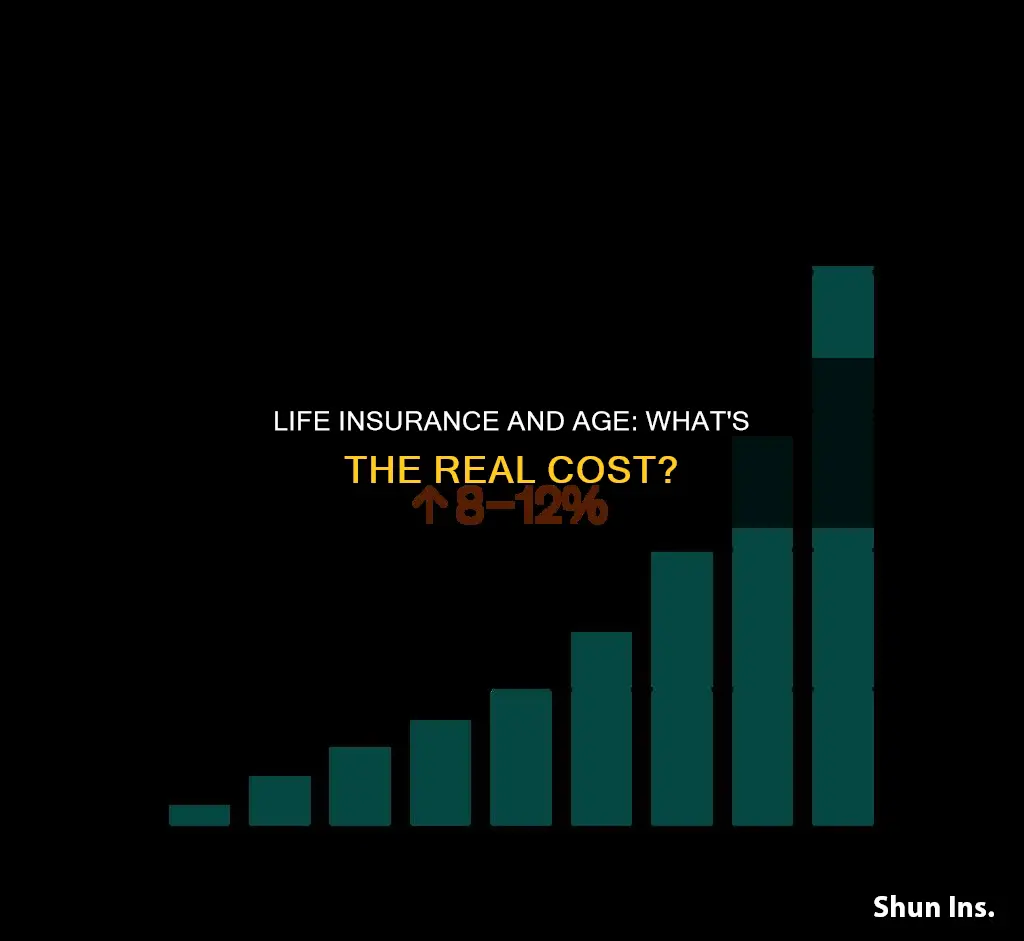

Age is one of the biggest factors influencing the cost of life insurance premiums. The older you are, the more likely you are to become ill or die, and so the more expensive your premiums will be. Life insurance premiums typically increase by around 8-10% for every year of age, but this can be as high as 12% if you're over 50. The type of policy you choose will also affect how your premium changes with age. Term life insurance premiums are set at the same price for the entire term, but this price will be higher if you buy the policy later in life. Whole life insurance has a consistent premium, but the age at which you buy the policy still matters – it's cheaper if you're younger.

| Characteristics | Values |

|---|---|

| Life insurance premiums | Increase with age |

| Risk | The older you get, the more high-risk you are in passing |

| Age and coverage | The older you are, the more coverage you will require |

| Age and qualification | Age can affect whether a person qualifies for life insurance coverage at all |

| Age and term life insurance | Term life insurance premiums are set at the same price for the entire term, but this price will be more expensive if you purchase the policy later in life |

| Age and whole life insurance | Whole life insurance has a consistent premium, but the age at which you purchase the policy matters. Getting your whole life coverage at 30 years old can lower your premium by thousands of dollars, compared to age 50 |

| Age and type of policy | Term life insurance is more suitable for younger people, while permanent life insurance is more suitable for older people |

| Age and financial situation | The younger you are, the fewer financial responsibilities you will have |

| Age and family situation | The older you are, the more likely you are to have dependents |

