Life insurance can be a useful tool to help you save for retirement, but it's important to note that it should not be your only source of income during this time. Permanent life insurance policies, such as whole life insurance, build up cash value over time, which can then be used as a source of income after retirement. This cash value is also often insulated from market risk and can provide stability and an emergency fund in times of need. Term life insurance, on the other hand, does not have a cash value component, but it is a more affordable option for those who may not be able to afford permanent life insurance. When deciding whether to incorporate life insurance into your retirement plan, it's essential to consider your current income, debt, estate plan, and the self-sufficiency of your children.

| Characteristics | Values |

|---|---|

| Purpose | Cover final expenses, pay off debts and estate taxes, fund a charitable contribution, or leave an inheritance |

| Considerations | Debt, income, family situation, estate planning |

| Types | Term life insurance, whole life insurance, universal life insurance, burial insurance |

| Tax advantages | Cash value grows tax-deferred; withdrawals up to the amount paid in premiums are not taxed |

| Disadvantages | Lower returns over time compared to other investments; may not have time to build sufficient cash value if purchased at an older age |

Explore related products

What You'll Learn

- Life insurance can be used to cover final expenses, pay off debts, and leave an inheritance.

- It can be used to fund charitable contributions

- It can be used to pay estate taxes

- Whole life insurance can be used to provide a stable source of income in retirement

- Life insurance can be used to supplement other retirement plans, such as a 401(k) or IRA

![]()

Life insurance can be used to cover final expenses, pay off debts, and leave an inheritance.

Covering Final Expenses

Final expenses can be a burden for your family when you pass away. Life insurance can help cover these costs, including funeral expenses, outstanding debts, and final income taxes. The median cost of a funeral with a burial and viewing in the US was $8,300 in 2023, while a funeral with cremation cost $6,280. Life insurance can ensure your family is not left struggling to cover these unexpected costs.

Paying Off Debts

Most debt does not disappear when you die and can become the responsibility of your estate and heirs. Life insurance can help cover these debts, including secured debt (e.g., mortgage, auto loans) and unsecured debt (e.g., credit card debt, medical bills). By having life insurance, you can protect your loved ones from inheriting these financial burdens.

Leaving an Inheritance

Life insurance is an effective way to pass money to your heirs tax-free. The death benefit is paid directly to your chosen beneficiaries, bypassing probate and ensuring they receive the funds regardless of how your estate is handled. This can provide financial security and comfort to your loved ones after your passing.

Additionally, life insurance can help equalize your estate if you have multiple heirs. For example, if you have a vacation home and one child wants to sell while the other wants to keep it, you can purchase a life insurance policy with a value equal to the home. This allows you to leave similar inheritances to your children without having to sell the property.

Life insurance can also be used to fund ongoing expenses for your loved ones, such as daily expenses or care for a child with special needs.

In summary, life insurance provides financial protection for your family by covering final expenses, paying off debts, and leaving a tax-free inheritance. It ensures your loved ones have the financial resources they need during a difficult time.

Life Event at 26: Does Insurance Coverage Change?

You may want to see also

Explore related products

$27.89 $29.99

$44.35 $74

![]()

It can be used to fund charitable contributions

Life insurance can be used to fund charitable contributions in several ways. One way is to name a charity as the beneficiary of your life insurance policy, which ensures that the charity will receive the death benefit proceeds from the policy. This method is simple and allows donors to retain control of the policy during their lifetime. However, it does not offer income tax advantages, and the charity must be prepared to wait until the donor's death to receive the benefit.

Another way to use life insurance to fund charitable contributions is to transfer ownership of the policy to a charity. This method provides the charity with immediate control of the contract and the option to surrender the policy for its cash value. The donor can also take an immediate charitable contribution tax deduction for transferring ownership. However, this decision is irrevocable, and the donor must be prepared to give up control of the policy.

Additionally, donors can gift dividends from a life insurance policy to a charity. This option allows the donor to take a tax deduction for the donated dividends while retaining ownership of the policy. However, the dividend pool is usually tied to the death benefit, so donating the dividends will reduce the total amount paid out upon the donor's death.

Finally, charitable giving riders can be attached to life insurance policies. These riders pay a specific percentage of the policy's face value to a qualified charity, although there may be limitations on the maximum gift amount. Riders are usually free and do not reduce the value of the policy. They eliminate the need to create and administer separate gift trusts.

Understanding Tax on Life Insurance Cash Surrender Value

You may want to see also

Explore related products

![]()

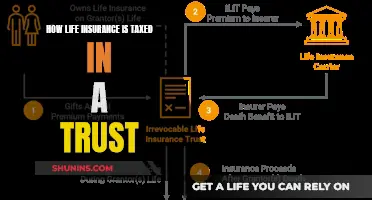

It can be used to pay estate taxes

Life insurance can be used to pay estate taxes, which is a key consideration for those with considerable assets. The proceeds from a life insurance policy can be used to pay off business debt, fund buy-sell agreements related to a business or estate, or even fund retirement plans.

However, it is important to note that unless an estate reaches a certain net worth, estate tax considerations may not apply. In the US, the threshold for federal estate taxes is $12.92 million as of 2023, increasing to $13.61 million in 2024. For those with estates below this level, life insurance may not be necessary for this purpose.

