In the United States, car insurance is required to drive legally. The type of coverage you need is defined by the state you live in and whether you are financing your vehicle. Liability insurance is required in all states except Virginia and remote areas of Alaska. This covers damage to others' property and injuries caused by an at-fault accident. Collision and comprehensive coverage are also recommended to protect your vehicle. When purchasing a new car, dealerships will not let you drive it off the lot without insurance. If you already have car insurance, you can update your policy to cover your new car, but your rates will likely change.

| Characteristics | Values |

|---|---|

| Required Documents | Driver's license, Vehicle Identification Number (VIN), Vehicle registration, Vehicle make, model, and year, Vehicle value, Miles driven per year, Name, Address, Date of birth, Gender, Marital status, Social Insurance Number |

| Optional Documents | Current insurance company and policy number, Traffic violations within the last 3 years, Previous claims filed in the last 8 years |

| When to Insure | Immediately after purchase |

| Exceptions | Virginia, remote parts of Alaska, vehicles that are not operable |

Explore related products

What You'll Learn

![]()

What documents do you need to insure a car?

The documents you need to insure a car vary depending on your location and the type of insurance you're seeking. Here is a list of documents you may need:

- Personal information: This includes your full name, permanent home address, and driver's license number. If you have a provisional or temporary license, some insurance companies can still cover you. However, most companies require a valid driver's license.

- Vehicle information: You'll need to provide details about the car you're insuring, such as the registration number, year of first registration, fuel type, modifications, Vehicle Identification Number (VIN), chassis manufacturer (for motorhomes), engine size, and physical condition.

- Proof of ownership or registration: While you don't always need to be the owner of the vehicle to insure it, you may be asked to provide proof of ownership or registration. This can be done through a V5C or 'log book' in the UK, which proves you are the registered keeper of the vehicle.

- Financial information: To purchase a car insurance policy, you'll typically need to provide a credit card number or banking information for the initial payment. If you plan to pay monthly, you may also need to set up a direct debit and provide additional details such as your bank name, account number, and sort code.

- Driving history and claims: Insurance companies will want to know about your driving record, including any traffic violations, accidents, and previous insurance claims. Be prepared to disclose any driving infractions and provide details of previous accidents.

- Social Security Number (SSN): In some countries like the US, you may need to provide your SSN to obtain car insurance.

- Other documents: Depending on your situation, you may also need to provide copies of report cards, membership cards, military ID cards, marriage certificates, divorce papers, and proof of any discounts you're eligible for (e.g., good student discount, military discount).

It's important to note that requirements may vary by insurer and policy type (e.g., temporary vs. annual insurance). Always review the specific documentation requirements provided by your chosen insurance company.

Police Cars: Insured?

You may want to see also

Explore related products

![]()

When do you need to buy insurance for a new car?

When buying a new car, you'll need to get insurance for it as soon as possible. Most dealerships require proof of insurance before you can drive the car out of the lot. If you already have insurance for another vehicle, you may be covered by a grace period, which usually lasts seven to 30 days. However, it's a good idea to contact your insurance company before buying your new car, as your premium will probably increase.

If you don't already have car insurance, you'll need to get a policy before you can drive your new car. You'll need to know the make and model of your new car, as well as the vehicle identification number (VIN), to get a quote. You can then compare quotes from different insurance companies to find the best rate. Once you've chosen a provider, you can purchase your policy, and you'll be ready to drive your new car home.

If you're buying a vehicle from a private seller, they usually won't request proof of insurance before you take possession of the car. However, it's important to remember that driving without insurance is illegal and can result in legal fees and other costly consequences if you're in an accident.

Gap Insurance: Vehicle Protection

You may want to see also

Explore related products

![]()

How much is new car insurance?

The cost of new car insurance depends on a variety of factors, including the driver's age, gender, location, driving record, credit score, and the make and model of the vehicle. It is important to note that insurance rates vary across different states and insurance companies. Here is a breakdown of the factors that influence the cost of new car insurance and some examples of insurance costs:

Age and Gender:

In many states, age and gender significantly impact car insurance costs. Younger drivers, especially those in the 16 to 29 age bracket, often face higher premiums due to their lack of driving experience. For example, in California, a 16-year-old male driver added to a family policy can expect an average annual cost of $3,772. The cost increases to around $4,458 annually if the 16-year-old opts for an individual policy.

Location:

Your location can significantly affect your insurance premiums. Insurance rates tend to be higher in densely populated urban areas with higher traffic density and increased risk of accidents, theft, and vandalism. For instance, in New Jersey, the average full coverage rate in Jersey City is $1,873, while in Newark, it jumps to $2,145.

Driving Record:

A clean driving record can help you secure more affordable premiums. On the other hand, accidents, speeding tickets, and violations like DUIs will typically increase your insurance rates. For example, in New Jersey, the average annual cost of car insurance with a clean record is $1,680. With a ticket, the cost increases to $1,831 per year, and with a DUI, it jumps to $2,997 per year.

