When you go to the hospital, you will usually provide your insurance information to the hospital staff. This allows them to bill your insurance company for the services you receive. Your insurance card contains information that the hospital will use to get paid by your insurance provider. It is standard practice for doctors to make a copy of your insurance card during your first visit. Additionally, hospitals often contract with insurance companies to become part of their network, which determines the rates at which they will be reimbursed for the care they provide. It is important to understand your insurance plan's benefits and limitations, as some plans may require you to seek treatment from specific hospitals or doctors.

| Characteristics | Values |

|---|---|

| How do hospitals know about your insurance? | You give your insurance information to the hospital when you go for care. |

| How do insurance companies know about your hospital visit? | The hospital bills the insurance company for the services you receive. |

| What information is shared? | Your insurance card contains information that the hospital will use to get paid by your insurance company. |

| What if I don't have my insurance card? | Doctors usually make a copy of your insurance card the first time you see them as a patient. |

| What if I go to an out-of-network hospital? | You may be charged more, and balance billing protections may not apply. |

Explore related products

What You'll Learn

![]()

Insurance cards

Using Insurance Cards at Hospitals:

When seeking medical care at a hospital, patients typically provide their insurance information to the administrative staff. This includes presenting their insurance card, which allows the hospital to verify coverage and determine the patient's financial responsibility for the services received. Doctors usually make a copy of the insurance card during the patient's first visit, ensuring smooth billing processes and reducing potential out-of-pocket expenses for the patient.

Network Considerations:

It is important to note that insurance companies often have networks of contracted healthcare providers, including hospitals. Seeking treatment at an in-network hospital generally results in lower out-of-pocket costs for the patient. Insurance cards help patients identify in-network hospitals and make informed choices about their care. Additionally, insurance companies may have specific requirements, such as using certain pharmacies, which can impact prescription drug coverage. Understanding these details, often outlined on the insurance card, ensures patients can maximize their benefits.

Emergency Room Visits:

In life-threatening emergencies, individuals can seek treatment at any hospital emergency room, regardless of insurance status or network participation. However, it is advisable to contact the insurance company before or after receiving emergency care to understand potential costs and coverage. The No Surprises Act, a federal law, protects individuals from unexpected out-of-network charges for emergency medical services in most cases.

Understanding Costs and Benefits:

Becoming the Commissioner of Insurance: Strategies for Success

You may want to see also

Explore related products

![]()

Emergency room visits

If you have a life-threatening medical emergency, you should go to the hospital emergency room. For instance, if you are experiencing a heart attack or are bleeding profusely from a wound, call 911 or go to the ER. You can always get treatment at an ER, regardless of your insurance status, but it may cost you more than if you went to a doctor's office or an urgent care clinic for treatment. If possible, call your insurance company before going to an ER.

When you go to the emergency room, you are protected from unexpected out-of-network charges (often called "surprise bills") for emergency medical services in most cases. If your health insurance covers emergency care, you cannot be charged more for emergency medical services than the in-network "cost-sharing" rate. However, it is important to note that some health plans do not cover emergency care.

In general, you will give your insurance information to the hospital when you go for treatment. The hospital will then bill your insurance company for the services you receive. Your insurance card proves that you have health insurance and contains information that the hospital will use to get paid by your insurance company. Doctors and hospitals often contract with insurance companies to become part of the company's "network." These contracts outline the payment the hospital will receive for the care they provide. If you go to a hospital in your insurance company's network, you will pay less out of pocket than if you go to a hospital that is not in your insurance company's network.

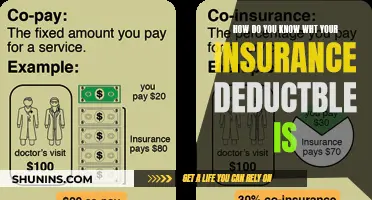

It is important to understand the costs associated with your health insurance plan. You pay a monthly premium and your cost-sharing, which is the portion of each treatment or service that you are responsible for. Most health plans also have a deductible, which is the amount of money you have to pay before your insurance will start paying for your treatment. Each insurance company has different rules for using health care benefits, so it is important to review your plan's benefits and limitations, especially if your plan requires you to receive care from certain hospitals or doctors.

