Several factors determine insurance rates, including credit history, demographics, vehicle type, driving record, and location. Interestingly, even inquiries about insurance claims can impact rates. Claims and inquiries are stored in a database called the Comprehensive Loss Underwriting Exchange (CLUE) report, which insurance companies use to assess property conditions and risks. While a soft inquiry for a quote typically doesn't affect credit scores, the CLUE report can influence insurance rates. This highlights the complexity of insurance pricing, where various factors interplay to determine an individual's rates.

| Characteristics | Values |

|---|---|

| Insurance inquiries | Can affect rates |

| Insurance claims | Can affect rates |

| Credit history | Can affect rates |

| Credit-based insurance scores | Can affect rates |

| FICO credit scores | Can affect rates |

| Demographics | Can affect rates |

| Vehicle make and model | Can affect rates |

| Coverage types and amounts | Can affect rates |

| Deductibles and insurance limits | Can affect rates |

| Insurance discounts | Can affect rates |

| Driving record | Can affect rates |

| Education level | Can affect rates |

| Marital status | Can affect rates |

| Home characteristics | Can affect rates |

| Claims history | Can affect rates |

Explore related products

What You'll Learn

![]()

Credit scores and history

While checking credit scores, insurance companies consider various factors, including the number of open accounts, the ratio of debt to available credit, past due payments, and the frequency of applying for new credit. These factors help them assess the risk associated with insuring an individual.

Maintaining a good credit score is beneficial for obtaining favourable insurance rates. Paying bills on time, reducing debt, and limiting credit card applications can positively influence insurance scores. Additionally, it is advisable to review credit reports for errors and dispute any inaccuracies, as this can also impact scores.

It's important to note that insurance companies use credit scores differently. Some states, like Oregon and Utah, restrict when insurance companies can consider credit scores, typically during the initial rate-setting or when offering a policy.

Credit-based insurance scores are just one factor in determining insurance rates, alongside demographics, vehicle type, coverage types, and driving history. However, they can carry significant weight, and a higher insurance score can lead to lower premiums.

Glass Claims: Impact on Auto Insurance Premiums

You may want to see also

Explore related products

$8.54

![Tomorotec Fingertip Pulse Oximeter Accurate Blood Oxygen Saturation Level (SpO2), Perfusion Index (PI), Pulse Rate (PR), Respiratory Rate (RR) Monitor with Lanyard [Sports & Aviation Use Only] (Black)](https://m.media-amazon.com/images/I/710sm4xwczL._AC_UL320_.jpg)

![]()

Claims and inquiries

In the case of car insurance, a driver's history of moving traffic violations, accidents, and claims is a significant factor in determining their insurance rates. A clean driving record generally results in lower insurance rates, while a history of at-fault accidents or traffic violations can lead to higher rates. Similarly, for homeowners insurance, the claims history of a property can impact the insurance rates for the current owner. This information is often tracked in Comprehensive Loss Underwriting Exchange (CLUE) reports, which maintain a record of claims filed on a particular home for up to seven years. Prospective homeowners are advised to review the CLUE report attached to the property and dispute any inaccuracies before purchasing insurance.

In addition to claims history, insurance companies may also consider an individual's credit history and score when setting insurance rates. A credit-based insurance score is calculated using similar factors to a credit score, including credit mix, debt-to-credit ratio, and payment history. A higher credit-based insurance score may result in lower insurance rates, as it indicates a lower risk of filing a claim. However, it is important to note that requesting a quote for insurance is typically considered a soft inquiry, which does not negatively impact an individual's credit score.

Other factors that can influence insurance rates include demographics such as age, marital status, and education level, as well as the type of vehicle or property being insured. Insurance companies may also offer discounts or lower rates for certain low-risk groups, such as married couples, low-mileage drivers, or safe drivers. It is beneficial to shop around and compare quotes from multiple insurance providers to find the most cost-effective option, as rates can vary significantly between companies.

Insurance Coverage Inquiries: Can They Raise Your Rates?

You may want to see also

Explore related products

![]()

Demographics

Several demographic factors can influence insurance rates, including age, sex, and marital status. For instance, married individuals are often considered less risky on the road, resulting in lower insurance rates. Conversely, teenagers and young people below the age of 25 typically face higher insurance premiums due to their higher accident risk.

Gender also plays a role in insurance rates, with males generally having more severe accidents than females, leading to higher insurance rates for males. However, it is important to note that using race or religion to set insurance rates is illegal.

In addition to demographics, insurance rates can be influenced by factors such as driving records, vehicle make and model, credit scores, and lifestyle choices. For example, those with a good driving record and lower credit risk scores may benefit from reduced insurance rates.

The Perks of Staying on Your Parent's Auto Insurance: Understanding the Timeline and Benefits

You may want to see also

Explore related products

![Tomorotec M130 Fingertip Pulse Oximeter Accurate Blood Oxygen Saturation Level (SpO2), Perfusion Index (PI), Pulse Rate (PR), Respiratory Rate (RR) Monitor Battery Lanyard [Sports & Aviation Use Only]](https://m.media-amazon.com/images/I/71PELhK3r3S._AC_UL320_.jpg)

![]()

Vehicle type

Cars with low safety ratings, high repair or replacement costs, and a higher likelihood of causing damage to others tend to be more expensive to insure. Vehicles with strong safety records and good safety equipment often qualify for discounts, while those with high-tech safety features may lead to higher premiums due to the cost of repairs. Sports cars, for example, often have high insurance rates because insurers are more likely to pay out large claims from speeding drivers. Electric cars also tend to be more expensive to insure due to their higher price tags and specialized parts.