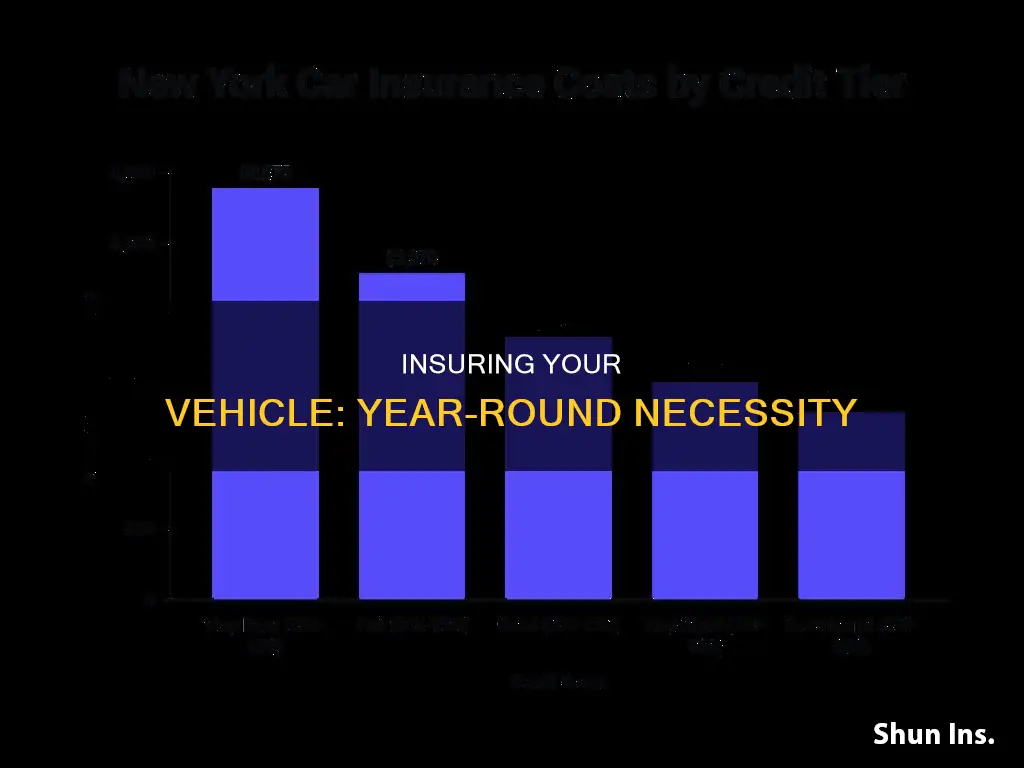

Credit Score:

In most states, insurance companies consider your credit score when determining your insurance rates. Generally, a higher credit score can lead to lower premiums, while a lower credit score may result in higher costs. In New Jersey, the average monthly premium for drivers with excellent credit is $90, while those with poor credit pay around $213 per month.

Vehicle Type:

The make, model, and age of your vehicle play a role in determining insurance rates. Newer cars with modern technology and higher values tend to be more expensive to insure than older models. Additionally, high-performance or luxury vehicles often cost more to insure.

Insurance Company and Coverage Level:

Insurance rates can vary significantly between different companies, even within the same state. It is essential to shop around and compare quotes from multiple insurers to find the most affordable option for your needs. The level of coverage you choose will also impact your premium. Minimum coverage will be the most affordable option, while full coverage, which includes comprehensive and collision insurance, will cost more.

- In California, the average monthly cost for state minimum coverage is $48, while the average cost for full coverage is $114.

- In New Jersey, the average monthly cost for state minimum coverage is $80, and the average cost for full coverage is $140.

Additionally, specific insurance companies may offer discounts for various factors, such as bundling policies, having multiple cars under one policy, maintaining a clean driving record, or paying your annual or six-month premium in a lump sum.

Insurance Total Loss: What's Next?

You may want to see also

Explore related products

![]()

What insurance do you need when buying a new car?

When buying a new car, you will need to insure it immediately. Dealerships will not let you drive your new car off the lot without insurance. If you already have car insurance, you can update your policy to cover your new car, but your rates will probably change. If you don't already have car insurance, you'll need to get a policy before you can drive your new car.

Types of Insurance Coverage

The type of insurance you need will depend on the requirements of the state in which you live. Some states require a personal injury protection policy and uninsured motorist coverage. You will need to insure your car for at least the minimum liability coverage mandated by your state. Liability insurance covers injuries or damage to others' property after an accident you cause, up to your policy's limits.

