The Affordable Care Act (ACA), often referred to as Obamacare, has significantly expanded health insurance coverage in the United States since its implementation. One of the key metrics to assess its impact is the number of newly insured individuals. Since its inception, the ACA has provided millions of Americans with access to affordable health insurance through its marketplaces, Medicaid expansion, and other provisions. Understanding how many people have gained coverage under the ACA is crucial for evaluating its success in reducing the uninsured rate and improving public health outcomes. Recent data and studies highlight substantial increases in insured populations, particularly among low-income and previously uninsured demographics, underscoring the ACA’s role in reshaping the nation’s healthcare landscape.

Explore related products

What You'll Learn

- Enrollment Growth Trends: Analyzing annual increases in ACA sign-ups since its inception

- State-by-State Coverage: Comparing newly insured numbers across different states under ACA

- Demographic Breakdown: Examining age, income, and racial groups gaining ACA coverage

- Impact of Medicaid Expansion: How expanded Medicaid programs boost ACA insured numbers

- Subsidy Effectiveness: Role of premium subsidies in increasing ACA enrollment rates

![]()

Enrollment Growth Trends: Analyzing annual increases in ACA sign-ups since its inception

Since its inception in 2010, the Affordable Care Act (ACA) has seen a steady, though not linear, increase in annual enrollments. The first open enrollment period in 2013-2014 attracted approximately 8 million sign-ups, a figure that has grown to over 14.5 million by the 2022-2023 enrollment period. This upward trajectory reflects both the expanding need for affordable healthcare and the evolving effectiveness of ACA outreach and policy adjustments. For instance, the COVID-19 pandemic prompted temporary policy changes, such as increased subsidies under the American Rescue Plan, which significantly boosted enrollment numbers.

Analyzing these trends reveals key drivers of growth. Expanded eligibility criteria, particularly in states that adopted Medicaid expansion, have played a pivotal role. States like California and New York, which embraced expansion early, consistently report higher enrollment rates compared to non-expansion states. Additionally, the ACA’s marketplace has adapted to address barriers like cost and accessibility. For example, the average premium after tax credits decreased by 4% in 2022, making plans more affordable for lower-income individuals and families.

However, enrollment growth isn’t uniform across demographics. Younger adults (ages 18-34) remain a challenging group to engage, despite their importance in balancing risk pools. Creative strategies, such as targeted social media campaigns and partnerships with colleges, have shown promise in increasing sign-ups among this age group. Conversely, older adults (ages 50-64) have consistently accounted for a larger share of enrollments, likely due to higher healthcare needs and pre-Medicare eligibility.

To sustain and accelerate enrollment growth, policymakers and advocates must focus on three actionable steps. First, simplify the enrollment process by reducing paperwork and streamlining online platforms. Second, invest in culturally competent outreach to address language and trust barriers in underserved communities. Third, maintain and expand subsidy programs that make coverage affordable for low- and middle-income households. By addressing these areas, the ACA can continue to reduce the uninsured rate and fulfill its mission of accessible healthcare for all.

In conclusion, the ACA’s enrollment growth trends highlight both its successes and areas for improvement. While annual increases demonstrate the program’s resilience and adaptability, disparities in sign-ups across demographics and regions underscore the need for targeted interventions. By learning from past trends and implementing strategic changes, the ACA can further solidify its role as a cornerstone of American healthcare.

Dialysis and Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

State-by-State Coverage: Comparing newly insured numbers across different states under ACA

The Affordable Care Act (ACA) has significantly expanded health insurance coverage across the United States, but the impact varies widely by state. Analyzing state-by-state data reveals distinct trends in newly insured numbers, influenced by factors like Medicaid expansion, population demographics, and state-level policies. For instance, states that expanded Medicaid under the ACA, such as California and New York, saw dramatic increases in coverage, with California alone adding over 5 million newly insured individuals by 2020. In contrast, non-expansion states like Texas and Florida experienced more modest gains, despite having higher uninsured rates pre-ACA. This disparity underscores the critical role of state decisions in shaping access to healthcare.

To compare these numbers effectively, consider the following steps: First, examine the percentage of the population that gained coverage rather than raw numbers, as this accounts for population size differences. For example, Kentucky, a Medicaid expansion state, saw its uninsured rate drop from 14.3% in 2013 to 5.5% in 2019, one of the largest declines nationally. Second, analyze the role of state-run marketplaces versus federal exchanges. States with their own marketplaces, like Washington and Colorado, often implemented more aggressive outreach and enrollment strategies, leading to higher coverage rates. Third, factor in demographic and economic variables, such as poverty rates and the size of the rural population, which can influence enrollment barriers.

A persuasive argument emerges when considering the economic and health benefits of higher coverage rates. States with greater ACA-driven insurance gains, such as Oregon and Nevada, have reported reduced uncompensated care costs for hospitals and improved health outcomes for low-income populations. For policymakers, this data highlights the importance of Medicaid expansion and robust marketplace support. For individuals, it emphasizes the need to leverage state-specific resources, such as local navigators or financial assistance programs, to maximize ACA benefits.