The cost of insurance is also influenced by the vehicle's popularity with thieves and the likelihood of it being vandalized. Cars that are more expensive to repair or replace will also have higher insurance rates. This includes vehicles with extra features like lane sensors, backup cameras, and high-end audio systems.

Additionally, the level of coverage chosen will impact insurance rates. Collision and comprehensive coverage, which protect against property damage, will result in higher premiums. However, if the vehicle is worth less than $4,000, this type of coverage may not be necessary, and opting for a higher deductible can lower the insurance rate.

Gap Healthcare Insurance: Filling Coverage Gaps

You may want to see also

Explore related products

![]()

Deductibles and limits

When it comes to insurance, understanding the terms "deductibles", "limits", and "endorsements" is crucial. These terms are commonly encountered when purchasing almost any form of insurance, be it auto insurance or business insurance.

Deductibles

A deductible, also known as an annual deductible, is the amount you agree to pay out of pocket towards a covered claim before your insurance coverage starts paying. Essentially, it is a form of risk-sharing between you and your insurance company. Deductibles typically apply to comprehensive and collision coverages, with common amounts ranging from $50 to $1,000 or more. For example, if you have a $500 collision deductible and cause $2,000 worth of damage in a covered accident, you will pay the initial $500, and your insurance company will cover the remaining $1,500. However, if the damage is only $300, you would pay the entire amount since it is less than your deductible.

Limits

Policy limits, or limits of liability, represent the maximum amount your insurance company will pay for specific types of covered claims. These limits are often expressed as a set of numbers, with each number indicating a specific type of coverage. For instance, in auto insurance, the first number may represent the bodily injury liability limit per person, the second number the bodily injury liability limit per accident, and the third number the property damage liability limit per accident. While each state has minimum required liability limits, opting for higher limits provides greater protection for your assets.

Endorsements

Endorsements refer to additional clauses or amendments to a commercial insurance policy that can expand or restrict coverage. Endorsements are often tailored to meet the specific needs of a business. They can adjust the liability coverage of a policy, adding or limiting coverage based on the policyholder's requirements. Endorsements within general liability policies can also modify coverage terms, limits, or conditions to align with the insured's needs.

Choosing the Right Deductible and Limit

When selecting your insurance policy, it's important to assess your budget, your ability to cover a deductible unexpectedly, and the value of the assets you need to protect. Generally, higher deductibles and lower limits lead to lower insurance premiums, while lower deductibles and higher limits result in higher premiums but offer more financial protection.

Understanding Auto Insurance Limits: What's Your Coverage?

You may want to see also

Frequently asked questions

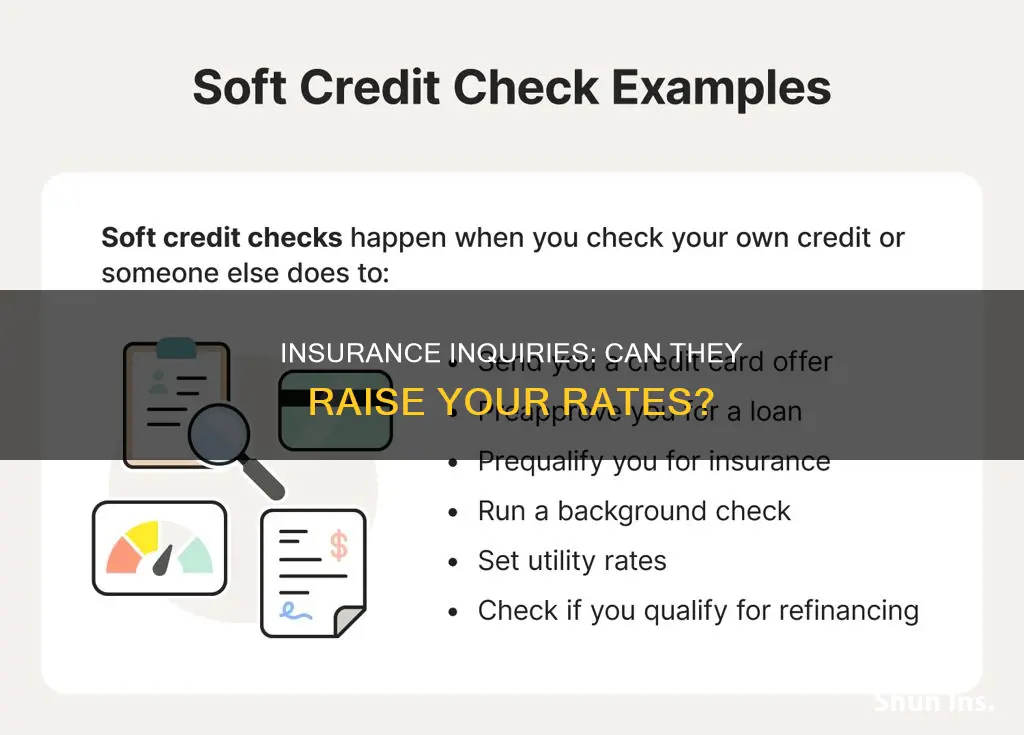

Requesting a quote for insurance should not affect your credit score. Insurance companies use soft pulls, which allow them to review your credit information without impacting your score.

Insurance companies add information to your file when they pay out money, deny a claim, or set up a file for a possible claim. This information is stored in a database called the Comprehensive Loss Underwriting Exchange report, or CLUE report. The CLUE report is reviewed by insurance companies to determine the risk of covering a property or person.

Aside from insurance inquiries, insurance rates can be affected by your credit score, demographics, vehicle make and model, coverage types, insurance company, driving record, and location.