Term life insurance is a type of insurance that guarantees a death benefit to the insured's beneficiaries if the insured person dies during the specified term. The premium for term life insurance is based on a person's age, health, and life expectancy. When buying term life insurance, you can choose the term length, which is typically 10, 15, 20, 25, or 30 years. The premium amount increases as you get older, with an average increase of 8% to 10% for every year of age. Term life insurance is generally more affordable than permanent life insurance, but the premium will go up if you renew the policy after the initial term ends.

| Characteristics | Values |

|---|---|

| Type | Level term or annually renewable |

| Length | 10, 15, 20, 25 or 30 years |

| Premium | Depends on age, health, term length, coverage amount, gender, and insurance provider |

| Renewal | Possible, but usually at a higher rate |

| Conversion to permanent coverage | Possible, but at a higher rate |

Explore related products

$18.95 $19.95

What You'll Learn

![]()

Term life insurance rates increase with age

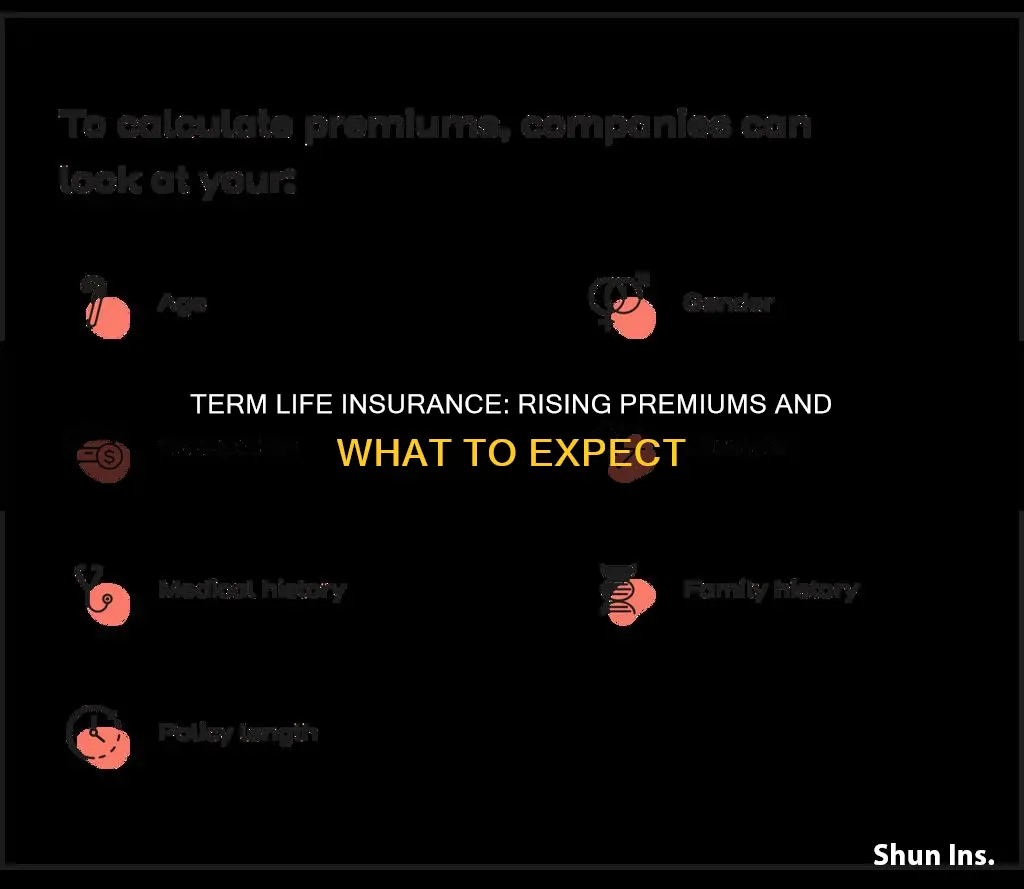

Life insurance companies use actuarial tables to estimate life expectancy and mortality rates and determine how much an individual will pay for coverage. The older you are, the more likely you are to become ill or pass away while under coverage, so age is a primary factor influencing your premium rate.

How Age Impacts Term Life Insurance Rates

Term life insurance rates typically increase with age as health issues become more frequent. The annual premium for a term life insurance policy is determined at the time of purchase and set for the duration of the policy. The premium amount increases on average by about 8% to 10% for every year of age. For example, a 45-year-old male will pay on average $1,125 for a new, 20-year term policy with $1,000,000 of coverage. The same policy purchased at age 46 will cost $1,225, and $1,345 a year if purchased at age 47.

The reason for the increase is simple: every birthday puts you one year closer to your life expectancy, and thus, you are more expensive to insure. The rates increase every year by 5% to 8% in your 40s and by 9% to 12% each year if you’re over age 50.

