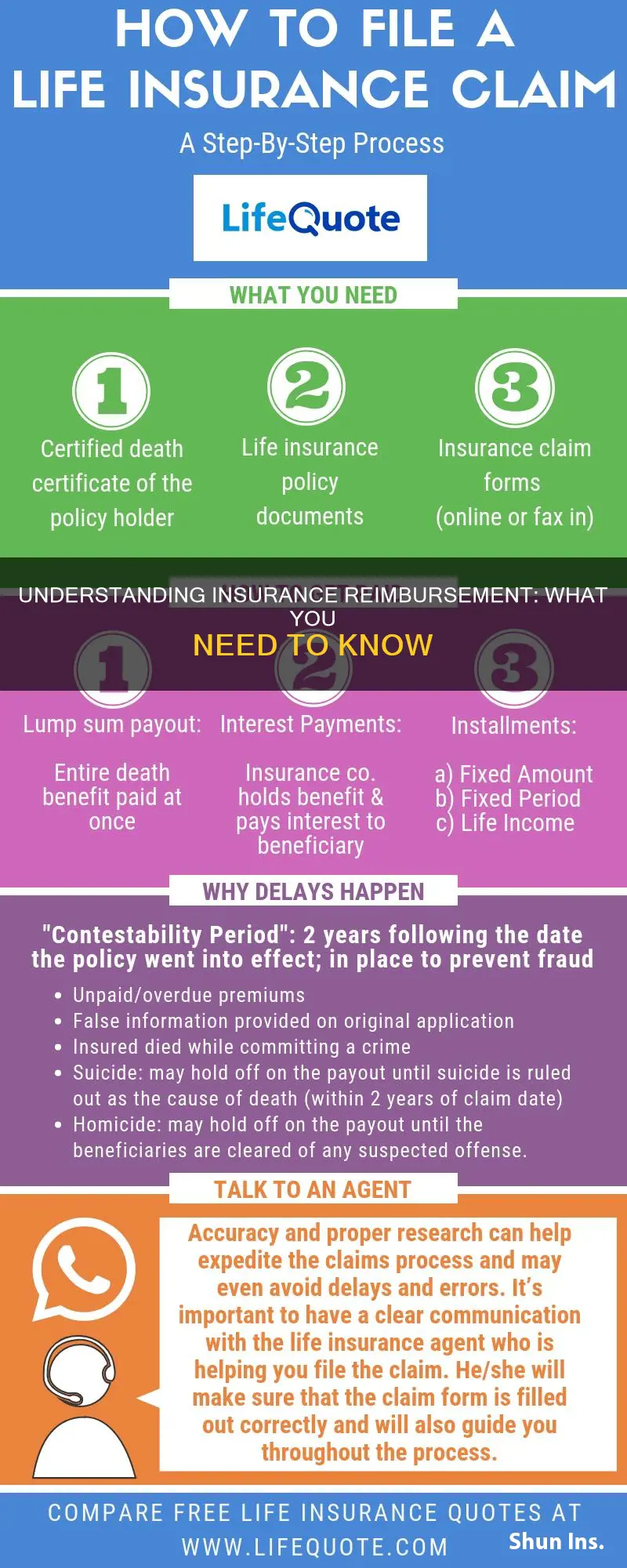

Reimbursement health insurance is a type of insurance policy where the policyholder pays for the medical expenses upfront and then claims reimbursement from the insurer. This form of insurance offers flexibility as it allows the policyholder to choose any hospital for treatment without being restricted to a network. It is important to note that reimbursement health insurance plans have specific terms and conditions, and the policyholder must review their policy to ensure that their expenses are covered under the plan.

