The cost of homeowners insurance depends on a variety of factors, including the location, age, size, and features of the house, as well as the coverage amount and policy structure. The average cost of homeowners insurance in the US is around $2,110 to $2,466 per year for $300,000 worth of dwelling coverage. For a $450,000 house, the average insurance cost is expected to be higher, with rates varying by location and insurance company. Homeowners insurance covers the replacement cost of the house, rather than its market value, so it is important to consider the cost of rebuilding the home when estimating insurance rates.

| Characteristics | Values |

|---|---|

| Average cost of homeowners insurance for a $450,000 house in the US | N/A |

| Average cost of homeowners insurance for a $400,000 house in the US | $3,231 a year or $269 a month |

| Cheapest insurance provider for a $400,000 house | Amica at $2,441 a year |

| Average cost of homeowners insurance for a $350,000 house in the US | $1,678 a year |

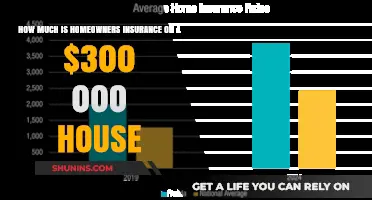

| Average cost of homeowners insurance for a $300,000 house in the US | $2,110 a year |

| National average cost of home insurance in the US | $2,466 a year or $206 a month |

| States with the most expensive average annual home insurance premiums | Nebraska, Louisiana, Florida, Oklahoma, and Kansas |

| States with the least expensive average annual home insurance premiums | Vermont, Alaska, Delaware, New Hampshire, and West Virginia |

| Average deductible amount | $500 to $2,000 |

| Typical deductible amount | $1,000 |

Explore related products

What You'll Learn

![]()

Average insurance rates for a $450,000 house

The average cost of homeowners insurance for a $450,000 house is influenced by several factors, including location, credit history, and the age and features of the house.

Home insurance rates vary by location, with some states being more expensive than others. For example, Oklahoma, Texas, Nebraska, Louisiana, and Florida are among the most expensive states for home insurance, while Vermont, Alaska, Delaware, and Hawaii are among the least expensive. The location of your home within a state can also impact the cost of insurance, with factors such as the local crime rate, the threat of natural disasters, and proximity to the coast influencing premiums.

The features of your home can also affect the cost of insurance. The age of the house, its size, the number of structures on the property, and the presence of features such as a swimming pool or trampoline can impact the premium. The cost of rebuilding your home, which is influenced by factors such as the cost of labor and supplies, can also affect insurance rates. Additionally, insurance companies consider the credit history of the homeowner, with those having poor credit histories paying more for insurance.

While the average cost of homeowners insurance in the U.S. is around $2,110 to $2,466 per year for $300,000 worth of dwelling coverage, the cost for a $450,000 house is likely to be higher. According to insurance.com, the average cost of homeowners insurance for a $400,000 house is $3,231 per year, with rates varying by location and insurance company. Amica offers the cheapest rate for this coverage amount at $2,441 per year.

It is important to note that insurance rates are not static and can fluctuate over time. Additionally, the cost of insurance for a specific property will depend on various factors, as outlined above. Therefore, it is recommended to compare rates from multiple companies and consider the coverage limits and deductibles to get a fair comparison.

Cancer Insurance and Taxes: Do You Need to Report?

You may want to see also

Explore related products

![]()

How location affects insurance rates

The cost of homeowners insurance is influenced by a variety of factors, and location is one of the most significant ones. The location of your home can affect your insurance rates in several ways. Firstly, the proximity to emergency services, such as fire stations, plays a role. Homes that are farther away from fire departments tend to have higher insurance premiums because they are at greater risk of severe damage in the event of a fire. Living in an area with a high crime rate can also increase insurance costs. Neighbourhoods with frequent burglaries or vandalism are considered high-risk, which leads to higher premiums.

Additionally, the age and construction materials of your home are factors that are often influenced by location. Older homes, particularly those with older electrical, plumbing, and heating systems, tend to be more expensive to insure. This is because these systems are more prone to issues and may need costly updates. Similarly, the materials used to build your home can significantly impact your insurance rates. Some materials may be more expensive to repair or replace, especially if they require specialized workmanship or are not readily available in your area.

Another critical aspect of location is the risk of natural disasters. If you live in an area prone to hurricanes, wildfires, floods, or earthquakes, you can expect to pay higher insurance premiums. Insurers charge more for homes in these high-risk zones because the likelihood of a claim being filed is much greater. Separate coverage for floods and earthquakes may even be required by your insurance company.

The cost of living in your area can also impact your insurance rates. In regions with a cheaper cost of living, it may be more affordable to rebuild or repair a home after a claim. Conversely, in areas with a higher cost of living, the cost of rebuilding or repairing a home may be significantly more expensive, leading to higher insurance premiums.

Finally, location can also determine the availability of insurance providers and the level of competition among them. In some states or regions, there may be a limited number of insurance companies offering coverage, which can result in higher rates due to less competitive pricing.

Mortgage Insurance: When and Why You Need It

You may want to see also

Explore related products

![]()

How to calculate insurance rates

The cost of home insurance is calculated based on a multitude of factors, and it can vary from company to company. The insurance premium for a house worth $450,000 will depend on a variety of factors, including the location, the cost to rebuild, the coverage amount, and personal factors. Here are some steps to help calculate insurance rates:

- Location and Environmental Factors: The location of your home is a significant factor in determining insurance premiums. Insurers consider the local crime rate, the threat of natural disasters, and the proximity to the coast. Environmental hazards, such as areas prone to wildfires, can also increase insurance rates.

