Life insurance brokers are intermediaries between insurance companies and consumers. They help consumers navigate the complex world of insurance and find the best policies for their needs. To become a life insurance broker, you'll need to meet certain educational and licensure requirements. While the specific requirements vary by state, here's a general guide:

1. Decide on your education: While a college degree is not always required, it can be beneficial. Degrees in insurance, business, economics, or finance are relevant.

2. Complete pre-licensing requirements: This includes taking courses from the state's licensing board or an approved organization and meeting any minimum training hours mandated by your state.

3. Pass a background check: Submit your fingerprints and ensure you meet the basic eligibility requirements, such as being at least 18 years old and having no felony charges.

4. Pass the licensing exam: This exam covers state laws and insurance products.

5. Apply for a license: Submit your application, provide proof of meeting the requirements, and pay the associated fees.

6. Get an insurance broker bond: Most states require this type of surety bond to hold brokers financially accountable and protect customers.

| Characteristics | Values |

|---|---|

| Education requirements | High school diploma or minimal postsecondary coursework; a college degree in a related field is beneficial |

| Age requirement | 18 years old in most states |

| Background check | Required in most states |

| Broker exam | Required in most states |

| License | Required in all states; separate licenses may be needed for different types of insurance and for working in multiple states |

| Work environment | Can work independently or as part of an insurance brokerage firm, remotely or from an office |

Explore related products

What You'll Learn

![]()

Check your state's requirements

Each state has its own set of procedures for applying for a life insurance broker's license. While the exact procedures vary, many states require applicants to complete pre-licensing training courses, pass an exam, and submit to fingerprinting. Some states may also require a background check. It is important to review the specific requirements for the state in which you plan to operate, as they can differ significantly.

In most states, the requirements for obtaining a license will depend on whether you are a resident of the state in which you are applying, a resident of a different state, or already licensed but planning to relocate. It is crucial to carefully review the resident and non-resident requirements for your desired state.

To obtain a life insurance broker's license, you must complete an application, provide supporting documentation, and pay a fee. As a broker, you may also be asked to provide evidence of your expertise through examinations and demonstrate compliance with criminal background checks. Once you obtain your license, remember that each state will require it to be renewed periodically, typically every one to three years.

In addition to state-specific requirements, it is essential to understand the difference between major lines and limited lines of authority for insurance. The Producer Licensing Model Act (PLMA) defines six major lines, including accident and health or sickness, and variable life and variable annuity products. States may also offer limited lines, capped at nine per state, which include car rental, credit, crop, and travel insurance.

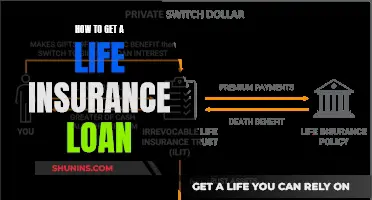

Leaving Life Insurance to a Trust: Is It Possible?

You may want to see also

Explore related products

$9.99

![]()

Complete pre-licensing requirements

To become a life insurance broker, you must meet the pre-licensing requirements. These vary depending on the state but typically include:

Complete a pre-licensing education course

Depending on your preference, you can take the subjects online or in a classroom. Each course has a minimum number of mandatory hours, typically ranging from 20 to 40 hours of instruction. The coursework covers a range of topics, including insurance industry regulations, insurance principles, and health insurance (if you plan to branch out and sell health insurance policies).

Some states may exempt prospective licensees from such requirements if they can submit evidence of relevant work experience. For example, in New York, a candidate for the broker license who has regularly been employed by an insurance company, broker, or agent for at least one year in the last three years may waive the education requirement and take the Life and Health Laws and Regulations exam.

Pass the state insurance licensure exam

Once you've finished the pre-licensing coursework, you'll need to take and pass the state licensure exam. If you're getting a life insurance license, you need to pass the Life, Accident, & Health (LA&H) test. The exam can have 50 to 200 questions and must be completed in two to three hours. The passing scores vary, but generally, you must get at least 70% correct to pass.

Provide proof of meeting pre-licensing requirements

Before taking the exam, you may need to provide proof that you have met all the pre-licensing requirements. This may include submitting your pre-licensing education certificate. Without valid proof, you may not be allowed to take the exam and may forfeit your payment.

Pass a background check

Most states require a background check as part of the pre-licensing requirements. This includes a check for any fraud or felony charges and verifying that you do not owe any federal or state income taxes. Some states also require that insurance agents and brokers do not have past-due child support.

Beneficiary Statements: Understanding Your Life Insurance Payouts

You may want to see also

Explore related products

![]()

Submit your application

Once you have completed the necessary education and pre-licensing requirements, passed a background check, and obtained an insurance bond, you are ready to submit your application for a licence. This is a crucial step in becoming an insurance broker and will allow you to start working independently or within a brokerage firm. Here is a detailed guide on submitting your application:

- Complete the requirements: Before submitting your application, ensure you have fulfilled all the necessary requirements. This includes taking the required courses, submitting your fingerprints for a background check, and passing the qualifying broker exam. Check with your state's licensing board to ensure you have met all the necessary criteria.