Explore related products

What You'll Learn

![]()

Life insurance premiums increase with age

Life insurance policies typically go up with every year you age, but you can expect a more substantial increase when you reach 50 years old. For example, if you opt for a 20-year term policy at age 20, you could pay around $250 every year until you reach the end of the term. However, renewing your coverage for another 20 years at 40 years old could now cost you $400 annually because of your increased risk factors.

Term life insurance premiums are set at the same price for the entire term, but this price will be more expensive if you purchase the policy later in life. And if you want to renew the coverage for another period after your term ends, your new premium will be calculated based on your current age.

Whole life insurance, a type of permanent life insurance, also has a consistent premium you'll be paying each period. The cost of your insurance won't increase each year because of age, but the age at which you purchase the policy matters. Getting your whole life coverage at 30 years old can lower your premium by thousands of dollars compared to age 50.

Age remains one of the most influential factors affecting life insurance premiums. Insurers assess premiums based on multiple personal rating factors, but an emphasis is placed on mortality risk, and the probability of death rises steadily as we get older.

Your life insurance needs might also change as you age. For example, a young person living with their partner with no plans of having children may need less coverage and will often qualify for cheaper life insurance rates. On the other hand, an older person who is supporting a family or running a business will likely require a larger policy that lasts longer. This policy, because of the larger overall coverage and older age of the applicant, may be more expensive compared to the younger person who needs less coverage.

In general, the rule of thumb says that the best time to buy insurance is while you're young, as the premiums will be low. The logic is simple: it is considered that if you are young, you are healthier and less susceptible to illnesses that come with ageing. Therefore, you have fewer health-related risks and, by extension, a lower premium.

Life Insurance and TIA's: What You Need to Know

You may want to see also

Explore related products

$12.99 $14.95

![]()

Age affects term life insurance

Age is one of the most influential factors in determining life insurance premiums. This is because the older you are, the more likely you are to become ill or die while under coverage. Life insurance companies use actuarial tables to estimate life expectancy and mortality rates, which, along with other factors, determine how much you'll pay for coverage.

Term life insurance premiums are set at the same price for the entire term, but this price will be more expensive if you purchase the policy later in life. For example, a 20-year term policy at age 20 could cost around $250 per year, whereas renewing coverage for another 20 years at age 40 could cost $400 annually due to increased risk factors.

The premium amount for term life insurance typically increases by about 8% to 10% for every year of age. This increase can be as low as 5% annually in your 40s and as high as 12% annually if you're over 50. Thus, it is generally recommended to purchase term life insurance at a younger age to secure lower premiums.

Additionally, age can affect the availability of term life insurance coverage. Most carriers only offer 20-year term policies to individuals aged 18 to 70. After this age, the length of coverage offered becomes restricted.

When considering term life insurance, it is important to keep in mind that the coverage amount you need depends on various factors, including your age, income, mortgage, debts, and anticipated funeral expenses.

Life Insurance: A Worthless Investment or Smart Move?

You may want to see also

Explore related products

![]()

Age affects whole life insurance

Age is one of the biggest factors that determines the premium on a life insurance plan. The older you are, the more your life insurance plan will cost. This is because the cost of life insurance is based on actuarial life tables that assign a likelihood of dying while the policy is in force. In other words, the older you are, the more likely you are to pass away while under coverage, and the more likely a death benefit claim will need to be paid out.

Whole life insurance, a type of permanent life insurance, has a consistent premium that remains the same each period. However, the age at which you purchase the policy matters. For example, getting whole life coverage at 30 years old can lower your premium by thousands of dollars compared to getting it at 50. Permanent life insurance is more suitable for later life when your debts and mortgage are paid off and your children are grown up. It is more expensive because there is a guaranteed payout, but the advantages are that you have lifetime coverage and your premiums won't increase, even if your health worsens.

