Health Maintenance Organization (HMO) insurance is a type of health insurance that provides coverage through a network of physicians, hospitals, and other healthcare providers. HMOs typically require members to use only in-network doctors and obtain a referral from their Primary Care Provider (PCP) before visiting a specialist. The cost of an HMO plan depends on various factors, including the plan tier, the number of dependents, and whether it is purchased through the Affordable Care Act marketplace or an individual plan. HMO plans generally do not provide coverage for out-of-network care, except in cases of emergency or urgent care.

| Characteristics | Values |

|---|---|

| Cost | HMO plans are one of the most affordable health insurance plans available. |

| Coverage | HMO plans only cover the cost of medical services involving an in-network doctor or hospital, except for emergency care. |

| Primary Care Physician | A primary care physician (PCP) is required to coordinate your care under an HMO plan. |

| Referrals | A referral from your PCP is typically required if you need to see a specialist. |

| Network Size | HMOs cover only in-network care, limiting the number of providers and hospitals you can visit. |

| Billing | Doctors and hospitals in the HMO's network may only bill you for copayments. They may not bill you for covered services that the HMO didn't pay or only partially paid. |

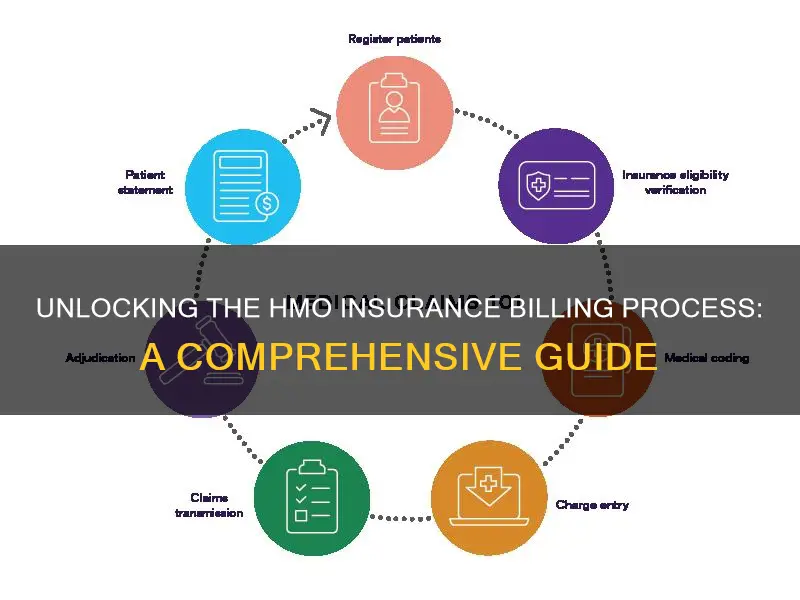

| Timely Filing Limits | Each HMO enters into an agreement with a network of providers, which may specify time limits for filing claims with the HMO. |

| Payment Timeframe | Many claims are paid electronically within a few days, but some may require a longer period. By law, a claim with complete and correct information must be paid within 30 days after it is received by the HMO. |

| Out-of-Pocket Costs | HMO plans typically offer lower out-of-pocket costs for deductibles, copays, and coinsurance when compared to other plans. |

| Premiums | HMO plans have lower premiums than other types of health insurance plans due to the network of providers agreeing to accept a certain level of payment for every service. |

Explore related products

What You'll Learn

![]()

How to choose a primary care provider (PCP)

A primary care provider (PCP) is a health care practitioner who sees patients with common medical problems and is often a patient's first point of contact for all their health issues. They are usually doctors, but they can also be physician assistants or nurse practitioners.

Determine Which Doctors Are "In-Network"

Most health plans have negotiated special, discounted rates with certain doctors and hospitals, known as "in-network" providers. Selecting an "in-network" doctor will help you avoid surprise "out-of-network" charges or having to pay in full out of pocket.

Find a Doctor with Expertise that Meets Your Health Needs

There are several types of doctors that can serve as a PCP:

- Family Practice/General Practice: These physicians can treat patients of all ages, from newborns to the elderly, and can often treat ailments that would normally require a specialist, like sports injuries or some women's health needs.

- Internal Medicine: Internal medicine physicians typically treat adults and specialize in the prevention, diagnosis, and management of diseases and chronic conditions.

- Pediatrics: Pediatricians specialize in the care of children, usually from birth until adolescence, and some may have additional specialties such as surgery or pediatric cardiology.

- Obstetrics/Gynecology: Obstetrician-gynecologists (OB-GYNs) specialize in women's health issues and may serve as PCPs, particularly for women of childbearing age.

- Geriatrics: Geriatricians often serve as PCPs for older adults with complex medical needs related to aging.

Ask for Referrals

Consider asking family, friends, colleagues, or other healthcare professionals for recommendations. You can also ask your current physician for a recommendation if you are moving to a new area and will be covered under the same insurance plan.