Characteristics and Values of Reimbursement Insurance

| Characteristics | Values |

|---|---|

| Policyholder Payment | The policyholder pays for the medical expenses upfront |

| Claim Submission | The policyholder submits a claim to the insurance company for reimbursement of medical expenses |

| Claim Verification | The insurance company verifies the claim and determines eligibility for reimbursement |

| Reimbursement | The insurance company reimburses the policyholder for eligible expenses as per the policy terms |

| Coverage | Coverage includes hospitalization expenses, doctor's fees, room rent, surgery, and medicine costs |

| Flexibility | Policyholders can choose any hospital for treatment without being restricted to a network |

| Tax Implications | Reimbursements are tax-free for employees if they have a health insurance plan with minimum essential coverage (MEC) |

| Employer Offerings | Employers can offer reimbursement through Health Reimbursement Arrangements (HRAs) or qualified small employer HRAs (QSEHRAs) |

| Employee Eligibility | Employees must be enrolled in individual health insurance coverage to use reimbursement funds |

Explore related products

What You'll Learn

- Reimbursement health insurance allows you to choose any hospital for treatment

- You pay upfront for medical expenses and then claim reimbursement from the insurer

- Reimbursement insurance is available to small businesses with fewer than 50 full-time employees

- Employees must submit proof of expenses to their employer to be reimbursed

- Reimbursement insurance is beneficial for medical emergencies, as there are no upfront payments

![]()

Reimbursement health insurance allows you to choose any hospital for treatment

Reimbursement health insurance is a type of insurance policy where the policyholder pays for the medical expenses upfront and then claims reimbursement from the insurer. This process is known as a reimbursement claim. The policyholder makes the payment, and then raises a claim. If the claim is approved, the insurer reimburses the expenses as per the policy terms.

Reimbursement health insurance offers flexibility as it allows the policyholder to choose any hospital for treatment without being restricted to a network. This means that the policyholder can make their medical decisions based on their preferences and requirements, ensuring their health insurance aligns with their unique needs. This can encourage a stronger sense of control over one's well-being.

For example, in an emergency, a person with reimbursement health insurance can seek medical treatment at any hospital of their choice. They would have to bear the treatment expenses initially and keep all the bills, receipts, and records. They can then submit a claim to the insurance company for reimbursement of the medical expenses (if they are covered by the plan) within the stipulated time. The claim documents will be verified by the insurer, and if approved, the policyholder will receive reimbursement for the medical expenses, in accordance with the policy's terms and conditions.

The coverage under reimbursement health insurance is similar to that of cashless health insurance and includes hospitalisation expenses such as doctor's fees, room rent charges, surgery expenses, and medicine costs. However, it is important to carefully review one's insurance policy or company guidelines to understand which expenses are covered and ensure a smooth claims process.

Insurance and TPS: Who's Covered?

You may want to see also

Explore related products

![]()

You pay upfront for medical expenses and then claim reimbursement from the insurer

Reimbursement health insurance policies allow policyholders to pay for medical expenses upfront and then claim reimbursement from the insurer. This process involves several steps:

Firstly, the policyholder must notify their insurance provider about the hospitalisation. In the case of planned procedures, this notification usually needs to be made within 3 days, whereas for emergencies, it must be done within 24 hours.

After notification, the policyholder can avail of the necessary treatment and settle the medical bills. They will need to personally cover the medical expenses and gather all relevant bills, receipts, and medical records. It is important to diligently safeguard all documentation, as missing receipts or invoices could jeopardise the reimbursement.

Once the policyholder has compiled all the necessary documents, they can submit them to the insurance company, along with the required claim forms. The insurer will then assess the claim, scrutinising expenses to ensure they align with the policy's terms. This may include checking for any exclusions or waiting periods outlined in the policy. For example, certain expenses, such as elective cosmetic procedures, may not be eligible for reimbursement.

Upon approval, the insurer will reimburse the policyholder for the covered expenses, either partially or in full, depending on the policy's coverage and limits. It is important to note that reimbursement policies do not guarantee full reimbursement for every medical expense. Every health insurance policy has sub-limits, and exceeding the maximum reimbursement limit may lead to out-of-pocket expenses.

It is crucial to carefully review the insurance policy and company guidelines to understand the extent of coverage and align expenses with the specified categories. This clear understanding will facilitate a smooth claims process. Additionally, attention to submission deadlines is essential, as missing them could result in a rejected claim.

Insurance Contracts: When Do They Begin?

