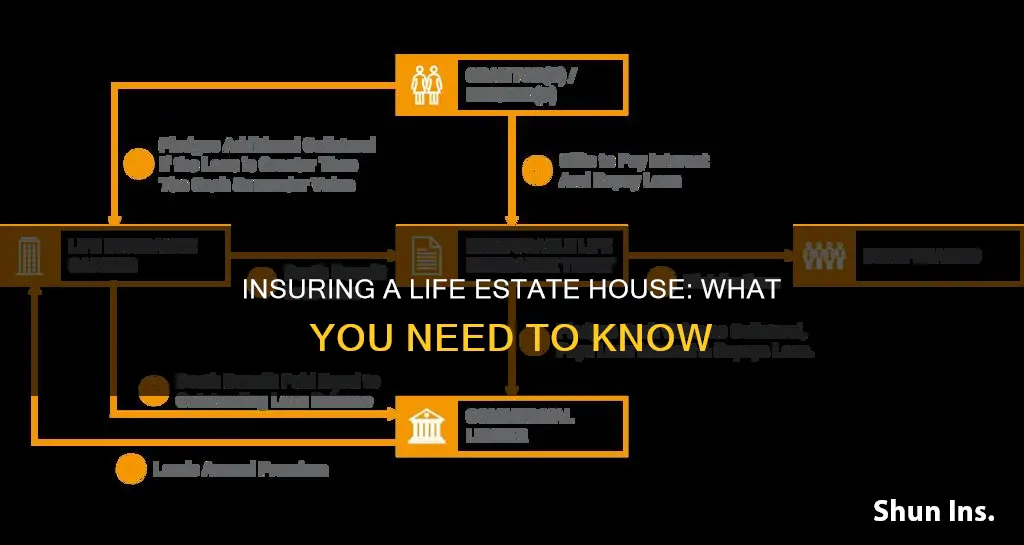

A life estate is a form of joint ownership that allows the current property owner to remain in the home until their death, at which point it passes to the other specified owner. The person who holds the life estate, called the life tenant, has full control of the property during their lifetime. They are responsible for costs such as property taxes, insurance, repairs, and maintenance and upkeep of the real estate. The life tenant retains all the rights and responsibilities of an owner except the right to sell or mortgage the property without the agreement of the remainderman.

| Characteristics | Values |

|---|---|

| Type of ownership | Joint ownership |

| Who can occupy the house | The life estate holder until their death |

| Who is the owner after the death of the life estate holder | The remainderman |

| Who is responsible for insurance payments | The life estate holder |

| Who is responsible for property tax | The life estate holder |

| Who is responsible for repairs and maintenance | The life estate holder |

| Who is responsible for real estate taxes | The life estate holder |

| Who should the insurance policy be written in the name of | The occupant |

| Who should be named in the Additional Insured Residence Premises endorsement | All the remaindermen |

Explore related products

What You'll Learn

- The life tenant is responsible for insurance payments

- The life tenant cannot sell or refinance without the remainderman's permission

- The life tenant cannot revoke the life estate without the remainderman's consent

- The remainderman should be protected with an Additional Insured Residence Premises endorsement

- The life tenant is responsible for property taxes

![]()

The life tenant is responsible for insurance payments

A life estate is a form of joint ownership that allows the current property owner to remain in the home until their death, at which point it passes to the other specified owner. The person who holds the life estate is called the life tenant, and they have full control of the property during their lifetime.

If the life tenant is no longer able to afford the upkeep and expenses, or is unable to due to physical or cognitive decline, the owners of the remainder interest may contribute their own funds.

In the case of a married couple, if one spouse still occupies the property as a life tenant, the insurance policy should be written in their name. A homeowner's policy may be issued to the occupant in this situation when the Coverage A amount is at least 80% of the property's replacement cost. Coverage A covers the physical dwelling, not the contents or liability.

Life estates can be complex, and it is recommended to consult with a knowledgeable attorney who has experience handling life estates, as well as an expert insurance broker/agent to ensure everyone involved is adequately protected with life estate coverage.

Life Insurance and Student Loans: Can They Garnish?

You may want to see also

Explore related products

![]()

The life tenant cannot sell or refinance without the remainderman's permission

A life estate is a form of joint ownership that allows one person, the life tenant, to remain in a house until their death, when it passes to the other owner(s), the remainderman. The life tenant has full control of the property during their lifetime and is responsible for maintaining the property, as well as paying property taxes and insurance. However, they cannot sell, mortgage, or refinance the property without the permission of the remainderman.

The life tenant's interest in the property ends at death, and ownership is transferred to the remainderman. The life tenant is responsible for costs such as property taxes, insurance, and maintenance, and they retain any tax benefits of homeownership. The remainderman has an ownership interest but cannot take possession until the life tenant's death.

The life tenant's inability to sell or refinance the property without the remainderman's permission is a crucial aspect of a life estate. This restriction provides protection for the remainderman, ensuring that their future ownership rights are not compromised without their consent. It also helps to maintain the value of the property, as any sale or refinancing would be subject to the remainderman's approval and could be blocked if it is not in their best interests.

Additionally, the life tenant may be able to rent out or make improvements to the property without the remainderman's consent, unless prohibited by the will, trust, or deed. However, taking out a new mortgage or otherwise encumbering the property would require the remainderman's approval. The remainderman has the right to protect their interests in the property and can file a lawsuit against the life tenant if they take any action that diminishes the property's value or attempts to sell it without consent.