Life insurance policies that accrue "cash value" can be particularly useful for retirement planning. The cash value within a policy is the balance remaining after a portion of a premium payment is applied to insurance costs. This cash value can be withdrawn as a source of income in retirement, and provided the amount withdrawn doesn't exceed the amount paid in premiums, it is typically not subject to taxes.

Additionally, life insurance policy ownership can be transferred to another person or entity to avoid federal taxation. By transferring ownership, individuals can remove life insurance proceeds from their taxable estate. However, it is important to note that the original owner must give up all rights to make changes to the policy, and the new owner will be responsible for premium payments.

Another way to remove life insurance proceeds from a taxable estate is to create an irrevocable life insurance trust (ILIT). By transferring ownership of the policy to the trust, the individual is no longer considered the owner, and the proceeds are not included in their estate. This option allows for some legal control over the policy to be maintained and ensures that all premiums are paid promptly.

Health and Life Insurance: Licensing Requirements and Benefits

You may want to see also

Explore related products

![]()

Whole life insurance can be used to provide a stable source of income in retirement

Whole life insurance is a type of permanent life insurance that provides coverage for the entirety of the insured person's life. It also includes a savings component, known as the cash value, which functions similarly to a retirement savings account. This cash value grows tax-deferred, and the policyholder can withdraw or borrow against it. The cash value typically earns a fixed rate of interest, and withdrawals are tax-free up to the total amount of premiums paid.

Whole life insurance can be used to provide a stable source of income during retirement in several ways:

- Supplementing retirement income: The cash value of a whole life insurance policy can be withdrawn or borrowed against to supplement retirement income. This can be especially useful during market downturns or when other retirement investments are underperforming.

- Replacing assets consumed in retirement: The guaranteed death benefit of whole life insurance can be used as retirement withdrawal insurance. It allows retirees to aggressively spend down their nest egg or purchase certain annuity products that guarantee income for life, even if the principal is depleted.

- Tax advantages: Withdrawals from whole life insurance policies are often tax-free, provided they do not exceed the amount of premiums paid. This can help reduce tax burdens during retirement, especially in high tax brackets.

- Diversifying retirement portfolio: Whole life insurance policies offer a fixed rate of return on the cash value, which is not subject to market volatility. This can provide a stable source of income in retirement, regardless of market conditions.

- Long-term care: Some whole life insurance policies offer riders that provide coverage for long-term care or critical illnesses. This can help alleviate financial stress and ensure quality care in the event of a serious illness or injury.

- Pre-retirement liquidity: Whole life insurance can serve as a source of liquidity before retirement, allowing individuals to keep their longer-term reserves safely invested while maintaining access to funds for timely investment opportunities or emergencies.

Colonial Life and Constitutional Insurance: Connected?

You may want to see also

Explore related products

![]()

Life insurance can be used to supplement other retirement plans, such as a 401(k) or IRA

Life insurance can be a useful supplement to other retirement plans, such as a 401(k) or IRA, but it is not a replacement. Life insurance can provide additional financial security and help meet retirement goals, but it is important to weigh the pros and cons before including it in your retirement strategy.

One of the main benefits of using life insurance as a supplement to your retirement plans is the tax advantages it offers. The cash value of a life insurance retirement plan (LIRP) grows tax-deferred, and withdrawals or loans taken out against the policy are often tax-free, provided they do not exceed the sum of premiums paid. This can provide a valuable source of tax-free income during retirement. Additionally, the death benefit paid out to beneficiaries is usually tax-free.

Another advantage of using life insurance as a supplement is the guaranteed interest offered by most policies. Unlike 401(k) investments, life insurance policies typically offer a minimum interest rate of 0%, protecting you from losses during stock market downturns. Life insurance also offers liquidity, allowing you to access the cash value of the policy at any time, whereas early withdrawals from a 401(k) come with a 10% penalty and income taxes.

However, there are also several disadvantages to consider. Life insurance policies often come with high fees and premiums that can outweigh the benefits. The management fees for a life insurance policy are typically much higher than those of a 401(k). Additionally, the rates of return on life insurance policies tend to be lower than those of a 401(k) or IRA, which could lead to lower investment growth over time.

When deciding whether to use life insurance to supplement your retirement plans, it is important to evaluate your financial situation, goals, and other options. For most people, maximising contributions to a 401(k) or IRA should be the priority. Life insurance as a supplement may be more suitable for those who have already maxed out their contributions to these accounts or who have a high net worth and want to provide lifelong financial support to dependents.

Who Can Be Your Life Insurance Beneficiary?

You may want to see also

Frequently asked questions

Yes, you can keep your existing basic life insurance coverage if certain conditions are met. These include being enrolled in a Federal Employees' Group Life Insurance (FEGLI) program when you retire, not having converted your life insurance coverage to an individual policy, and having had life insurance coverage for the preceding 5 years (or the full periods of federal service when coverage was available).

A LIRP is a permanent life insurance policy that combines life insurance coverage with a "cash value" component that can be used for retirement income. The cash value grows over time and can be withdrawn or borrowed against, providing a tax-free income stream during retirement.

Whole life insurance offers several benefits for retirement planning. It provides permanent life insurance coverage, has fixed premiums, and allows you to build guaranteed cash value over time. The cash value can be used to supplement your retirement income or cover future expenses. Additionally, whole life insurance is insulated from market risk and provides stability to your financial portfolio.