- Prepare the necessary documents: Gather all the required documents, including proof of completed pre-licensing requirements, proof of passing the licensing exam, and your background check results. You will also need to provide identification and residency documents, such as a driver's licence or passport, and utility bills or bank statements, respectively.

- Fill out the application form: Obtain the application form from your state's insurance licensing board or download it from their website. Carefully fill out the form, providing accurate and truthful information. Be sure to sign and date the form where required.

- Pay the associated fees: Licensing applications typically require the payment of fees, which vary by state. Check with your state's insurance licensing board to find out the cost of the application and licensing fees. These fees are usually payable through the website or by cheque or money order.

- Submit the application: Submit your completed application, along with all supporting documents and fee payments, to the relevant authority. You can usually submit your application online, by mail, or in person at the licensing office. Keep a copy of your application for your records.

- Await processing: After submitting your application, the licensing authority will review it and process your request. This process can take some time, so be patient and ensure you have submitted all the required information to avoid delays.

- Follow up: If necessary, follow up with the licensing authority to check the status of your application. They may provide you with an application number or tracking code to help you track the progress of your application.

- Receive your licence: Once your application has been approved, you will receive your insurance broker licence. Congratulations! You are now a licensed insurance broker and can start practising. Be sure to familiarise yourself with any ongoing requirements to maintain your licence, such as continuing education or renewal procedures.

Submitting your application is a significant step towards becoming an insurance broker. Ensure you carefully review the requirements and criteria set by your state's insurance licensing board to increase your chances of a successful application.

Life Insurance: Pre-or-Post Tax? Understanding the Basics

You may want to see also

Explore related products

![]()

Get an insurance broker bond

To become a life insurance broker, you'll need to meet basic eligibility requirements, get the necessary training, and meet licensure requirements. One of the key requirements to become an insurance broker in most states is to obtain an insurance broker bond.

An insurance broker bond is a type of surety bond that functions as a safeguard to protect clients' financial and personal well-being. It is a three-party agreement that protects consumers from unethical business practices, such as fraud, price manipulation, or coercion to purchase inappropriate insurance products. The three parties involved are the obligee (usually a state department of insurance or licensing), the principal/obligor (you or your company), and the guarantor (the company from which you purchase the bond).

The cost of an insurance broker bond varies depending on the state and your financial strength, typically ranging from 1-15% of the required bond amount. Most states require insurance brokers to post bonds between $10,000 and $20,000. You can obtain a quote for an insurance broker bond from companies that provide these bonds, such as SuretyBonds.com or JW Surety Bonds.

It's important to note that insurance broker bonds are not the same as insurance policies. While insurance products protect you and your company, broker bonds protect the consumer interest and the obligee. By obtaining an insurance broker bond, you are agreeing to develop lawful strategies to assist your clients and abide by the laws in the state where you practice.

Life Insurance: Pre-tax Benefits and Their Implications

You may want to see also

Explore related products

![]()

Pass the licensing exam

Passing the licensing exam is a crucial step in becoming a life insurance broker. While the specifics may vary depending on your location, here are some general guidelines to help you prepare for and pass the exam:

Understand the Exam Structure and Content:

Research the structure and content of the licensing exam for your state. The exam typically covers a range of topics related to life insurance, including insurance basics, types of policies, underwriting, policy provisions, tax considerations, and applicable regulations. It's important to familiarize yourself with the exam outline to know the areas you need to focus on.

Enroll in a Pre-Licensing Course:

Consider enrolling in a comprehensive pre-licensing course offered by reputable providers such as ExamFX or America's Professor. These courses are designed to provide you with the foundational knowledge and exam-taking techniques needed to pass the licensing exam. They offer structured learning materials, video lectures, practice tests, and support to enhance your understanding of the material.

Allocate Sufficient Study Time:

Ensure you allocate sufficient time to study for the exam. Develop a study plan that covers all the relevant topics. Dedicate time to review the material, participate in practice quizzes and exams, and seek additional resources if needed. The more time you invest in studying, the better your chances of retaining the information and performing well on the exam.

Utilize Practice Tests and Study Materials:

Take advantage of practice tests and study materials offered by your pre-licensing course provider. These resources help you become familiar with the exam format, question types, and timing. Practice tests also help you identify areas where you need further review, allowing you to focus your studies effectively. Aim to work through as many practice questions as possible to improve your understanding and exam-taking skills.

Stay Updated with Exam Changes:

Keep yourself informed about any changes or updates to the licensing exam. Exam content and requirements can evolve over time, so it's important to refer to the most current information available. Stay connected with relevant professional organizations or websites that provide up-to-date exam guidelines and resources.

Seek Additional Support:

If you find certain concepts challenging, don't hesitate to seek additional support. Reach out to your course instructors, join study groups, or connect with other candidates preparing for the same exam. Engaging with others can provide clarification on complex topics and expose you to different perspectives, enhancing your overall understanding.

Remember that passing the licensing exam is a crucial step towards becoming a life insurance broker. By following these guidelines and committing to your studies, you'll be well on your way to achieving your goal.

Max Life Insurance: Safe Investment Option?

You may want to see also