When it comes to gap insurance, there are several factors that come into play when determining its impact and relevance. While age and location can influence insurance rates, the effect varies depending on whether it is in the context of home insurance or car insurance. In the case of home insurance, the location of the house is a significant factor, as homes in riskier areas prone to environmental damage or crime tend to have higher insurance premiums. Additionally, the age of the house matters, as older homes may be costlier to fix due to older components that need to be replaced. On the other hand, for car insurance, age and location can impact the cost of gap insurance, which protects individuals from depreciation by covering the difference between the car's value and the loan amount owed. Factors such as age, driving record, and vehicle type can influence pricing, with insurers typically offering gap insurance for new vehicles.

| Characteristics | Values |

|---|---|

| Age | Older homes are costlier to fix and have older components that need replacing to comply with current codes. Older age can also impact car insurance rates. |

| Location | Houses in areas prone to environmental damage, crime, or with a high number of claims will pay higher prices on their premiums. Location can also impact car insurance rates. |

| Other Factors | Other factors that impact insurance rates include the home's age, your insurance history, and how long you've maintained continuous coverage. |

Explore related products

What You'll Learn

![]()

Age impacts the cost of gap insurance

Younger drivers, particularly those below 25 years of age, are often deemed to be in a higher-risk category by insurance companies. This perception results from the assumption that younger drivers have less experience on the road and are more prone to accidents or traffic violations. Consequently, younger drivers may face higher insurance rates for gap coverage.

On the other hand, older drivers may also experience age-related impacts on their gap insurance costs. Insurance providers may consider older drivers, especially those above the age of 65, to be in a potentially higher-risk group due to assumptions about age-related changes in vision, reflexes, and cognitive abilities. This perception can lead to higher gap insurance premiums for older individuals.

It is important to note that the specific impact of age on gap insurance costs can vary across different states and insurance providers. Some states and insurers may place more emphasis on age as a determining factor than others. Additionally, the impact of age on insurance rates may be influenced by other variables, such as an individual's driving record, the type of vehicle they own, and their insurance history.

To obtain the most accurate information about how age influences gap insurance costs for a specific individual, it is advisable to consult with insurance providers directly or utilize online tools that allow for personalized quotes based on age, location, and other pertinent factors. By doing so, individuals can gain a clearer understanding of the relationship between age and gap insurance rates and make informed decisions regarding their insurance choices.

Direct Auto Insurance and National General: Are They Synonymous?

You may want to see also

Explore related products

![]()

Location impacts the cost of gap insurance

For homeowners, location is a significant factor in insurance rates. Houses located in areas prone to natural disasters such as wildfires, hurricanes, or hail damage will have higher insurance premiums. Living in the city versus the country can also affect rates, as urban areas with higher crime rates or frequent insurance claims tend to have higher premiums. Additionally, proximity to emergency services like police and fire departments can impact rates.

Similarly, location influences the cost of auto insurance, including gap insurance. Insurance companies consider various factors, such as age, gender, driving record, and location when pricing car insurance. A person's location can indicate the likelihood of accidents, theft, or vandalism, impacting insurance rates.

The impact of location on insurance rates is evident in the variation of coverage and discounts offered by insurers across different states. For example, in the United States, AAA offers insurance in California, Nevada, and Utah, with coverages, costs, and discounts varying between these states.

Overall, location is a critical factor in determining insurance rates, and it can affect the cost of gap insurance. Insurers assess the risk associated with a particular location and adjust premiums accordingly, resulting in higher or lower rates depending on the area's perceived risk.

Drive Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Gap insurance covers theft or damage

Gap insurance is an optional auto insurance coverage that applies if your car is stolen or deemed a total loss. It covers theft or damage in the sense that it protects you from the financial gap between what you owe on your car loan and the amount paid out in a total loss settlement from an auto insurer. This gap arises because once you buy a car, its value starts to decrease, sometimes significantly. If your car is stolen or written off, standard vehicle insurance pays the depreciated value of your vehicle, not its value when you bought it. Gap insurance covers the difference between the remaining value of your vehicle loan or lease and your vehicle's actual cash value at the time of the incident.

