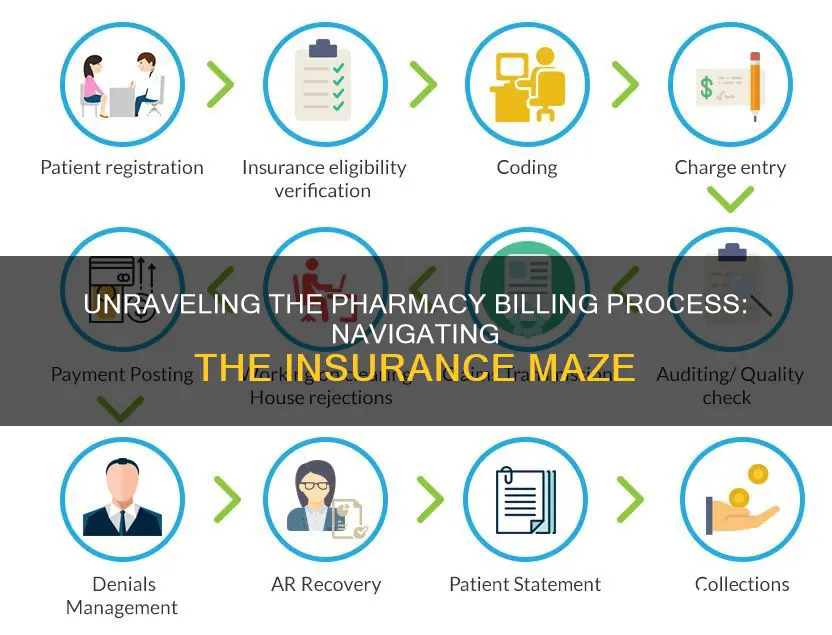

Pharmacy billing and reimbursement is a complex process that involves multiple steps and stakeholders. The billing cycle typically begins with receiving a prescription from a patient, followed by gathering patient data, including insurance information, and transmitting the pharmacy claim to the insurance company. This is followed by third-party payor adjudication, where the insurance company determines the financial responsibility of the patient and the insurance plan. The process concludes with payment processing, where the pharmacy receives reimbursement for the medication dispensed. Properly entering patient and prescription information is crucial to avoid errors and allegations of fraud. The revenue cycle in pharmacy billing encompasses medication procurement, inventory management, dispensing methods, administration, coding, and billing, ultimately impacting reimbursement. Understanding the dynamics of pharmacy billing and reimbursement is essential for effective financial management in the healthcare industry.

Explore related products

What You'll Learn

- Reimbursement policies and plans (e.g., HMOs, PPO, CMS, private plans)

- Third-party resolution (e.g., prior authorization, rejected claims, plan limitations)

- Third-party reimbursement systems (e.g., PBM, medication assistance programs, coupons, and self-pay)

- Healthcare reimbursement systems (e.g., home health, long-term care, home infusion)

- Coordination of benefits

![]()

Reimbursement policies and plans (e.g., HMOs, PPO, CMS, private plans)

When it comes to reimbursement policies and plans, there are several options to choose from, each with its own unique features, advantages, and disadvantages. Here is an overview of some of the commonly available reimbursement policies and plans:

Health Maintenance Organization (HMO)

HMOs are a type of managed healthcare system that focuses on providing medical treatment on a prepaid basis. Members typically pay a fixed monthly fee, regardless of the amount of medical care needed. In return, HMOs offer a wide range of medical services, including office visits, hospitalization, and surgery, mostly within their network of contracted physicians and facilities. One of the key advantages of HMOs is their cost-effectiveness, as they have agreements in place with providers to pay them less, resulting in lower costs for plan members. Additionally, HMO members benefit from low out-of-pocket expenses and a strong focus on wellness and preventative care. However, one of the disadvantages of HMOs is the potential difficulty in obtaining specialized care, as members usually need a referral from their chosen primary care physician (PCP) to see a specialist.

Preferred Provider Organization (PPO)

PPOs are another type of managed healthcare system that offers a network of healthcare providers for a specific rate. One of the key advantages of PPOs is the flexibility they offer, allowing members to receive care from any healthcare provider, both in and out of their network, without requiring referrals. When using a PPO, staying within the network results in smaller copays and full coverage. However, choosing a provider outside the network will lead to higher out-of-pocket costs and potentially limited coverage. PPOs are generally more expensive than HMOs, with higher monthly premiums, but they provide the benefit of having some coverage even when going out of the network.

