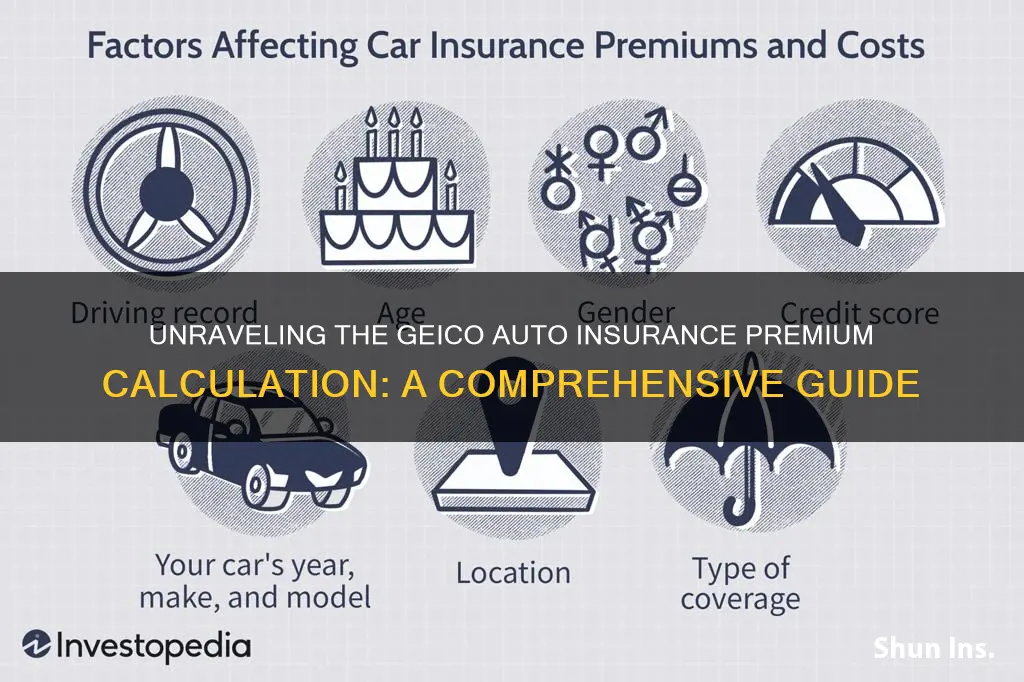

GEICO auto insurance rates are calculated by GEICO actuaries, who assess potential risks from statistical data. A multitude of characteristics are used to determine the odds that someone will have an accident, and insurance rates are then determined based on an individual's combination of high and low-risk factors. The more likely you are to have an accident, the higher your premium will be. Factors that influence your insurance premium include the car you drive, how often you drive it, where it is kept, the safety features installed, your age, gender, marital status, credit-based insurance score, prior insurance history, and your driving record.

| Characteristics | Values |

|---|---|

| Vehicle safety features | Airbags, anti-lock brakes |

| Age | |

| Gender | |

| Marital status | |

| Credit-based insurance score | |

| Prior insurance history | |

| Driving record | |

| Driving habits | |

| Membership in an organization | |

| Defensive driving courses | |

| Location | |

| Vehicle make and model | |

| Vehicle usage | |

| Coverage options | Bodily injury liability, property damage liability, uninsured motorist coverage, emergency roadside service, rental reimbursement, mechanical breakdown insurance |

Explore related products

What You'll Learn

![]()

Vehicle safety features

- Forward collision warning: This feature warns the driver of a potential front collision, giving them time to react and avoid an accident.

- Lane departure warning: This system alerts the driver when the vehicle deviates from its lane, helping to prevent accidental lane changes and reducing the risk of sideswipe collisions.

- Rear cross-traffic warning: Sensors detect vehicles approaching from the sides and warn the driver, reducing the risk of collisions when reversing or changing lanes.

- Automatic emergency braking: This feature can sense an impending collision and automatically apply the brakes to avoid or mitigate the impact.