If you are financing your new car, your lender will likely require you to have full coverage car insurance. Full coverage includes your state's minimum requirements, plus comprehensive insurance and collision insurance. Comprehensive insurance covers damage to your car from things like fire, hail, vandalism and theft. Collision insurance pays for damage to your car from crashes with objects or other vehicles.

Gap insurance is also recommended, especially if you are financing your car. Gap insurance covers the difference between the remaining balance of your car loan and the current market value of your car if it's totaled or stolen.

Getting Insurance for a New Car

If you don't have car insurance, you'll need to get a policy before you can drive your new car. You can get a car insurance policy before you buy a car, as long as you know the make and model of your future vehicle. You will need the vehicle identification number (VIN), mileage, and your driving record. You can then compare insurance quotes and submit an application. Once you have proof of insurance, you can purchase your vehicle.

Vehicle Registration: Insurance or Not?

You may want to see also

Explore related products

![]()

How can you save on new car insurance?

When it comes to saving money on car insurance, there are several strategies you can employ. Here are some detailed tips to help you save on new car insurance:

- Shop around for insurance providers: Prices differ from company to company, so it's worth getting quotes from multiple insurers. Compare at least three quotes from different types of insurance companies, such as those that sell directly or through independent agents. Ask friends and family for recommendations, and research the company before committing. Remember, the lowest price doesn't always mean it's the best option; consider the company's reputation and the quality of their customer service.

- Compare insurance costs before buying a car: Auto insurance premiums are based on factors like the car's price, repair costs, safety record, and theft likelihood. Research the insurance costs for different vehicles before purchasing. Safe and moderately priced vehicles, such as small SUVs, tend to be cheaper to insure than expensive or flashy cars.

- Raise your deductible: Opting for a higher deductible can significantly lower your premium costs. Just ensure you have enough money set aside to pay the higher deductible if you need to make a claim.

- Reduce optional insurance on older cars: If your older car is worth less than ten times the insurance premium, consider dropping collision or comprehensive coverage. Evaluate whether the insurance payout would be worth more than the car's value in the event of a claim.

- Bundle your insurance policies: Many insurers offer discounts if you purchase multiple types of insurance from them, such as homeowners and auto insurance, or if you insure more than one vehicle. However, always compare costs with other companies to ensure you're getting the best deal.

- Maintain a good credit history: Establishing solid credit has numerous benefits, including lower insurance costs. Many insurers use credit information to determine auto insurance policies, as research shows that people who manage their credit effectively tend to make fewer claims. Regularly check your credit record to ensure its accuracy.

- Take advantage of low-mileage discounts: Some insurance companies offer discounts for motorists who drive less than the average number of miles per year or those who carpool to work. If your driving habits fit this profile, be sure to inquire about these discounts.

- Ask about group insurance: Some companies provide reduced rates for drivers who obtain insurance through group plans from their employers, professional associations, alumni groups, or other affiliations. Check with your affiliated organizations to see if they offer any insurance benefits.

- Seek out other discounts: There are various other discounts that insurers may offer. For example, some companies provide discounts for accident-free driving records, taking a defensive driving course, or having a young driver on your policy who is a good student or away at college without a car. Ask your insurer about any potential discounts you may qualify for.

- Choose an easily insurable vehicle: When buying a new car, consider its insurability. Some vehicles may be more challenging or costly to insure due to factors such as high theft records, limited availability of replacement parts, or high repair costs. Research the insurability of the vehicle before making a purchase.

- Keep your driving record clean: A clean driving record without traffic violations or accidents can help you obtain lower insurance rates. Safe driving habits not only keep you and others safe on the road but can also result in insurance savings.

- Inquire about available discounts with your insurer: Different insurers offer various discounts. Ask your insurance agent or consult their website to learn about the specific discounts they provide. For example, they may offer discounts for safety or anti-theft features in your vehicle, paperless billing, or paying your premium in full.

- Consider local and regional insurance companies: While large national insurance companies dominate the market, local and regional insurers often excel in customer satisfaction ratings and may offer lower insurance rates. Don't overlook these smaller companies when shopping for insurance.

Renew Vehicle Insurance: A Quick Guide

You may want to see also

Frequently asked questions

Yes, you need to insure a vehicle all year. Most states require you to carry liability insurance on each car you drive, regardless of how often the vehicle is on the road.

If your car is not operable, you might not have to insure it. Check with your state's department of motor vehicles.

If you don't drive your car often, it won't cost you much to insure it. Most car insurance companies offer multi-car discounts and base their rates on factors like how many miles you drive each car annually.

If you have multiple cars, you can minimize your car insurance premiums by shopping for the best rates, ensuring you get all the discounts you're entitled to, and carrying a higher deductible on the oldest car.

If you're buying a new car, you'll need to get a new car insurance policy to go with it. You can get a car insurance policy before you buy a car as long as you know the make and model. If you already have a policy, you can update it to cover your new car, but your rates will probably change.