Unlike other types of loans, Federal Housing Administration (FHA) loans require borrowers to pay a mortgage insurance premium (MIP) to secure the mortgage loan. This insurance premium is paid to the FHA and is required for all FHA loans. It is an additional payment that provides the mortgage lender with protection in the event that the borrower defaults on their loan. FHA loans are a good option for homebuyers who have not saved much for their down payments. However, it is important to note that FHA loans have a maximum loan amount that it will insure, known as the FHA lending limit. This limit is calculated based on the median house prices in each county and typically increases annually.

| Characteristics | Values |

|---|---|

| FHA loan insurance name | Mortgage Insurance Premium (MIP) |

| Who it protects | Lender |

| When it is paid | Upfront and annually |

| Upfront payment | 1.75% of the total loan value |

| Annual payment | Based on loan amount, length of loan, and down payment |

| Loan amount | Maximum amount is the FHA lending limit |

| Down payment | As low as 3.5% |

| Credit score | As low as 500 |

| Getting out of MIP | Refinancing |

Explore related products

$0.99 $15.99

What You'll Learn

![]()

FHA mortgage insurance requirements

FHA loans are a great option for homebuyers who have not saved much for their down payments. They are also a good option for first-time homebuyers. However, FHA loans require mortgage insurance, which is a significant drawback to an otherwise generous loan. This insurance is to protect FHA-approved lenders against losses if you default on your mortgage payments.

There are two types of FHA loan insurance payable on an FHA loan: the upfront mortgage insurance premium (UFMIP) and the annual mortgage insurance premium (MIP). The upfront premium is typically paid at closing and is 1.75% of your loan amount. It can be financed into your mortgage amount or paid in full in cash. The annual premium is charged based on factors such as your loan amount, the size of your down payment, and the loan term. This premium is then divided by 12 and charged in monthly installments added to your monthly mortgage payment.

FHA mortgage insurance is generally more expensive than private mortgage insurance (PMI) on a conventional loan, and it's required regardless of your down payment amount. It is also for the life of the loan. The only way to get out of paying FHA mortgage insurance is to refinance into a different type of loan, such as a conventional or VA loan.

It is important to note that FHA mortgage insurance does not protect the borrower but instead protects the lender against default. If a borrower defaults on an FHA loan, the Federal Housing Administration (FHA) will compensate the lender for the outstanding balance.

Unraveling the Benefits of Bundling with Farmers Insurance

You may want to see also

Explore related products

![FHA Multi-Family Housing Mortgage Insurance Program... Hearing... S. Hrg. 107-534... Committee On Banking, Housing, & Urban Affairs, United States Senate... 107th Congress, 1st Session [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

![]()

FHA loan refinancing

FHA loans are a type of mortgage loan backed by the Federal Housing Administration. They are a good option for homebuyers who have not saved much for their down payments, as well as those with a higher debt-to-income ratio and lower credit scores. FHA loans require mortgage insurance, which is typically 0.55% of the loan amount and is paid for the life of the loan. This insurance protects lenders against losses that may result from defaults on home mortgages.

If you have an FHA loan and want to get out of paying mortgage insurance, refinancing is your only option. However, refinancing may not always be financially beneficial, as it may result in higher interest rates. It is important to carefully consider the costs and benefits before deciding to refinance.

There are several FHA loan refinance options available, including the FHA Simple Refinance and the FHA Streamline Refinance. The FHA Simple Refinance allows homeowners to lower their interest rates, switch from an adjustable-rate mortgage to a fixed-rate loan, and remove a co-borrower from the mortgage. To qualify, a credit score of 580 is typically required. The FHA Streamline Refinance is similar but may not require an appraisal or an in-depth credit report, resulting in a quicker process. To qualify for this option, you must have an existing FHA loan with no outstanding monthly payments and meet specific conditions regarding the timing and frequency of your mortgage payments.

In addition to the FHA Simple and Streamline Refinance options, there is also the Cash-Out Refinance. This option allows homeowners to refinance their existing mortgage by taking out another mortgage for more than they currently owe. To be eligible, borrowers typically need at least 20% equity in the property, as determined by an appraisal. A Cash-Out Refinance can be useful for various purposes, such as home improvement, college tuition, or debt consolidation.

When to Report Scratches to Your Auto Insurance Company

You may want to see also

Explore related products

![]()

FHA loan MIP costs

FHA loans are a good option for homebuyers who have not saved much for their down payments. However, a key drawback of FHA loans is that they require you to pay mortgage insurance in the form of Mortgage Insurance Premiums (MIP). MIP protects the lender if you default on the loan.

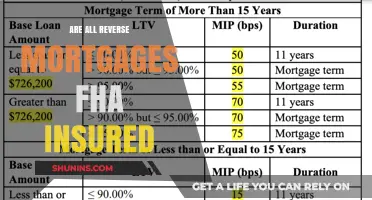

The upfront MIP payment is typically due when you close on your FHA loan, although it can be added to the balance of the loan. This upfront payment is only due once unless you refinance or take on another FHA loan in the future. The upfront MIP cost totals 1.75% of the loan amount. You can pay this premium all at once at closing or add it to your mortgage and pay it over time, although you will pay interest on this cost if you choose the latter option.