- Dwelling Coverage: Dwelling coverage is a crucial aspect of home insurance. It refers to the cost of rebuilding your home in the event of a total loss. The dwelling coverage limit should be based on the cost of reconstruction, taking into account the home's age, size, and materials used. The dwelling coverage also sets the coverage limits for other structures on your property and personal belongings.

- Personal Property Coverage: This type of coverage protects your personal possessions in the event of damage or destruction. It typically covers items such as clothing, appliances, electronics, and furniture. The coverage amount is usually calculated as a percentage of your dwelling coverage, often ranging from 50% to 70%.

- Liability Coverage: Liability coverage protects you in case of legal or medical claims made against you. It typically starts at $100,000, but the amount can vary depending on your needs and assets. If the liability limits offered by the insurer are insufficient, you may need to purchase an umbrella insurance policy, which provides additional coverage beyond your home and auto insurance policies.

- Deductibles: The deductible is the amount you pay out of pocket before your insurance coverage kicks in. Higher deductibles often lead to lower premiums, while lower deductibles result in higher premiums. Typical deductible amounts range from $500 to $2,000, but some companies offer higher deductible options.

- Personal Factors: Your personal factors, such as credit history and claim history, can also impact your insurance rates. A higher number of claims or a lower credit score may result in higher premiums. Additionally, factors like the presence of a swimming pool or trampoline on your property can increase premiums due to higher liability risks.

- Using Calculators and Comparisons: Online calculators, such as those provided by NerdWallet, Bankrate, and Policygenius, can help you estimate insurance rates based on your ZIP code, dwelling coverage, and other relevant factors. Comparing quotes from multiple insurance providers will give you a better understanding of the rates and coverage options available to you.

While these steps provide a general guide, it's important to recognize that insurance rates can vary significantly between companies due to their unique risk assessment methods. Therefore, it's advisable to gather multiple quotes and carefully review the coverage details to make an informed decision about your home insurance policy.

Farmers Insurance Refund Policy: What You Need to Know

You may want to see also

Explore related products

$8

![]()

Insurance rates by state

The average cost of homeowners insurance in the US is between $2,110 and $2,601 per year for $300,000 worth of dwelling coverage. However, rates vary significantly by state, with some states' average rates differing by thousands of dollars.

Oklahoma is the most expensive state for home insurance, with an average rate of $5,858 per year. Other states with high average insurance rates include Nebraska, Louisiana, Florida, Kansas, and Texas. These high rates are often due to these states' increased risk of natural disasters, such as hurricanes, windstorms, and tornadoes. For example, Florida's high insurance rates are projected to be a result of the state's vulnerability to hurricanes.

On the other hand, Hawaii has the lowest home insurance rates, averaging $613 to $631 per year. Vermont, Alaska, Delaware, New Hampshire, and West Virginia are also among the states with the lowest average annual insurance premiums. These states tend to have a lower risk of natural disasters and a cheaper cost of living, making it more affordable to rebuild after a claim.

Other factors that influence insurance rates by state include the age and square footage of the home, the deductibles and policy limits chosen, and the cost of building materials.

Usaa Homeowners Insurance: Expensive but Worth the Cost?

You may want to see also

Explore related products

![]()

Discounts and ways to save on insurance

The cost of homeowners insurance is influenced by several factors, including the location, age, and square footage of the house, the deductibles and policy limits chosen, and the cost of building materials. The national average cost of home insurance is $2,466 per year for a policy with a $300,000 dwelling limit. However, rates vary across different states.

- Compare rates from different insurance companies: It is recommended to compare rates from at least three companies, ensuring that the coverage limits and deductibles are similar for an accurate comparison. Different companies offer different rates, and shopping around can help you find a better deal.

- Bundle policies: One of the simplest ways to save on homeowners insurance is to bundle your policies. Many companies offer discounts if you purchase homeowners insurance along with another policy, such as auto insurance. This is often referred to as a "multi-policy discount."

- Increase your deductible: Raising your deductible can lead to significant savings on your premiums. For example, increasing your deductible from \$1,000 to \$2,500 can save you about 12% a year on average. However, ensure you have enough cash set aside to pay the higher deductible if needed.

- Improve your credit score: Insurers use credit information to price homeowner's insurance policies. Establishing a solid credit history can help lower your insurance costs.

- Upgrade your home's security: Installing a security system and smart home devices can make your home safer and may also reduce your insurance costs. Certain insurers offer discounts for homes with security features.

- Choose a home with lower insurance risks: When buying a home, consider the cost of homeowner's insurance. Select a home that is within close proximity to a fire department and has a low risk of damage from floods, wildfires, earthquakes, or storms. A hip roof, for example, can lead to savings on your premium as it is less likely to be blown off in a storm.

Political Risk Insurance: Necessary Protection or Wasteful Expense?

You may want to see also

Frequently asked questions

The average cost of homeowners insurance in the US is $2,466 per year for $300,000 in dwelling coverage. Therefore, the cost of insurance for a $450,000 house is likely to be higher than this.

The insurance company Amica offers the cheapest rates for a $400,000 house at $2,441 per year. You can contact insurance companies directly to get a quote for a $450,000 house.

The cost of homeowners insurance varies by state. The most expensive states for homeowners insurance are Nebraska, Louisiana, Florida, Oklahoma and Kansas. The least expensive states are Vermont, Alaska, Delaware, New Hampshire and West Virginia.

The cost of homeowners insurance depends on the level of coverage you require. Liability coverage usually starts at $100,000 but can be higher depending on your needs. The higher the level of coverage, the higher the insurance premium.