Factors Beyond Age That Affect Term Life Insurance Rates

In addition to age, life insurance companies consider various other factors when determining rates and whether an applicant is insurable, including:

- Type of coverage: Term life insurance plans generally have significantly lower rates than whole life insurance policies.

- Health class: Younger individuals in excellent health can expect to pay the lowest rates for life insurance. Those with pre-existing conditions are often moved into higher-rate classes.

- Gender: Since women have a longer average life expectancy than men, their rates are lower.

- Amount of coverage: The less coverage you buy, the lower the premiums.

- Health history: Generally, people in good health will pay lower rates than those with multiple health conditions.

- Lifestyle: Non-smokers are looked at more favourably than those who use tobacco. Higher-risk activities such as skydiving, rock climbing, vehicle racing and rodeo can trigger higher rates or even jeopardise your coverage eligibility.

Choosing the Right Term Life Insurance Coverage

When considering how much coverage you need, your financial obligations, current lifestyle and long-term plans will play important roles. If you can fit the monthly premium into your budget, your 20s are the best time to buy affordable term life insurance coverage. It is wise to buy life insurance when you’re younger before rates increase significantly and your policy options decline.

How Life Insurance Sales Can Make You Rich

You may want to see also

Explore related products

![The Almost Free Money Value Pack: 3 Bestsellers at One Low Price [Passive Income for Life, Almost Free Money, Garage Sale Superstar]](https://m.media-amazon.com/images/I/71IEq8XoBpL._AC_UY218_.jpg)

![]()

Level term vs. renewable term life insurance

Term life insurance is a guaranteed life benefit paid to beneficiaries of the insured after death. It provides a death benefit for a specified period of time. Once the term expires, the policyholder can either renew it for another term, convert it to permanent coverage, or allow the term life insurance policy to lapse.

Level Term Life Insurance

Level term life insurance is a policy that has a level death benefit for the entire time the policy is in effect. This means that your beneficiaries will get paid the same amount regardless of whether you die in the third year or last year of your policy. Level term life insurance is also referred to as level benefit term life insurance, highlighting the death benefit as the unchanging part of the policy.

The two options usually go hand in hand: a level life insurance death benefit with level premium payments. Most of the "normal" term policies available today are some flavour of level term life. Level term life insurance is also sometimes used to refer to a policy with a premium that doesn't change over its life (level premium term life insurance).

Level term life insurance is predictable, as it allows you to know in advance how much money you'll be leaving to your life insurance beneficiaries if you die during the policy term. It also helps with budgeting, as the amount you pay for coverage stays the same year-over-year. Additionally, it can be cheaper in the long run, as it allows you to lock in a rate and coverage amount based on your current health. If you're young and healthy, this means you can get affordable life insurance coverage for a long period of time.

However, a potential drawback of level term life insurance is that the premiums are linked to your health. Rates are locked in based on your current health, and if you improve your health over the years, you may end up paying a level but inflated price for the entire term. In this case, you might be better off with an annually renewable policy for a shorter period of time, after which you can reapply for a level term policy at a potentially lower rate.

Renewable Term Life Insurance

Renewable term life insurance is different from level term life insurance in that the premiums will go up over time as the policyholder ages. In other words, the premium payment will change from year to year and might cost you more money than level term life insurance. While renewable term life insurance might be more affordable in the short term, it can become more expensive than level term life insurance over a longer period.

Renewable term life insurance may be a good option for someone who needs coverage only temporarily, such as a person who is between jobs but wants death benefit protection. For most term life insurance buyers, however, coverage is needed for longer periods of time, such as until their children are adults or their mortgage is paid off. In these cases, a level term life insurance policy may be a more cost-effective option.

Suitability Requirements: A Must for Life Insurance Products?

You may want to see also

Explore related products

![]()

How term life insurance works

Term life insurance is a type of insurance that provides a death benefit for a specified period of time, known as the term. It guarantees payment of a stated death benefit to the insured's beneficiaries if the insured person dies during the specified term. The length of the term can vary, with policies typically lasting 10, 15, 20, or 30 years.

When purchasing a term life insurance policy, the insurance company determines the premium based on the policy's value, also known as the payout amount, and factors such as the insured person's age, gender, and health. The insurance company may also consider the company's business expenses, investment earnings, and mortality rates for each age group. In some cases, a medical exam may be required, and the insurance company may inquire about the applicant's driving record, current medications, smoking status, occupation, hobbies, and family health history.

During the term, the insured person pays premiums to maintain their coverage. If the insured person dies during the term, the insurance company will pay the policy's face value to the designated beneficiaries. This cash benefit is typically tax-free and can be used to cover expenses such as healthcare, funeral costs, consumer debt, and mortgage debt. However, beneficiaries are not obligated to use the insurance proceeds to settle the deceased's debts.

