of Mind

Life is unpredictable, and a recession can make the future seem even more uncertain. Life insurance offers peace of mind, knowing that your loved ones will be financially protected no matter what happens.

While life insurance rates may not be significantly impacted by a recession, especially for term life insurance policies, it's still important to consider the financial stability of the insurance company before purchasing a policy. By securing a life insurance policy, you can ensure your loved ones have the financial support they need, even during challenging economic times.

Using Child Life Insurance for Your Dog: Is It Legal?

You may want to see also

Explore related products

![]()

Life insurance can help cover the gap if the stock market drops

Life insurance is a valuable tool to protect your family's financial security, especially during a recession. While the stock market can be volatile and unpredictable, life insurance provides a safety net that can cover the gap if the stock market drops. Here's how life insurance can help:

Financial Protection

Life insurance offers financial protection for your loved ones in the event of your untimely death. This support is crucial during economic downturns when budgets are tight and unemployment is high. It can help cover funeral costs, pay off debts, and maintain living expenses for your dependents.

Peace of Mind

The stock market's unpredictability can be concerning for investors, but life insurance provides peace of mind. With a life insurance policy, you know that your beneficiaries will receive a payout, regardless of the performance of your investments or retirement accounts. This assurance can help ease worries during market downturns.

Stability in Uncertain Times

Recessions can bring uncertainty and instability, but life insurance offers stability by providing a guaranteed payout. This stability is especially important if you have dependents who rely on your income. By maintaining your life insurance policy, you ensure that your loved ones will have financial support even if your investments take a hit during a bear market.

Protection Against Debt

During a recession, many people may turn to credit cards or loans to cover everyday expenses. Life insurance can help cover these debts in the worst-case scenario. It can pay off credit card debts, student loans, or any other financial obligations you may leave behind.

Long-Term Financial Security

While the stock market fluctuates, life insurance provides long-term financial security. With a term life insurance policy, you lock in a premium rate for the duration of the term, which could be 10, 15, 20, or even 30 years. This means that even if the stock market drops, your life insurance coverage remains unchanged, providing a consistent level of financial protection for your family.

In summary, life insurance is an essential tool to protect your family's financial well-being, especially during uncertain economic times. It can help cover the gap if the stock market drops, providing peace of mind and financial stability for your loved ones.

Child Life Insurance: Voluntary Protection for Your Children

You may want to see also

Frequently asked questions

Life insurance rates are not significantly impacted by short-term economic volatility. However, if a recession lasts longer than expected, insurers may incrementally increase rates on permanent policies for new business, but these changes are usually minimal.

There are two main types of life insurance: term and whole. Term life insurance covers individuals for a set number of years, while whole life insurance is a type of permanent life insurance that lasts your entire life. Whole life insurance premiums may be higher if purchased during economic instability, as these rates are determined by the previous year's performance.

Yes, life insurance is just as important, if not more, during a recession. It provides a financial safety net for your loved ones, helping them cover funeral costs, pay off debts, and maintain their standard of living.

During a recession, there is a higher risk of job loss and increased financial uncertainty. Life insurance can help cover living expenses, pay off debts, and provide financial security despite stock market fluctuations. It is a way to protect your loved ones from financial hardships if something happens to you.