- Pedestrian automatic emergency braking: Similar to automatic emergency braking, this system specifically detects pedestrians and helps avoid accidents involving them.

- Rear automatic braking: This feature automatically applies the brakes when an obstacle is detected behind the vehicle, preventing or reducing the severity of rear-end collisions.

- Blind spot intervention: This system alerts the driver to vehicles in their blind spot, reducing the risk of lane change collisions.

- Adaptive cruise control: This feature maintains a set distance from the vehicle ahead, automatically adjusting the speed to ensure a safe following distance.

- Lane centering assistance: This system helps keep the vehicle centred in its lane, reducing the driver's workload and the risk of drifting into adjacent lanes.

- Lane-keeping assistance: This feature provides gentle steering assistance to keep the vehicle within its lane, preventing unintentional lane departures.

- Automatic high beams: These headlights automatically adjust their brightness based on surrounding conditions, improving visibility without dazzling other drivers.

- Automatic crash notification: In the event of a collision, this feature automatically alerts emergency services, potentially speeding up response times and reducing the severity of injuries.

While these safety features can increase the cost of the vehicle and repairs, they have been proven to reduce accident frequency and severity. As a result, insurers may offer discounts for vehicles equipped with these advanced safety systems, making them a worthwhile investment for drivers seeking enhanced safety and lower insurance premiums.

Capital One: Gap Insurance Coverage

You may want to see also

Explore related products

![]()

Age, gender, marital status, and location

Age, gender, and marital status are all factors that GEICO uses to calculate auto insurance premiums. These factors are based on statistical data, which GEICO actuaries analyse to assess the potential risk of an individual having an accident.

Age is a significant factor in determining auto insurance premiums. Younger drivers, particularly teenagers, are considered to be at a higher risk of accidents due to their lack of driving experience. As a result, they often face higher insurance premiums. On the other hand, older drivers may also experience an increase in premiums due to age-related changes in vision, reaction time, and other physical abilities.

Gender is another factor that influences insurance rates. Historically, women have been considered lower-risk drivers and have enjoyed lower premiums. However, this practice has been challenged in recent years, and some insurance companies are moving towards gender-neutral pricing.

Marital status also plays a role in insurance premium calculations. Married individuals are often considered more stable and responsible, leading to lower insurance rates. Conversely, single individuals may face higher premiums due to perceived higher risk.

Location is a critical factor in determining auto insurance premiums. Insurance rates can vary significantly depending on the state or region in which the insured vehicle is located. This is because different areas have different accident rates, theft rates, weather conditions, and population densities, all of which can impact the likelihood of accidents or vehicle damage. Urban areas, for example, tend to have higher insurance rates due to increased traffic congestion, higher accident rates, and more frequent vehicle thefts.

In addition to these factors, GEICO also takes into account various other factors, such as driving history, claims history, vehicle type, safety features, and credit score, to calculate auto insurance premiums. By considering a combination of these factors, GEICO aims to provide fair and accurate insurance rates for its customers.

U.S. Auto Insurance: USAA's Cost and Coverage

You may want to see also

Explore related products

![]()

Driving record and history

Driving records and history are key factors in determining auto insurance premiums at GEICO. The company assesses an individual's driving record to evaluate their risk as a driver and calculate their premium. GEICO checks an individual's driving record every 6 to 12 months, especially when applying for a new policy or renewing an existing one. This process involves examining the customer's driving history, including any recent at-fault accidents, traffic violations, or speeding tickets, which can significantly impact their insurance rates.

GEICO, like all insurance companies, evaluates an individual's driving record to determine their insurance rates and overall risk as a driver. The company typically checks an individual's driving history when they first become a customer and then periodically, usually every 6 to 12 months, or when the policy is up for renewal. This process allows GEICO to reassess the driver's risk profile and adjust their premium accordingly.

The frequency of checks may vary depending on the customer's tenure with GEICO. New customers can expect an initial assessment of their driving record to set their insurance rates. For existing customers, GEICO may conduct checks less frequently if they have a long-standing relationship with the company and the company already has insights into their driving habits.