Gap insurance does not cover engine failure or other repairs. It also does not cover injuries, death, or funeral costs. It only pays out after a total loss covered by your collision or comprehensive insurance. It is worth noting that gap insurance does not cover the costs of vehicle repairs or bodily injuries resulting from an accident. Additionally, it does not cover engine failure or other mechanical issues. Gap insurance is designed to protect you financially in the event of a total loss or theft of your vehicle.

Gap insurance is particularly useful if you have a long commute, as higher-than-average mileage may cause your car's value to drop. It is also useful if you made a small down payment or none at all, as you may owe more than your car's value. You can determine your car's current market value by checking a respected industry guide, such as the Kelley Blue Book. This will help you understand if the gap insurance coverage is worth it for your specific situation.

In summary, gap insurance can provide valuable financial protection if your car is stolen or deemed a total loss. It covers the difference between the depreciated value of your vehicle and the amount you still owe on your loan or lease. However, it is important to note that gap insurance does not cover all types of damages or repairs, and it is designed specifically for total loss or theft situations.

Apply for AAA Auto Insurance: Steps to Follow

You may want to see also

Explore related products

![]()

Gap insurance is optional

Gap insurance is an optional form of auto insurance coverage that applies if your car is stolen or deemed a total loss. It is not a requirement, and you can decide whether or not to purchase it based on your own personal circumstances.

Gap insurance is designed to cover the difference between the depreciated value of your car and the loan amount owed if your car is involved in an accident. If your car is financed or leased without a down payment, the amount borrowed may be more than the car's value. In the event of an accident that totals your car or it being stolen, standard car insurance will only pay up to the current value, which may be less than the outstanding loan or lease amount. This is known as negative equity.