You may want to see also

Explore related products

![]()

Reimbursement insurance is available to small businesses with fewer than 50 full-time employees

Reimbursement insurance is a flexible and increasingly popular option for small businesses with fewer than 50 full-time employees. It allows employers to reimburse workers for individual healthcare expenses, including insurance premiums, up to a set limit. This option is known as a Health Reimbursement Arrangement (HRA) and is an alternative to a traditional group health plan.

With an HRA, employers can provide defined non-taxed reimbursements to employees for qualified medical expenses. This includes monthly premiums and out-of-pocket costs, such as copayments and deductibles. Employees must be enrolled in individual health insurance coverage to use the funds. There are two types of HRAs available to small businesses: the Individual Coverage HRA (ICHRA) and the Qualified Small Employer HRA (QSEHRA).

The ICHRA is suitable for businesses of all sizes, allowing reimbursement for individual insurance premiums and medical expenses. The QSEHRA is tailored for small employers with fewer than 50 employees, offering tax-free reimbursement for qualified health expenses. Small businesses can also take advantage of the Small Business Health Options Program (SHOP) coverage to qualify for the Small Business Health Care Tax Credit, which can save up to 50% of the employer's contribution for two consecutive years.

While it is not federally mandated for small businesses with fewer than 50 employees to provide health insurance, doing so can offer significant benefits. These include attracting and retaining talent, improving employee health and productivity, and fostering a healthier and more satisfied workforce.

Understanding Allstate Insurance's Billing Address Requirements

You may want to see also

Explore related products

![]()

Employees must submit proof of expenses to their employer to be reimbursed

Employees who spend their own money on job-related items may request reimbursement. However, not every expense will be reimbursable. It is important to set parameters for various expense categories. For example, a company may reimburse remote employees for their internet service but not their work computer.

There are several types of expenses that are generally taxable for the employee, such as the personal use of a company car, trips and prizes, and services. However, there are also many non-taxable reimbursement categories, such as approved employee business reimbursements that conform to IRS expense reimbursement guidelines.

To qualify as an accountable reimbursement plan, the expense must occur in the performance of services as an employee of the employer, the employee must substantiate their expenses, and return any excess amounts. When an employer reimburses an employee pursuant to an accountable plan, the reimbursement won’t count as wages or income to the employee.

ACA's Impact: Insured Americans Surge

You may want to see also

Explore related products

![]()

Reimbursement insurance is beneficial for medical emergencies, as there are no upfront payments

Reimbursement insurance is a specific account-based health plan that allows employers to provide defined non-taxed reimbursements to employees for qualified medical expenses. It is beneficial for medical emergencies as there are no upfront payments required. Instead of paying upfront, the policyholder pays for the medical expenses out of their own pocket and is later repaid by the insurance company. This is particularly useful in situations where patients are unable to pay their bills, as they are not required to pay anything before receiving treatment.

While reimbursement insurance does not require upfront payments, it is important to note that the policyholder may need to pay some or all of their deductible before receiving reimbursement. The deductible is the amount that the policyholder must pay out of their own pocket before the insurance company starts covering the costs. In some cases, medical providers may ask for partial or full payment of the deductible before providing medical services. However, this is not always the case, and some providers may send the bill to the insurance company before charging the patient.

It is also worth mentioning that reimbursement insurance typically covers a range of medical expenses, including hospitalization expenses such as doctor's fees, room rent charges, surgery expenses, and medicine costs. Additionally, reimbursement insurance can help lower monthly insurance payments, as the reimbursement amount can vary based on factors such as age and the number of dependents. This makes it a more affordable option for many individuals and families.

Overall, reimbursement insurance can provide peace of mind during medical emergencies by eliminating the worry of upfront payments. By understanding the coverage provided and the reimbursement process, individuals can ensure a smooth claims process and focus on their health and recovery without the added financial stress.

Mileage-Based Insurance: The Future of Driving and Insurance

You may want to see also

Frequently asked questions

Reimbursement insurance is a type of insurance policy where the policyholder pays for the medical expenses upfront and then claims reimbursement from the insurer.

The policyholder pays for the treatment upfront and then raises a claim. If the claim is approved, the insurer reimburses the expenses as per the policy terms.

Reimbursement insurance offers flexibility as you can choose any hospital for treatment without being restricted to a network. It also allows you to make your medical decisions based on your preferences and requirements.