GEICO obtains driving records from state DMVs or LexisNexis, reviewing the past 5 years of driving history, including accidents and moving violations. Any new violations since the last check can result in increased insurance rates. For example, GEICO insurance premiums typically increase by an average of 60% after an accident and by 50% after a speeding ticket.

The impact of driving records on insurance premiums highlights the importance of maintaining a clean driving history. Safe driving behaviours and a spotless driving record are rewarded by insurance companies, resulting in lower premiums over time. Conversely, accidents, claims, speeding tickets, and other moving violations can lead to higher premiums.

In addition to driving records, GEICO considers various other factors when calculating auto insurance premiums, including the vehicle's safety features, age, gender, marital status, credit-based insurance score, and prior insurance history. These factors collectively contribute to determining an individual's risk profile and the corresponding premium.

Auto Insurance: Bicycle Accident Coverage?

You may want to see also

Explore related products

![]()

Insurance coverage and limits

Insurance coverage limits define the maximum amount an insurer will pay out for a covered claim. Each type of coverage in a policy has its own specified limit, and it's important to understand these limits to ensure you have adequate protection.

For example, liability coverage limits on car insurance are typically shown as three separate numbers, such as $50,000/$100,000/$30,000. These numbers represent the maximum amounts that an insurer will pay out for bodily injuries per person, per accident, and property damage, respectively. In this example, the insurer will pay up to $50,000 for bodily injuries per person, $100,000 total for bodily injuries per accident, and $30,000 for property damage.

When selecting insurance coverage limits, it's crucial to weigh the potential costs of an accident against your personal savings, assets, and state legal restrictions. While higher coverage limits provide better financial protection, they also result in higher insurance rates. On the other hand, lower coverage limits may lead to insufficient coverage, leaving you with hefty out-of-pocket expenses in the event of a claim.

It's important to regularly review and adjust your insurance coverage limits to keep up with life changes, such as marriage, adding a teen driver, moving to a different state, or purchasing a new home. These life changes can impact your insurance rates and may require adjusted coverage limits.

GEICO, for instance, offers a Coverage Calculator to help users understand insurance coverage and the factors to consider when selecting their limits and deductibles. This tool takes into account factors such as life changes, vehicle information, and driving habits to provide customized cost estimates and coverage suggestions. Ultimately, the level and type of coverage you choose depend on your individual needs and preferences.

Understanding Auto Insurance in Canada: A Comprehensive Guide

You may want to see also

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

![]()

Discounts and premium reductions

Additionally, GEICO offers Accident Forgiveness, which helps keep insurance rates affordable by preventing insurance rates from increasing after the first at-fault accident. This is available for qualifying drivers who have been accident-free for five years or more, although it may not apply to drivers under 21 years of age.

Furthermore, customers can save money by bundling different types of insurance, such as homeowners and car insurance. Discounts may also be available based on membership in an organization or defensive driving courses taken. Finally, customers can lower their premium by selecting a higher deductible, although this should be weighed against the ability to pay out of pocket in the event of an accident.

Auto Liability Insurance: A Savior in Hit-and-Run Scenarios?

You may want to see also

Frequently asked questions

GEICO auto insurance rates are analyzed by GEICO actuaries, who assess potential risks from statistical data. A multitude of characteristics have been proven to accurately determine the odds that someone will have an accident. Insurance rates are then determined based on an individual's combination of high and low-risk factors. You pay according to your risk of loss: higher risk = higher premium.

Actuaries aim to determine the most accurate and fair car insurance premiums. Some influences include the vehicle's safety features, the regulations in your state, age, gender, marital status, a credit-based insurance score, and prior insurance history.

The car you drive, how often you drive it, and where it is kept are all factors used to determine your rate. A car's make and model help determine expected repair costs, theft rates, and the types of safety features installed.

The more time and miles you put on your vehicle, the higher the chance you may be involved in an accident. Other items that may be considered include how long you have been driving, your driving record, and your claims history.