The US tax code is a complex system with many variables and considerations, and one of the key areas of complexity is the treatment of life insurance products and their tax implications. For instance, the Internal Revenue Service (IRS) outlines specific rules for different types of insurance, such as term vs. cash value or whole life, and the manner of disposition. This is further complicated by the various forms and schedules that must be completed, such as Form 1120, which includes specific instructions for corporations with interests in life insurance companies or those that are personal holding companies. One of the key considerations in this area is the distinction between the basis of a life insurance contract and the investment in the contract, which has been a subject of much discussion and litigation. Officer life insurance premiums and their placement on Form 1120S, Schedule M-2, are also affected by whether the S corporation is the policy owner and beneficiary.

Explore related products

What You'll Learn

![]()

Data entry for officer life insurance premiums

To begin the data entry process, you should identify the relevant tax form, which, in this case, is Form 1120S, also known as the U.S. Income Tax Return for an S Corporation. Within Form 1120S, Schedule M-2 is the schedule specifically designed for reporting certain adjustments, including those related to officer life insurance premiums.

In Screen Ms of UltraTax CS, you will find fields specifically dedicated to officer life insurance premiums. These fields include the "Officer life insurance premiums" field and the "Cash surrender value-officer life" field. The amounts entered in these fields are typically transferred to Schedule M-2 for further calculations.

When entering data for officer life insurance premiums, it is important to consider the tax implications. According to Rev. Rul. 2008-42, premiums paid by an S Corporation on an employer-owned life insurance contract do not reduce the S Corporation's Accumulated Adjustment Account (AAA). This is because the premiums are considered a nondeductible expense related to tax-exempt income. Therefore, when entering these premiums in Screen Ms, they should be transferred to Schedule M-2 under the "Other Adjustments Account - Other reductions" section.

Additionally, the "Cash surrender value-officer life" field in Screen Ms should be utilized for entering any cash surrender values related to officer life insurance. These values are then transferred to Schedule M-2 under the "Other Adjustments Account - Other additions" section. It is important to note that you can prevent the automatic transfer of these amounts to Schedule M-2 by leaving the corresponding fields in Screen Ms blank.

By following these guidelines, you can accurately perform data entry for officer life insurance premiums, ensuring compliance with tax regulations and proper reporting on Form 1120S.

Primerica Life Insurance: Is It Worth the Price?

You may want to see also

Explore related products

![15 Practice Sets LIC ADO Life Insurance Corporations of India Apprentices Development Officer PRE. EXAM 2019 Strictly According to Latest Exam Pattern [paperback] JBC Editorial Board [Jan 01, 2019] …](https://m.media-amazon.com/images/I/513p-q3zPpL._AC_UY218_.jpg)

![]()

Reporting life insurance transactions

To address this, the IRS designed Schedule M-2 of Form 1120S, U.S. Income Tax Return for S Corporations. This form includes the concepts of the Accumulated Adjustments Account (AAA), Other Adjustments Account (OAA), and Previously Taxed Income (PTI). However, the instructions for Schedule M-2 do not require that these columns reconcile with the corporation's retained earnings.

For example, per Rev. Rul. 2008-42, premiums paid by an S Corporation on an employer-owned life insurance contract that the corporation owns and is a beneficiary of do not reduce the S Corporation's Accumulated Adjustment Account. Similarly, the life insurance proceeds received by an S Corporation on the death of an individual who was employed by the S Corporation within the last 12 months or who is a director or highly compensated employee do not increase its Accumulated Adjustment Account.

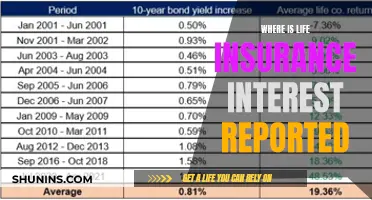

Additionally, Rev. Rul. 2009-13 illustrates how the tax treatment of dispositions of life insurance products differs based on the type of insurance (term vs. cash value, or "whole life") and the manner of disposition. Upon the surrender of a life insurance policy, income is recognized to the extent that the amount received exceeds the investment in the contract. In contrast, the amount of income recognized on the sale of a life insurance contract is the excess of the amount realized over the basis of the contract.

It is important to note that there may be discrepancies in the instructions for reporting life insurance transactions, which can lead to different presentations of similar events and incorrect answers. Therefore, it is essential to refer to the relevant sections of the tax code, such as Secs. 1367 and 1368, for accurate reporting.

Straight Life Insurance: Better Than Annuities for Longevity?

You may want to see also

Explore related products

![15 Practice Sets LIC ADO Life Insurance Corporations of India Apprentices Development Officer PRE. EXAM 2019 Strictly According to Latest Exam Pattern ... [paperback] JBC Editorial Team [Jan 01, 2019]](https://m.media-amazon.com/images/I/51LlMSYEbTL._AC_UY218_.jpg)

![]()

Life insurance tax treatment

Taxation of Life Insurance Proceeds:

Life insurance proceeds received by beneficiaries due to the death of the insured person are generally not considered part of the beneficiary's gross income and are typically exempt from income or estate taxes. However, there are certain exceptions. For example, if the payout is structured as multiple payments, those payments may be taxable. Additionally, if the life insurance proceeds are included as part of the deceased's estate and the total value exceeds the federal estate tax threshold (which was $12.92 million as of 2023), estate taxes must be paid on the excess amount.