Point of Service (POS)

A POS plan combines characteristics of both HMO and PPO plans. Like an HMO, a POS plan usually has a minimal copay when using an in-network provider, and members must choose a primary care physician for referrals within the network. However, if members opt for out-of-network healthcare, the coverage functions more like a PPO, with higher deductibles and copayments. One of the advantages of a POS plan is the freedom of choice it offers, allowing members to mix the types of care they receive, both in and out of the network. Additionally, there is no requirement to consult a primary care physician for non-network care.

Exclusive Provider Organization (EPO)

An EPO is a managed care plan where services are covered only if members use doctors, specialists, or hospitals within the plan's network, except in emergency situations. EPOs do not provide coverage for out-of-network care, except in emergencies.

Understanding Loss Payees: Protecting Lenders and Borrowers Alike

You may want to see also

Explore related products

![]()

Third-party resolution (e.g., prior authorization, rejected claims, plan limitations)

Third-party resolution is a critical component of the billing and reimbursement process in pharmacies. It involves addressing issues such as prior authorization, rejected claims, and plan limitations. Here's an in-depth look at each of these aspects:

Prior Authorization

Prior authorization is a process utilized by health insurance companies to determine whether they will cover a prescribed medication, procedure, or service. It is a cost-control measure to assess the medical necessity and cost implications before authorizing treatment. This process is often required for more expensive and specialized treatments or medications, such as surgeries, MRIs, durable medical equipment, and specialty drugs. The decision to approve or reject a prior authorization request rests with a clinician at the insurance company, and their determination can delay or deny patient access to the prescribed treatment.

Rejected Claims

Rejected claims can occur for various reasons, such as incorrect or incomplete information, non-covered medications or procedures, or issues with insurance coverage. When a claim is rejected, the pharmacy or healthcare provider may need to contact the insurance company to resolve the issue or submit additional information. In some cases, an appeal process may be initiated to challenge the rejection.

Plan Limitations

Plan limitations refer to the specific terms and conditions of an insurance plan that may restrict coverage for certain medications, procedures, or services. These limitations can include factors such as age, medical necessity, the availability of generic alternatives, or drug interactions. Understanding plan limitations is essential for pharmacies to ensure accurate billing and reimbursement.

Overall, third-party resolution plays a crucial role in ensuring that patients receive the necessary treatments while also managing the financial implications for all parties involved. It requires coordination between pharmacies, healthcare providers, and insurance companies to navigate the complex landscape of insurance coverage and reimbursement.

Term Insurance Takeover: Navigating the Transition When Your Carrier is Sold

You may want to see also

Explore related products

![]()

Third-party reimbursement systems (e.g., PBM, medication assistance programs, coupons, and self-pay)

Pharmacy billing and reimbursement is a complex process that involves multiple stakeholders, including the patient, the pharmacy, the prescribing physician, insurance providers, and third-party reimbursement systems. Third-party reimbursement systems play a crucial role in helping patients access their medications and reducing their out-of-pocket expenses. Here is an overview of some common third-party reimbursement systems:

Pharmacy Benefit Managers (PBMs)

Pharmacy Benefit Managers (PBMs) are companies that act as intermediaries between health insurers, Medicare Part D drug plans, large employers, and other payers. They develop formularies (lists of covered medications), negotiate rebates and discounts with drug manufacturers, and contract with pharmacies for reimbursements. PBMs have a significant impact on drug costs and patients' access to medications. They are paid rebates by drug manufacturers and then reimburse pharmacies on behalf of health insurance providers for drugs dispensed to patients. PBMs have faced scrutiny due to their role in rising prescription drug costs, and there have been calls for greater transparency in their business practices.

Medication Assistance Programs

Medication Assistance Programs are typically offered by drug manufacturers to provide financial assistance to patients with special financial needs or those who cannot afford their medications. Patients may present a special prescription card issued by the manufacturer, which entitles them to reduced prices for their medications. These programs help improve medication adherence by making treatments more affordable for patients.

Coupons and Vouchers

Drug manufacturers may also offer coupons or vouchers that can be processed as prescription cards, reducing the cost of brand-name medications for a limited number of fills. These coupons can be a valuable tool for patients struggling to afford their prescriptions, especially when used in conjunction with insurance coverage.