In summary, the life tenant's restriction on selling or refinancing the property without the remainderman's permission is a key feature of a life estate. It ensures that the remainderman's rights are protected and helps to maintain the value of the property for the future owner.

Haemochromatosis: Life Insurance Considerations and Impacts

You may want to see also

Explore related products

$20.17 $20.17

![]()

The life tenant cannot revoke the life estate without the remainderman's consent

A life estate is a form of joint ownership that allows the current property owner to remain in the home until they die, at which point it passes to the other specified owner(s). The person who holds the life estate is called the life tenant, and they have full control of the property during their lifetime. The other owner(s) are the heirs, or remaindermen, who will inherit the property after the life tenant's death.

The life tenant has the right to use the property, rent it out, and make improvements, but they are also responsible for maintaining the property and paying property taxes and insurance. While the life tenant has control over the property during their lifetime, they cannot revoke the life estate without the consent of the remainderman. This is because the life estate creates a sort of legal joint ownership, and the remainderman has a vested interest in the property.

If the life tenant wishes to terminate the life estate or change the remainderman, they must obtain the approval of all remaindermen. This is because the life estate deed is a legal document that establishes the life tenant's right to occupy and use the property until their death. The deed also designates the remainderman as the beneficiary who will inherit the property after the life tenant's death, bypassing the probate process.

The life estate deed must be carefully drafted to include specific legal language and must be recorded in the town or city where the property is located. It is important to consult with an attorney to ensure that the deed is accurate and complies with state-specific laws and regulations.

While a life estate can provide benefits such as a simple property transfer and lifetime occupancy for the life tenant, it also has potential drawbacks. One of the main disadvantages is the lack of flexibility, as the life tenant cannot revoke or sell the property without the consent of the remainderman. Additionally, the life tenant loses some decision-making power and must obtain approval from the remainderman for major property decisions, such as alterations or sales.

Getting Life Insurance for Someone Else

You may want to see also

Explore related products

![]()

The remainderman should be protected with an Additional Insured Residence Premises endorsement

A life estate is a form of joint ownership that allows one person to remain in a house until their death, when it passes to the other owner(s). The person who holds the life estate is called the life tenant, and they have full control of the property during their lifetime. The other owners are usually heirs, known as remaindermen, who will inherit the property upon the death of the life tenant.

The remainderman has an ownership interest in the property while the life tenant is alive, and as such, has an interest in ensuring the property is not damaged, its value diminished, or the property encumbered or sold. The life tenant cannot sell or mortgage the property without the consent of the remainderman.

To protect the interests of the remainderman, an Additional Insured Residence Premises endorsement should be put in place. This is a form of insurance that covers anyone other than the policyholder. In the context of a life estate, the remainderman should be named in this endorsement, which will protect them from liability as well as possible damage or loss related to the property itself.

The Additional Insured Residence Premises endorsement can be tailored to the specific needs of the remainderman and can include coverage for defence, third-party lawsuits, and property damage. It is important to note that the endorsement may have limitations and may not cover all types of liability.

By having this endorsement in place, the remainderman can be assured that their interests in the property are protected, and they will not be held financially responsible for any issues that may arise during the life tenancy.

Life Insurance After a DUI: What You Need to Know

You may want to see also

Explore related products

![]()

The life tenant is responsible for property taxes

A life estate is a form of joint ownership that allows the current property owner to remain in the home until their death, at which point it passes to the other specified owner. The person who holds the life estate is called the life tenant, and they have full control of the property during their lifetime. The other owner is called the remainderman, and they automatically receive the title to the property upon the life tenant's death.

If the life tenant is no longer able to afford the upkeep and expenses, or is unable to due to physical or cognitive decline, the remainderman may contribute their own funds.

In the case of a life estate, the insurance policy should be written in the name of the life tenant. A homeowner's policy may be issued to the occupant in this situation when the Coverage A amount is at least 80% of the property's replacement cost. Coverage A refers to the portion of homeowners' insurance coverage that covers the physical dwelling, not the contents or liability.

Heirs (remaindermen) should protect themselves with an Additional Insured Residence Premises endorsement. This endorsement will protect the remainderman from liability, as well as possible damage or loss related to the property itself.

Universal Life Insurance: Does It Expire or Endure?

You may want to see also

Frequently asked questions

A life estate is a form of joint ownership that allows one person to remain in a house until their death, when it passes to the other owner(s). The person who holds the life estate is called the life tenant, and the other owner(s) are called the remainderman.

A life estate is typically set up to ensure that the next generation will eventually get the family home and to avoid probate, the legal process of proving a will, distributing assets, paying creditors, and settling an estate. The life tenant retains all the rights and responsibilities of an owner except the right to sell or mortgage the property without the agreement of the remainderman.

The life tenant is responsible for insurance payments and is the named insured on the policy. A homeowner's policy may be issued to the life tenant when the Coverage A amount is at least 80% of the property's replacement cost. Coverage A covers the physical dwelling, not the contents or liability.

Heirs (remaindermen) should protect themselves with an Additional Insured Residence Premises endorsement. All remaindermen should be named in this endorsement, which will protect them from liability as well as possible damage or loss related to the property itself.