Think About Logistics

Consider the location of the doctor's office and whether it is convenient for you to travel to. Also, take into account the office hours and whether they align with your schedule.

Evaluate the Doctor's Office

When you visit the office, observe the cleanliness, modernity, and overall environment of the practice. Evaluate the demeanor of the staff and how efficiently and respectfully they interact with patients.

Assess Communication and Compatibility

The doctor-patient relationship is an important one, so it is crucial to select a PCP with whom you feel comfortable and can communicate openly and honestly. Consider the doctor's communication style and whether it aligns with your preferences. Additionally, think about whether you prefer a provider focused on disease treatment or wellness and prevention, and whether their treatment approach aligns with your ideals.

Consider Specialties or Areas of Interest

Every person has unique health needs, and it is beneficial to choose a PCP with areas of expertise that match your medical needs. For example, if you have a chronic condition, you may want a provider with a special interest or additional training in that area.

Research Credentials and Reviews

Check the doctor's credentials, including their qualifications, education, and experience, and whether they are board-certified in their field. You can also look for reviews from real patients to gain insights into their experiences with the doctor's care.

Remember, choosing the right PCP may take time and effort, but it is well worth it to find a provider you trust and feel comfortable with.

Exploring the Benefits: How Secondary Insurance Impacts Out-of-Pocket Costs

You may want to see also

Explore related products

![CPC Exam Prep + Medical Billing & Coding + Medical Terminology [3-IN-1]: The Unfair Advantage Career System: Pass the Exam & Get Hired | Exam Simulator, ATS Resume & Interview Kit + Custom AI Coach](https://m.media-amazon.com/images/I/61rrA2UQUaL._AC_UL320_.jpg)

![]()

When to get a referral from your PCP

When you have a Health Maintenance Organization (HMO) insurance plan, your primary care physician, or PCP, is your first point of contact for care. If you need to see a specialist, you will usually need a referral from your PCP.

In most cases, you must see your PCP first and get their approval before seeing another healthcare provider or specialist. This is called getting a referral. Your PCP will refer you to a doctor who can provide the care you need. The referral may be given electronically, on paper, or over the phone.

It is important to understand how referrals work to avoid unexpected bills. Without a referral, you may have to pay more or cover all the costs yourself.

- When your PCP cannot provide the care you need: If your PCP is unable to provide the specific treatment or service you require, they will refer you to a specialist who can. For example, if you have symptoms like a runny nose, congestion, and itchy eyes, your PCP will examine you and may refer you to an allergist if they suspect allergies.

- When you need to see a specialist: In most cases, HMO plans require you to get a referral from your PCP before seeing a specialist. The referral allows you to see another doctor within the health plan's network. Without a referral, your HMO may not cover the specialist's services.

- When you want to continue seeing a specialist you saw before enrolling in an HMO plan: If you were already seeing a specialist before signing up for an HMO plan and you wish to continue their treatment, you will need to get a referral from your PCP.

- When you change your PCP while seeing a specialist: If you decide to switch your PCP while receiving care from a specialist, your new PCP may need to issue a new referral for you to continue treatment with the specialist.

It is important to note that referrals usually have an expiration date, typically ranging from 90 days to one year from the date of issue. Make sure to see the referred doctor within this timeframe.

Additionally, there are some situations where you may not need a referral from your PCP to receive coverage:

- Medically necessary emergency treatment and urgent care: HMO plans typically cover emergency and urgent care services without requiring a referral.

- Routine care from an obstetrician-gynecologist within your plan's network: You can directly access routine women's health care, including preventive services like mammograms and Pap smears, without a referral.

- Behavioral health services from a provider within your plan's network: HMO plans usually cover behavioral health services without the need for a referral.

The Unseen Hazards: Understanding Insurance Liabilities and Their Impact

You may want to see also

Explore related products

![]()

What to do if you need to see a specialist

If you need to see a specialist, you will usually need a referral from your primary care physician (PCP). Your PCP will be your first point of contact for care, and they will refer you to a specialist if they cannot provide the care you need.

You will need a referral to see a specialist in most cases, but there are some exceptions. You won't need a referral for emergency care, and you also won't need one for routine care from an obstetrician-gynecologist, including preventive services like mammograms and pap smears. In addition, some HMOs do not require a referral to see a behavioural health specialist.

It's important to understand how referrals work to avoid unexpected bills. Getting a referral doesn't guarantee that your plan will cover all costs, and you may still need to pay a copay or meet your deductible. However, without a referral, you could end up paying more or even all of the costs.

Referrals also need to come from your current PCP if you want your plan to cover the cost of care when:

- A specialist refers you to another specialist

- You're going to see a specialist who is not in your plan's network

- You were seeing a specialist before enrolling in an HMO plan and want to continue seeing them

- You change your PCP while getting care from a specialist—your new PCP may need to issue a new referral

Referrals also have an expiration date, so be sure to see the doctor you were referred to within the time limit, which is typically between 90 days and one year.