Descriptively, the landscape of newly insured numbers under the ACA is a patchwork of success stories and missed opportunities. California’s Covered California marketplace enrolled over 1.6 million people in 2020, while Texas, despite its large uninsured population, enrolled fewer than 1.1 million. Such variations reflect not only policy choices but also cultural and political attitudes toward healthcare. States with strong public health infrastructures, like Massachusetts, which had near-universal coverage pre-ACA, have built on their existing systems to further reduce uninsured rates.

In conclusion, comparing state-by-state coverage under the ACA reveals both the potential and limitations of federal healthcare reform. By focusing on Medicaid expansion, marketplace efficiency, and demographic factors, states can identify strategies to close coverage gaps. For consumers, understanding these trends can help navigate enrollment processes and advocate for policies that improve access. As the ACA continues to evolve, state-level data remains a vital tool for measuring progress and guiding future reforms.

MetLife's Employer Life Insurance: What's the Deal?

You may want to see also

Explore related products

![]()

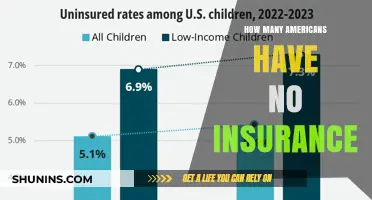

Demographic Breakdown: Examining age, income, and racial groups gaining ACA coverage

The Affordable Care Act (ACA) has significantly expanded health insurance coverage, but understanding who benefits most requires dissecting the demographics. Age plays a critical role: young adults aged 18-34, often dubbed the "young invincibles," saw a notable coverage increase due to ACA provisions like staying on parental plans until 26 and subsidized marketplace options. However, enrollment rates among this group remain lower compared to older demographics, highlighting the need for targeted outreach strategies emphasizing affordability and simplified enrollment processes.

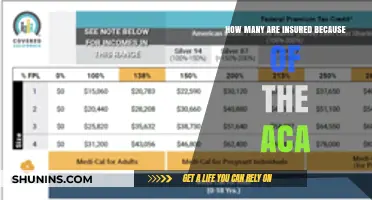

Income disparities also shape ACA coverage gains. Individuals and families with incomes between 100% and 400% of the federal poverty level (FPL) have experienced the most substantial increases in coverage, thanks to premium tax credits and cost-sharing reductions. For example, a family of four earning up to $100,000 annually may qualify for subsidies, making plans more accessible. Conversely, those just above the 400% FPL threshold often face a "coverage gap," struggling to afford marketplace plans without assistance. Policymakers must address this gap to ensure equitable access.

Racial and ethnic minorities have seen significant strides in coverage under the ACA, but disparities persist. Hispanic and Black Americans, historically underrepresented in insurance rolls, have experienced some of the largest coverage gains. For instance, Hispanic adults saw a 12 percentage point drop in uninsured rates post-ACA. However, language barriers, immigration status concerns, and systemic inequities continue to hinder full participation. Culturally tailored outreach, multilingual resources, and addressing implicit biases in healthcare systems are essential to closing these gaps.

To maximize ACA’s impact, stakeholders must adopt a data-driven, targeted approach. For young adults, leveraging social media campaigns and simplifying enrollment processes could boost participation. For low-income populations, expanding Medicaid in non-expansion states and enhancing subsidy structures would address affordability barriers. For racial and ethnic minorities, community-based initiatives and trusted messengers can improve trust and enrollment. By addressing these demographic nuances, the ACA can move closer to its goal of universal coverage.

Teen Driver with Permit: Insurance Requirements and Coverage Explained

You may want to see also

Explore related products

![]()

Impact of Medicaid Expansion: How expanded Medicaid programs boost ACA insured numbers

Medicaid expansion under the Affordable Care Act (ACA) has been a game-changer for millions of low-income Americans, significantly boosting the number of newly insured individuals. By extending eligibility to adults earning up to 138% of the federal poverty level, states that adopted expansion saw a dramatic increase in coverage rates. For example, Kentucky’s uninsured rate dropped from 14.3% in 2013 to 5.8% in 2016 after expanding Medicaid, illustrating the direct impact of this policy on ACA enrollment numbers. This expansion not only provides access to healthcare but also reduces financial barriers, as Medicaid typically offers lower out-of-pocket costs compared to private insurance plans available through the ACA marketplace.