It is worth noting that permanent life insurance premiums are usually 10-15 times higher than term life insurance premiums because policyholders are covered for a much longer period, and the policy can earn cash value.

In addition to age, other factors that influence life insurance premiums include overall health, gender, smoking status, participation in risky hobbies, and pre-existing conditions.

Specialty Life Insurance: Legit or a Scam?

You may want to see also

Explore related products

![]()

Age affects eligibility for life insurance

Age is one of the most influential factors when it comes to determining eligibility for life insurance and the premium payable. Insurers assess premiums based on multiple personal rating factors, but an emphasis is placed on mortality risk, and the probability of death rises steadily as we get older.

Insurers use actuarial life tables to help set life insurance rates. These tables estimate life expectancy and mortality rates and, along with other factors, can determine how much someone will pay for life insurance coverage.

The older you are, the more likely you are to become ill or die while under coverage. This means that the older you are when you purchase a policy, the more expensive the premiums will be. The premium amount increases, on average, about 8% to 10% for every year of age; it can be as low as 5% annually if you're in your 40s, and as high as 12% annually if you're over 50.

Age also affects whether a person will qualify for life insurance coverage at all, with qualifying medical exams getting increasingly stringent as you get older. Most carriers only offer 20-year term policies to those aged 18 to 70, and after that, you won't be able to get a term that lengthy. Whole life insurance usually has a higher age limit, so you may still be able to find coverage until you're about 85 years old.

While it's never too late to buy life insurance, and there is no right or wrong age to do so, it's generally recommended to purchase life insurance when you're young and healthy, as the premiums will be lower.

Life Insurance Consumer Reports: What You Need to Know

You may want to see also

Explore related products

![]()

Age is not the only factor influencing life insurance premiums

- Health and Medical History: Your overall health and medical history can affect your life insurance premiums. Pre-existing medical conditions, chronic illnesses, high blood pressure, obesity, and other health issues can increase your premiums as they contribute to potential future health complications.

- Gender: On average, men tend to pay higher life insurance premiums than women due to their shorter life expectancy. According to statistics, women live approximately five years longer than men, resulting in lower premiums for women.

- Smoking Status: Smokers are often subject to higher life insurance premiums because smoking is associated with an increased likelihood of developing certain health conditions.

- High-Risk Activities: Participation in dangerous activities or extreme sports, such as skydiving, rock climbing, or racing, can significantly drive up your life insurance premiums. Insurers view these activities as increasing the risk of injury or death.

- Driving Record: A history of driving violations or accidents within a certain timeframe can also impact your premiums. Insurers may consider you a higher risk if you have multiple infractions on your record.

- Mental Health: Mental health issues, such as depression, are associated with higher mortality rates. Consequently, individuals with mental health diagnoses may be required to pay higher life insurance premiums.

- Payment Schedule: The frequency of your payments can also make a difference. Paying your life insurance premiums annually instead of monthly may result in cost savings.

- Occupation: Your choice of occupation can influence your premiums. Certain professions are considered higher risk by insurers due to their inherent dangers or accident-prone nature.

- Type of Policy: The type of life insurance policy you choose also plays a role in determining premiums. Term life insurance is generally more affordable than permanent life insurance, which offers coverage for a lifetime.

- Coverage Amount: The amount of coverage you need will impact your premiums. Higher coverage limits present a greater financial risk to the insurance company, resulting in higher premiums to compensate for that risk.

Life Insurance Payouts: Tax Implications and Exemptions

You may want to see also

Frequently asked questions

Age is one of the most influential factors when it comes to life insurance premiums. The older you are, the more high-risk you are considered to be, and so the more you will have to pay for your insurance coverage.

Term life insurance premiums are set at the same price for the entire term, but this price will be more expensive if you purchase the policy later in life.

Whole life insurance has a consistent premium you pay each period. While the cost of your insurance won't increase each year because of age, the age at which you purchase the policy does matter. The older you are, the more you will pay.

Yes, life insurance companies have maximum age limits. Term life policies typically cap at around 75 years old, while whole life insurance policies usually have a higher age limit, with coverage available until around 85 years old.