Taxation of Interest and Withdrawals:

Interest earned on certain life insurance policies, such as annuities, can be subject to taxes. If the policyholder withdraws money or takes out a loan against the policy, the withdrawal or loan amount may be taxable if it exceeds the total amount of premiums paid. This is because the cash value of the policy can be considered a tax-free return of the principal, while any excess funds are treated as regular taxable income.

Taxation of Surrendered Policies:

When a policyowner surrenders or cancels a life insurance policy, the amount received upon surrender may be taxable. The tax consequences are governed by specific sections of the tax code, and the calculation depends on whether the policy is surrendered or sold. Upon surrender, income is recognized to the extent that the amount received exceeds the investment in the contract. On the other hand, the amount of income recognized on the sale of a life insurance contract is the excess of the amount realized over the basis of the contract.

Taxation of Employer-Owned Life Insurance:

Employer-paid group life insurance plans that pay out more than $50,000 may be taxable, according to the Internal Revenue Service (IRS). Additionally, in the case of employer-owned life insurance, the premiums paid by the employer on the policy do not reduce the Accumulated Adjustment Account (AAA) of the S Corporation. Similarly, the life insurance proceeds received by an S Corporation upon the death of an employee or director do not increase the AAA.

Reporting Life Insurance Transactions:

The reporting requirements for life insurance transactions can be complex, especially for S Corporations. Schedule M-2 of Form 1120S, designed for S Corporations, includes concepts like the Other Adjustments Account (OAA) and Accumulated Adjustments Account (AAA) that impact the tax treatment of life insurance premiums and cash surrender values. Taxpayers and preparers should carefully review the instructions and seek professional tax advice to ensure accurate reporting.

Borrowing Against Your Globe Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

S corporation ownership

S corporations are corporations that elect to pass corporate income, losses, deductions, and credits through to their shareholders for federal tax purposes. They are considered a special tax status with the IRS and offer certain tax advantages. S corps are restricted to no more than 100 shareholders, and shareholders must be US citizens or residents. They can have only one class of stock, and ownership is restricted—they cannot be owned by C corporations, other S corporations (with some exceptions), LLCs, partnerships, or trusts.

To become an S corporation, the corporation must submit Form 2553, Election by a Small Business Corporation, signed by all shareholders. S corps are subject to certain obligations imposed by the state, such as appointing and maintaining a registered agent, filing annual reports, and paying annual fees. They must also comply with requirements like adopting bylaws, issuing stock, holding initial and annual director and shareholder meetings, and keeping meeting minutes with corporate records.

S corps may have preferable self-employment taxes compared to LLCs because the owner can be treated as an employee and paid a reasonable salary. They offer limited liability protection, so shareholders (owners) are generally not personally responsible for business debts and liabilities.

Regarding life insurance, S corps must report life insurance transactions, including premiums paid and cash surrender value. These amounts are typically entered in the Officer life insurance premiums and Cash surrender value-officer life fields in Screen Ms and transferred to Schedule M-2 of Form 1120S, the US Income Tax Return for an S Corporation.

Thus, S corporation ownership involves adhering to specific tax regulations, shareholder restrictions, and compliance requirements, offering advantages such as limited liability protection and preferential self-employment taxes.

U.S.AA Life Insurance Annuity Distribution: Your Complaint Guide

You may want to see also

Explore related products

![]()

IRS Form 1120 instructions

IRS Form 1120 is the U.S. Corporation Income Tax Return form. It is used to report the income, gains, losses, deductions, credits, and to figure out the income tax liability of a corporation. Unless they are exempt under section 501, all domestic corporations, including those in bankruptcy, must file an income tax return, regardless of whether or not they have taxable income.

The form must be filed at the applicable IRS address, and if a return is filed on behalf of a corporation by a receiver, trustee, or assignee, the fiduciary must sign the return instead of the corporate officer. If an employee of the corporation completes Form 1120, the paid preparer section should be left blank. However, anyone who is paid to prepare the return must sign and complete the section, including their preparer tax information.

Form 1120 has various schedules that must be completed depending on the corporation's situation. For example, Schedule M-3 must be filed by corporations that, at any time during the tax year, had assets in or operated a business in a foreign country or a U.S. possession. Schedule O is used by a corporation that is a component member of a controlled group to report the apportionment of taxable income, income tax, and certain tax benefits between all group members. Schedule G is used to provide information about certain entities, individuals, and estates that own, directly, 20% or more, or own, directly or indirectly, 50% or more of the total voting power of all classes of the corporation's stock entitled to vote. Schedule PH is used by a personal holding company (PHC) to figure the PHC tax.

In addition, Form 1120 has specific instructions for certain line items. For instance, line 34 is for entering the penalty calculated using Form 2220, Underpayment of Estimated Tax by Corporations. If the corporation owes a penalty, it must be entered on Form 1120, page 1, line 34. If the corporation receives a notice about penalties after filing its return, it should send the IRS an explanation, and the IRS will determine if the corporation meets the reasonable-cause criteria.

Physician Life Insurance: A Necessary Safety Net

You may want to see also

Frequently asked questions

Form 1120 is a US Income Tax Return for an S Corporation.

An S Corporation is a corporation that is not the owner of the policy or a beneficiary.

If the S Corporation is not the owner of the policy or a beneficiary, the premiums paid are entered on the DED screen, line 12 as other deductions.

The amount of insurance is then automatically included in the Schedule M2 Line 2 for Column A (AAA) as ordinary income (or on line 4 if the corporation has a year loss).

The OAA, or Other Adjustments Account, is a concept invented by the IRS that has no basis or definition in the Code or regulations.