Self-Pay

In some cases, patients may choose to pay for their prescription medications out of pocket, without relying on insurance. This option is typically chosen by patients who do not have insurance coverage or prefer not to use it for various reasons, such as high deductibles or the medication not being covered by their plan. Self-pay allows patients to maintain privacy regarding their medical conditions and treatment choices.

These third-party reimbursement systems play a crucial role in helping patients access their medications and reducing their financial burden. They work in conjunction with insurance providers and pharmacies to ensure that patients can obtain the treatments they need at a more affordable cost.

Understanding the Fundamentals of Minimum Sum Assured in Term Insurance

You may want to see also

Explore related products

![]()

Healthcare reimbursement systems (e.g., home health, long-term care, home infusion)

Healthcare reimbursement systems such as home health, long-term care, and home infusion differ from the pharmacy billing cycle in that they involve a broader range of services and care options. These systems are designed to provide care for individuals who require ongoing support and assistance with their daily living activities, including but not limited to dressing, feeding, using the bathroom, meal preparation, and mobility.

Home health care involves providing medical and personal care services to individuals in their homes. It often includes skilled nursing care, physical therapy, occupational therapy, or other healthcare services that are ordered by a physician. Home health care aims to help individuals recover, maintain their independence, and prevent or delay the need for long-term care.

Long-term care, on the other hand, refers to a range of services that assist individuals with chronic illnesses or disabilities who cannot care for themselves for extended periods. Long-term care can be provided at home, in assisted living facilities, or in nursing homes. It includes both custodial and skilled care, focusing on maximizing patients' quality of life and meeting their needs over an extended period.

Home infusion therapy is a specific type of healthcare service that involves administering medications through a needle or catheter outside of a hospital setting, typically in a patient's home or an alternate site such as an ambulatory infusion suite. This approach is often preferred by patients as it allows them to continue their normal activities while receiving treatment. Home infusion is a safe and effective alternative to inpatient care for acute and chronic conditions, including infections, cancer, dehydration, gastrointestinal diseases, and immune system diseases.

The reimbursement for these healthcare services can vary depending on the patient's insurance plan and the specific services provided. In the United States, Medicare and Medicaid play a significant role in covering the costs of long-term care, especially for senior citizens. However, Medicare's fee-for-service program does not typically cover home infusion therapy, creating a financial burden for patients who require this type of treatment.

Overall, healthcare reimbursement systems for home health, long-term care, and home infusion are designed to provide ongoing support and care for individuals who need assistance with their daily living activities, ensuring their well-being and quality of life.

Understanding Key Man Insurance: Securing Corporate Stability

You may want to see also

Explore related products

![]()

Coordination of benefits

When an individual has multiple health plans, the primary plan will pay its share of the healthcare costs first. The secondary plan then pays up to 100% of the remaining costs, as long as these costs are covered under the plan. It is important to note that neither plan will pay more than 100% of the total healthcare costs, so having multiple health insurance plans does not result in double the benefits.

The determination of which plan is primary and which is secondary depends on various factors, including the type of plan, the size of the company, and the location. For example, in the case of employer-sponsored plans, the individual's employer is generally the primary payer, while the spouse's employer plan is secondary. In situations where a child has dual coverage by married parents, the "birthday rule" is often applied, where the parent whose birthday falls earlier in the year has their insurance plan considered primary.

The coordination of benefits process helps to streamline the billing and reimbursement process, ensuring that individuals receive the benefits they are entitled to while avoiding overpayments by either plan. It is important for individuals with multiple insurance plans to review their policy documents, notify their insurance providers, and submit claims and documentation to both primary and secondary insurers to ensure smooth coordination of benefits.

Unraveling the Intricacies of Insurance Reserves: A Guide to Understanding This Crucial Concept

You may want to see also

Frequently asked questions

The pharmacy billing cycle involves receiving the prescription, gathering patient data, pharmacy claim transmittal, and third-party payor adjudication.

Information required includes the patient's name, address, date of birth, contact information, allergies, and payment type (cash vs. insurance).

Third-party payor adjudication is when the payor compares the charges with the terms of the patient's benefit plan and determines what the patient owes and what the insurance plan is financially responsible for.

Fee-for-service reimbursement is when providers receive payment for each service rendered, whereas episode-of-care reimbursement is when providers receive one lump sum for all the services they provide related to a condition or disease.