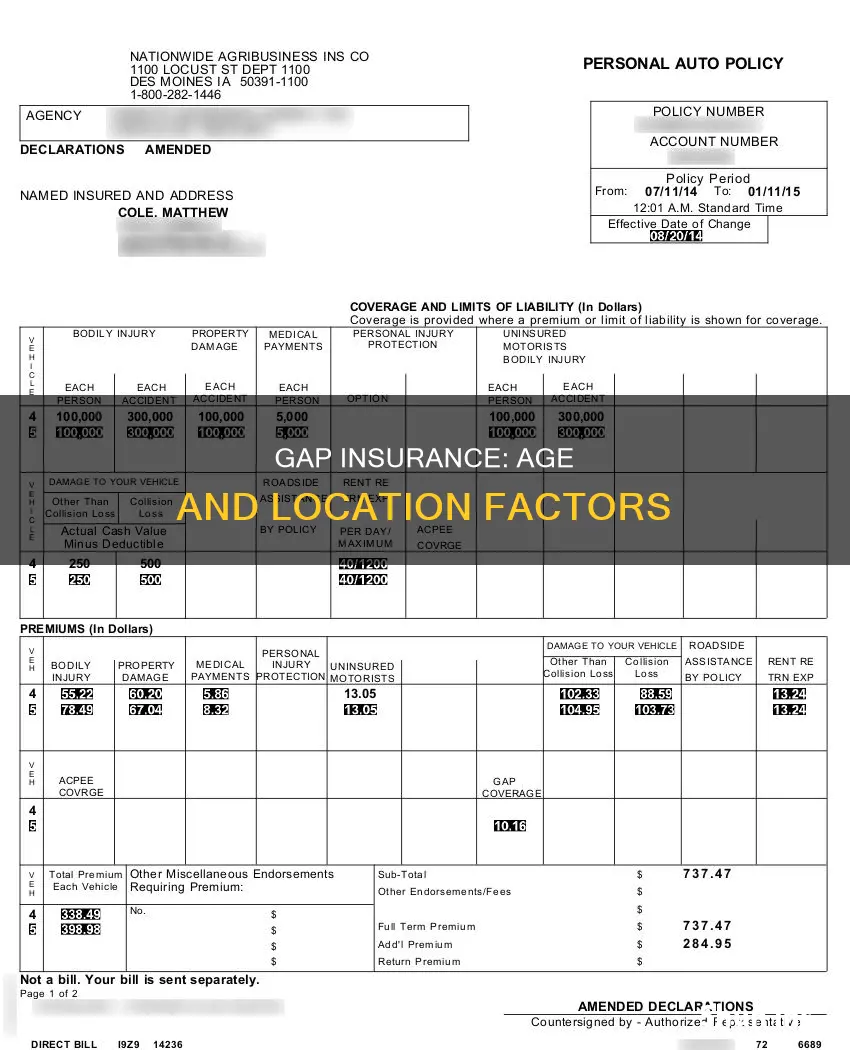

The cost of gap insurance is usually about 5% of your annual car insurance premium, although this can vary depending on factors such as your age, driving record, and location. It is typically only available as an option when buying or leasing a new vehicle, and some lenders may require it on leased vehicles.

The decision to purchase gap insurance depends on your financial situation and your willingness to take on the risk of a potential out-of-pocket expense if your car is worth less than your remaining lease or loan amount. It is a useful form of protection for those who want to ensure they are covered in the event of their car being stolen or written off.

Drunk Driving and Auto Insurance: What's the Verdict?

You may want to see also

Explore related products

$18.38 $35

$17.14 $23.95

![]()

Gap insurance is for new vehicles

Gap insurance is an optional form of coverage that can be added to an existing auto insurance policy. It is designed to protect drivers who have negative equity in their vehicles. This situation arises when the amount owed on a car loan or lease is greater than the car's current market value. This can occur due to a variety of factors, such as a small down payment, high-interest loan, fast depreciation, or a long-term loan.

When a car is totalled, stolen, or involved in an accident, standard vehicle insurance policies only cover the depreciated value of the vehicle. Gap insurance bridges the gap between the depreciated value and the outstanding loan or lease balance. For example, if your car is worth $20,000 at the time of a total loss but you still owe $25,000 on your loan, gap insurance would cover the $5,000 difference, minus your deductible.

Gap insurance is typically considered when buying or leasing a new vehicle. This is because new vehicles begin to depreciate in value as soon as they are driven off the dealer's lot, with an average depreciation of 20% in the first year. As a result, some lenders or leasing agencies may require gap insurance to protect their investment. Additionally, gap insurance is usually offered for vehicles that are one to five years old, as older vehicles may not qualify for this type of coverage.

The cost of gap insurance varies and is influenced by factors such as the driver's age, driving record, location, and vehicle type. It is generally priced as a percentage of the collision and comprehensive premiums on the auto insurance policy, typically ranging from 5% to 6%. According to the Insurance Information Institute, gap insurance can be added for as little as $20 per year.

While gap insurance provides financial protection, it is not mandatory. The decision to purchase it depends on individual circumstances and the willingness to take on the risk of negative equity. It is important to carefully consider the terms and conditions of gap insurance policies, as well as shop around for the best rates, to ensure it aligns with your specific needs.

Trip Interruption Insurance: What's Covered When Your Car Breaks Down

You may want to see also

Frequently asked questions

Yes, age is one of the factors that affect the cost of gap insurance. The cost of gap insurance is usually about 5% to 6% of your annual car insurance premium.

Yes, location affects gap insurance. The availability of gap insurance and the cost of coverage may vary from state to state.

Gap insurance is an optional auto insurance coverage that applies if your car is stolen or deemed a total loss. When your loan amount is more than your vehicle is worth, gap insurance coverage pays the difference.

Gap insurance covers the difference between the depreciated value of the car and the loan amount owed if the car is involved in an accident.