If the policy expires before the insured person's death or if they live beyond the policy term, there is generally no payout. At the end of the term, the policyholder may choose to renew the policy, but the premiums will be recalculated based on their age at the time of renewal, resulting in higher costs.

Term life insurance is usually more affordable compared to permanent life insurance because it offers a death benefit for a limited time and does not accumulate cash value. It is ideal for individuals who want substantial coverage at a lower cost. However, term life insurance premiums increase with age, and the availability of coverage may be affected by the policyholder's health status.

Term Life Insurance: Building Equity or Not?

You may want to see also

Explore related products

$20.18 $24.99

![]()

The pros and cons of term life insurance

Term life insurance is a type of insurance that provides a death benefit for a specified period of time, known as the term. Once the term expires, the policyholder can either renew it, convert it to permanent coverage, or let it lapse. The cost of term life insurance is typically based on a person's age, health, and life expectancy. It is generally considered a more affordable option compared to whole life insurance, as it does not have a cash value component. However, the premiums for term life insurance can increase with age.

Pros

- Affordable coverage: Term life insurance is usually less expensive than whole life insurance because it covers a specific period and does not build cash value.

- Simple to understand: Without the investment component, term life insurance is generally simpler and easier to understand than whole life insurance.

- Flexible term lengths: Term life insurance offers flexibility in choosing the duration of coverage, such as 10, 20, or 30 years. This allows individuals to align their coverage with their financial goals and needs.

- No long-term commitment: With term life insurance, there is no commitment after the term ends. Individuals can reassess their needs and make changes without any binding obligations.

Cons

- Premium increases upon renewal: Renewing a term life insurance policy for another term often results in higher premiums due to increased age and changing health conditions.

- No benefits if outlived: If the policyholder outlives the term, there is no payout or financial benefit unless an optional return of premium rider is purchased.

- No cash value: Term life insurance premiums only go towards coverage, and there is no portion saved or invested for future use.

- Limited coverage period: Term life insurance provides coverage for a specific term, after which the coverage ends. It may not be suitable for those seeking lifelong coverage.

Exercise and Life Insurance: Is There a Catch?

You may want to see also

Explore related products

![]()

When to buy term life insurance

Term life insurance is a type of insurance that provides a death benefit for a specified period. It is generally more affordable than whole life insurance and is suitable for people who want substantial coverage at a low cost. The best time to buy term life insurance is as soon as possible, as the younger and healthier you are, the lower your premium will be. Here are some factors to consider when deciding when to buy term life insurance:

- Family Planning: If you are planning to start a family or already have children, term life insurance can provide financial protection for your loved ones in the event of your untimely death. You can choose a term length that covers the period when your family is dependent on your income, including education costs for your children.

- Debt and Financial Obligations: Consider your debt and financial obligations when deciding to purchase term life insurance. It can help ensure that your family or estate won't be burdened with debt in the event of your death. This includes mortgage payments, credit card debt, or private student loans.

- Age and Health: Age and health are significant factors in determining the cost of term life insurance. The younger and healthier you are, the lower your premiums will be. As you age, the risk of developing health conditions increases, resulting in higher mortality rates and insurance rates. Buying term life insurance at a younger age can help lock in lower rates.

- Policy Length: Term life insurance policies typically offer coverage for a set number of years, such as 10, 15, 20, or 30 years. Choose a term length that covers the period when your family's financial needs are the highest. If you're planning to retire debt-free, a shorter-term policy might be sufficient.

- Cost and Affordability: Term life insurance is generally more affordable than whole life insurance, especially if you're young and healthy. If affordability is a concern, opt for a term policy with a lower premium. You can also compare quotes from multiple insurance companies to find the best rates.

- Conversion Options: Some term life insurance policies offer the option to convert to permanent coverage later on. If you anticipate needing lifelong coverage but can't afford it initially, look for term policies with flexible conversion options and deadlines that align with your needs.

Will Life Insurance Test for Adderall?

You may want to see also

Frequently asked questions

Term life insurance is a type of insurance that provides a death benefit for a specified period of time, known as the term. The policyholder's beneficiaries receive a payout if the insured person dies during the term. Term life insurance policies typically last for 10, 15, 20, or 30 years and can be renewed at the end of the term, usually at a higher rate.

Your age is a primary factor in determining the cost of term life insurance. The older you are when you purchase a policy, the higher the premiums will be. This is because the cost of life insurance is based on actuarial life tables that assign a likelihood of death while the policy is in force. The premium amount typically increases by about 8% to 10% for every year of age.

In addition to age, term life insurance rates are influenced by several factors, including health, gender, lifestyle behaviours (such as smoking), occupation, and family health history. The insurance company also considers its business expenses, investment earnings, and mortality rates when determining rates.