The annual MIP costs will vary depending on the size, term, and loan-to-value (LTV) ratio of the loan. The larger your down payment, the lower your MIP costs will be. With a 10% or larger down payment on an FHA loan, you’ll pay MIP for the first 11 years. With less than 10%, MIP lasts the entire loan term. Most lenders add MIP to your monthly mortgage payment.

The monthly MIP cost goes down every year as it is calculated as a percentage of the average outstanding balance for the year. As you pay down the principal of the loan, the balance drops and so do your MI costs.

Reporting Crashes: When to Inform Your Insurance Company

You may want to see also

Explore related products

![]()

FHA loan vs. conventional loan

FHA loans are government-backed home loans insured by the Federal Housing Administration. They are designed to make it easier for borrowers to qualify for a loan, even if they have a low credit score or are unable to save for a down payment. FHA loans have less-restrictive qualifications, with a minimum credit score of 580 required to be eligible for a 3.5% down payment. If your credit score is between 500 and 579, you may still qualify for an FHA loan, but you will need to make a 10% down payment.

FHA loans are a good option for first-time homebuyers, as they allow for third-party funds, or "gift money", to be used for the down payment. This money can come from a friend, employer, or charity, as long as it is a true gift with no expectation of repayment. FHA loans also do not require a home inspection, only an appraisal.

However, one of the drawbacks of FHA loans is that they require mortgage insurance, which is usually for the life of the loan. This insurance protects lenders against losses that result from defaults on home mortgages. The mortgage insurance for an FHA loan with a 3.5% down payment is typically 0.55% of the loan amount.

Conventional loans, on the other hand, are home loans offered by private lenders without any direct government backing. They are not insured by a federal agency, so the lender assumes the risk associated with issuing the loan. Conventional loans typically require a higher credit score, a lower debt-to-income (DTI) ratio, and a higher down payment than FHA loans. While some conventional loans require a 20% down payment, others can offer a lower down payment of 3%.

Another difference between FHA and conventional loans is the appraisal process. FHA loans require an appraisal, which is generally more onerous than conventional appraisals in terms of safety and soundness issues with the dwelling. Some conventional loans may only require an Automated Valuation Model (AVM) to suffice.

In terms of interest rates, FHA loans typically have higher interest rates than conventional loans. However, it's important to note that interest rates for both loan types can vary based on market conditions and the borrower's credit score.

Finally, when it comes to refinancing, FHA loans may offer more flexibility. Some refinance loans are designed specifically to help FHA borrowers get a better deal or avoid hurting their credit scores due to missed payments. With conventional loans, you may be stuck with the original loan type even if you refinance.

In conclusion, both FHA and conventional loans have their advantages and drawbacks. FHA loans are generally more accessible to borrowers with lower credit scores or those who struggle with down payments, while conventional loans may offer better terms for borrowers with higher credit scores and more substantial down payments. The best option for each borrower will depend on their individual financial situation and needs.

Carport Coverage: Attached to House?

You may want to see also

Explore related products

![]()

FHA loan eligibility

FHA loans are backed by the Federal Housing Administration, an agency under the US Department of Housing and Urban Development (HUD). FHA loans are insured by the FHA, which means that the owners of your mortgage are protected against loss if you default on your loan. FHA loans are a good option for homebuyers who have not saved much for their down payments or have a lower credit score.

FHA loans have a minimum credit score requirement of 500, but borrowers with a credit score of 500–579 may still qualify for an FHA loan with a 10% down payment. Many lenders have their own minimum credit score requirements, with Rocket Mortgage® requiring a minimum score of 580 for FHA loans. A good track record of timely payments will likely make you eligible for an FHA loan.

FHA loans also have a maximum loan amount that they will insure, known as the FHA lending limit. These limits are calculated based on the median house prices in each county and increase annually for many counties in the United States. The minimum FHA 203(k) loan balance is $5,000, and any home repairs or improvements must be concluded within 6 months to stay within the loan terms.

FHA loans require mortgage insurance, which is based on the loan balance at the beginning of each 12-month period following the closing of the loan. The insurance is calculated as 0.55% of the loan amount. This insurance is for the life of the loan unless you refinance, in which case it may be eliminated.

Ikon Pass Insurance: Worth the Cost?

You may want to see also

Frequently asked questions

Yes, FHA loans require borrowers to pay a mortgage insurance premium (MIP). This is an additional payment made to secure the mortgage loan.

The upfront MIP payment is 1.75% of the total value of your loan, due when you close on your FHA loan. Alternatively, it can be added to the balance of the loan. There is also an additional annual payment, the cost of which depends on your loan amount.

FHA mortgage insurance lowers the risk to the lender, meaning they can offer loans to borrowers who might not otherwise qualify. It also means that lenders will not require as large a down payment as they would without it.