Unveiling the VM Insurance Term: Understanding Virtual Management Coverage

You may want to see also

Explore related products

![]()

How to pay for out-of-network care

Paying for out-of-network care can be expensive, and some plans, like HMOs and EPOs, do not reimburse out-of-network providers at all. This means that you could be responsible for the full amount charged by your doctor if you choose to go out-of-network for care.

Know the Difference Between In-Network and Out-of-Network Providers

In-network providers have agreed to charge rates determined by your insurance company. When you use in-network providers, you pay a set part of the total bill, known as a copayment or coinsurance. Out-of-network providers, on the other hand, have not agreed to a contract with your insurance company and may charge higher rates for the same services. However, this doesn't mean your insurance company will pay these higher rates. They may only pay the amount they would for an in-network service, leaving you with a higher bill.

Understand Copays and Coinsurance: In-Network vs Out-of-Network

Copayments for in-network and out-of-network care can vary significantly. For example, an in-network doctor might charge $200 for an office visit, with your insurance company paying $170 and you paying the remaining $30. An out-of-network doctor, however, might charge $300 for the same visit, leaving you with a bill of $130.

Coinsurance rates also tend to be higher for out-of-network providers. For instance, you might pay 20% coinsurance for an in-network doctor visit but 30% for an out-of-network visit. Additionally, you may be responsible for the difference between the in-network and out-of-network fees.

Beware of Out-of-Network Services That Aren't Covered

Some insurance plans, like HMOs, may not cover out-of-network services at all. If you need an out-of-network specialist, you can appeal to your insurance company for an exception, but there is no guarantee it will be granted.

Carefully Compare Out-of-Network Costs

While it is possible to shop around and compare prices for services provided by out-of-network providers, it may not be worth the effort. Out-of-network costs are rising faster than in-network costs, and in most cases, in-network services will save you money.

Plan Ahead When You Can

If you know you will need to use out-of-network providers, it is essential to do your research. Use in-network providers whenever possible for non-emergency medical care and services. Compare prices between different out-of-network providers, as even in-network providers can charge different rates for the same services. Check your benefits package for information about copays, coinsurance, and out-of-network costs, and call your insurance provider with any questions.

Supplemental Insurance

If you still need care from out-of-network providers after considering your in-network options, supplemental health insurance may help with out-of-pocket expenses. Supplemental insurance can assist in paying deductibles and other costs, but it is important to purchase it in advance, as it may not provide coverage after a critical illness or injury has occurred.

The Power of Collaboration: Unlocking New Opportunities in the Insurance Industry

You may want to see also

Explore related products

![]()

Understanding timely filing limits

The timely filing limit typically ranges from 90 to 180 days from the date of service. However, some insurance companies allow for shorter or longer periods, with the shortest limit being 30 days and the longest being 720 days or two years. Medicare, for example, allows for a timely filing limit of 365 days from the date of service. It's important to note that timely filing limits may also vary for different plans within the same insurance carrier.

Healthcare providers must be diligent in submitting claims within the specified timely filing limits. If a claim is submitted after the deadline, the insurance company will deny the claim, and the provider will not receive reimbursement for those services. In some cases, insurance companies may deny claims even when submitted within the timely filing limit, and it is crucial to have a system in place to manage these situations effectively.

To find the timely filing limits for specific insurance companies, providers can refer to the insurer's website or provider manual, which contains comprehensive information about their claim submission and reimbursement processes. Additionally, creating a spreadsheet with filing limitations for the insurances in your state can be a helpful tool for tracking timely filing limits.

By understanding and adhering to timely filing limits, healthcare providers can minimize billing confusion, foster transparent communication with patients, and maintain a steady revenue stream to meet operational expenses.

The Truth About Term Insurance: Unraveling the Mystery of Surrender and Refund Values

You may want to see also

Frequently asked questions

No, but the provider can bill enrollees for copayments or coinsurance as outlined in your contract. You may also be billed for non-covered services if you agreed in advance to pay for them.

Each HMO enters into an agreement with a network of providers. The provider's contract may specify time limits for filing claims with the HMO. An enrollee cannot be held responsible for claims that a provider fails to submit to the HMO in a timely way.

Many claims are paid electronically within a few days, but in some circumstances, it requires a longer period. By law, a claim that contains complete and correct information, as requested by the HMO, must be paid within 30 days after it is received by the HMO. If it is not paid within 30 days, the provider may charge interest to be paid by the HMO.

No, to be a member of an HMO, you must live or work in its service area.

![Medical Billing & Coding for Beginners: [2 books in 1] The Ultimate Guide to Elevate from Foundation to Expertise, Build Career-Defining Skills, and Open Doors to a Prosperous and Flexible Career](https://m.media-amazon.com/images/I/710avB3cUxL._AC_UL320_.jpg)