Understanding Insurance Payments: Tracking and Verifying Claims

You may want to see also

Explore related products

![]()

Ambulance services

If your ambulance ride is related to a car accident, your auto insurance is likely to be your primary coverage. In this case, you won't have to pay a deductible, copay, or coinsurance. Medical payments coverage or personal injury protection (PIP) as part of your auto insurance policy will typically cover the cost of ambulance services after a car accident. Additionally, if you were not at fault for the accident and do not have MedPay or PIP, you can make a claim against the other driver's liability car insurance. Uninsured and underinsured motorist coverage (UM/UIM) can also help pay for ambulance rides if the other driver is at fault but does not have sufficient insurance.

Health insurance plans typically cover emergency transport to the nearest medical facility that can treat your condition. They may also cover non-emergency transports, such as transportation from an out-of-network hospital to the closest in-network hospital or from a hospital to a rehabilitation facility. However, ground ambulance services are often not covered by billing protections in the No Surprises Act, and you may be charged out-of-network rates. Private health insurance generally covers medically necessary ambulance rides, but you may still have to pay out of pocket, including deductibles, copays, or coinsurance. Medicare Part B also covers medically necessary ground and air ambulance transportation in certain situations, but you will be responsible for a portion of the costs.

To avoid surprise billing, it is advisable to work with an ambulance company that is in your insurance network. If you receive a surprise bill, you can check your state's laws for protections and negotiate your bill.

Navigating the Medical Billing Maze: Sending Bills to GEICO Insurance Patients

You may want to see also

Explore related products

![]()

Health plans

Most health plans have a deductible, which is the amount an individual must pay before their insurance starts contributing to the payments. The amount of the deductible and the monthly premium vary across different plans and insurance companies. It is important for individuals to understand the benefits and limitations of their specific health plan, especially regarding the network of doctors and hospitals covered by their insurance.

In the context of hospital visits, health plans can provide coverage for emergency room services and post-stabilization care. The No Surprises Act, a federal law effective from January 1, 2022, protects individuals from unexpected out-of-network bills for emergency medical services. However, it is always recommended to contact your insurance company before seeking emergency care to understand potential costs.

Additionally, health plans may have specific requirements for prescription medication coverage. While the Affordable Care Act mandates that all health plans sold to individuals or through small employers include prescription medication coverage, it is important to check with your insurance company about their specific requirements, such as using a pharmacy within their network.

Overall, health plans provide financial protection and assistance with medical costs, but individuals should be aware of the specific details, limitations, and requirements of their chosen plan to ensure they maximize their benefits and minimize unexpected expenses.

Insuring Your Mobile Phone: What You Need to Know

You may want to see also

Explore related products

![]()

Prescription medications

If you find out that your insurance provider won't pay for a prescription, you have several options. You can try generic or alternative medications, which may be more affordable. You can also explore patient assistance and manufacturer copay programs that can help you cover costs. These programs can often reduce out-of-pocket costs to $0 per month, and you can typically find them on the websites of drug manufacturers.

If you can't find a lower-cost option, your doctor may still be able to help. You can request a 90-day prescription and compare costs, as a 3-month supply may be better value than filling monthly. Your doctor can also confirm to your health plan that the medication is appropriate for your medical condition, which may allow you to get a prescribed drug that's not normally covered by your plan.

If you've explored all other options and still can't get your medication covered, you have the right to appeal the decision. You can learn more about the appeals process by contacting your insurance company or visiting their website. In urgent situations, you can request an expedited appeal, and a final decision must be made within 4 business days.

The Evolution of Insurance: Adapting to a Changing World

You may want to see also

Frequently asked questions

You can check with your insurance company to see if they require you to use a specific network of doctors and hospitals. Your insurance card should also have a phone number you can call for information.

Doctors will usually make a copy of your insurance card the first time they see you as a patient. You can also provide your insurance information to the hospital when you go for care, and they will bill your insurance company for the services you receive.

The No Surprises Act, which came into effect on January 1, 2022, protects you from unexpected out-of-network bills. If you believe you have been incorrectly billed, you can contact the No Surprises Help Desk or your insurer for assistance.