To understand the mechanics of this boost, consider the eligibility criteria. Before expansion, Medicaid primarily served specific groups like children, pregnant women, and disabled individuals, leaving many low-income adults without coverage. Expansion bridged this gap, automatically qualifying millions for Medicaid who previously fell into the "coverage gap"—earning too much for traditional Medicaid but too little to afford private insurance. For instance, a single adult earning $18,000 annually in an expansion state qualifies for Medicaid, whereas in a non-expansion state, they would likely remain uninsured unless their employer offers affordable coverage. This shift in eligibility criteria directly correlates with the surge in ACA-insured numbers, as Medicaid enrollment accounts for a significant portion of the ACA’s overall coverage gains.

The ripple effects of Medicaid expansion extend beyond individual coverage. Hospitals in expansion states have reported substantial reductions in uncompensated care costs, as more patients have insurance to cover their medical bills. For example, a 2020 study found that expansion states saw a 39% decline in uncompensated care, freeing up resources for hospitals to improve services. This financial stability for healthcare providers indirectly supports the ACA’s goal of making healthcare more accessible and affordable for all. Additionally, expanded Medicaid has been linked to improved health outcomes, such as increased rates of diabetes management and cancer screenings, further underscoring its role in strengthening the overall healthcare system.

However, the impact of Medicaid expansion is not uniform across all states. As of 2023, 10 states have yet to expand Medicaid, leaving approximately 2 million people in the coverage gap. These individuals, often referred to as the "able-bodied poor," face limited options for affordable coverage, highlighting the disparities in ACA-insured numbers between expansion and non-expansion states. For instance, Texas, a non-expansion state, has an uninsured rate of 18%, compared to 6% in California, which expanded Medicaid early. Advocates argue that closing this gap could significantly increase the number of newly insured under the ACA, while opponents cite concerns about long-term costs and federal dependency.

In practical terms, states considering Medicaid expansion should weigh the immediate benefits against potential challenges. Federal funding covers 90% of expansion costs, making it a financially viable option for most states. Policymakers can also explore waivers to customize their programs, such as incorporating work requirements or premiums, though these modifications may affect enrollment rates. For individuals, understanding whether their state has expanded Medicaid is crucial. Residents of expansion states can apply for Medicaid through their state’s marketplace or directly through the state’s Medicaid agency, while those in non-expansion states may need to explore subsidized private plans on Healthcare.gov. By leveraging Medicaid expansion, states can play a pivotal role in maximizing the ACA’s potential to insure millions more Americans.

Securing Your Church Minibus: A Comprehensive Insurance Guide

You may want to see also

Explore related products

![]()

Subsidy Effectiveness: Role of premium subsidies in increasing ACA enrollment rates

Premium subsidies under the Affordable Care Act (ACA) have been a cornerstone in expanding health insurance coverage, particularly among low- and middle-income populations. By reducing the cost of premiums, these subsidies make health insurance more affordable for millions of Americans. For instance, during the 2021 and 2022 enrollment periods, enhanced subsidies under the American Rescue Plan Act (ARPA) led to a record-breaking 14.5 million sign-ups on HealthCare.gov, a 21% increase from the previous year. This surge highlights the direct correlation between subsidy generosity and enrollment rates, demonstrating that financial assistance is a powerful tool in bridging the affordability gap.

The effectiveness of premium subsidies lies in their ability to target specific income brackets, ensuring that those most in need of assistance can access coverage. For example, individuals earning between 100% and 400% of the federal poverty level (FPL) are eligible for subsidies, with the average subsidy amount in 2023 reducing premiums by approximately 75%. This targeted approach not only increases enrollment but also fosters a healthier risk pool by encouraging younger, healthier individuals to sign up, which is critical for the sustainability of the ACA marketplace.

However, the impact of subsidies is not without challenges. One key issue is the "subsidy cliff," where individuals earning just above 400% of the FPL face steep premium increases without assistance. This cliff effect can deter enrollment among those slightly above the eligibility threshold, creating a coverage gap. Policymakers must address this issue by either expanding eligibility or introducing tiered subsidy structures to ensure a smoother transition for those nearing the income cutoff.

To maximize the effectiveness of premium subsidies, practical steps can be taken. First, increasing awareness of subsidy availability is crucial. Many eligible individuals remain uninsured due to lack of information about their eligibility. Second, simplifying the enrollment process can reduce barriers to access. Finally, extending enhanced subsidies beyond their current expiration date would provide long-term stability and encourage sustained enrollment growth. By addressing these areas, premium subsidies can continue to play a pivotal role in increasing ACA enrollment rates and reducing the uninsured population.

Does Mastercard Quicksilver Offer Trip Insurance? Benefits Explained

You may want to see also

Frequently asked questions

Since its implementation in 2010, the ACA has helped over 20 million previously uninsured Americans gain health coverage through expanded Medicaid, the health insurance marketplace, and other provisions.

The ACA has reduced the uninsured rate significantly, with estimates showing that approximately 40-50% of the previously uninsured population has gained coverage through its programs.

Yes, a substantial portion of the newly insured under the ACA comes from states that expanded Medicaid, as this policy has provided coverage to millions of low-income individuals who were previously ineligible.