When considering whether a Health Savings Account (HSA) is better than traditional insurance, it’s essential to weigh the unique advantages and limitations of each option. HSAs, paired with high-deductible health plans (HDHPs), offer tax benefits, portability, and the ability to save for future medical expenses, making them appealing for those who prioritize long-term savings and control over healthcare spending. In contrast, traditional insurance plans typically feature lower deductibles and broader coverage, providing more immediate financial protection and predictability, which may be preferable for individuals with frequent medical needs or those seeking comprehensive care without significant out-of-pocket costs. Ultimately, the choice depends on personal health needs, financial situation, and long-term goals.

Explore related products

What You'll Learn

- Cost comparison: HSA vs. traditional insurance premiums and out-of-pocket expenses

- Flexibility: HSA’s tax advantages and investment potential versus fixed traditional plans

- Coverage scope: Preventive care, catastrophic events, and network restrictions in both options

- Long-term savings: HSA’s rollover benefits vs. traditional insurance’s annual resets

- Eligibility and suitability: HSA’s high-deductible requirement vs. traditional plan accessibility

![]()

Cost comparison: HSA vs. traditional insurance premiums and out-of-pocket expenses

Health Savings Accounts (HSAs) often come with lower monthly premiums compared to traditional insurance plans, making them an attractive option for budget-conscious individuals. For example, a 30-year-old nonsmoker might pay $200 monthly for a high-deductible HSA-compatible plan versus $350 for a traditional PPO with a lower deductible. However, this trade-off means higher out-of-pocket costs until the deductible is met. A typical HSA plan has a $3,000 deductible, while a traditional plan might cap it at $1,000. If you rarely visit the doctor, the HSA’s lower premium could save you $1,800 annually, even after accounting for occasional out-of-pocket expenses.

Analyzing out-of-pocket costs reveals a more nuanced picture. Traditional insurance plans often cover preventive care (like annual checkups) with no cost-sharing, whereas HSA plans may require you to pay these expenses until the deductible is met. For instance, a routine blood test costing $200 would be fully covered under a traditional plan but would come out of your pocket under an HSA. However, HSAs allow tax-free contributions and growth, meaning the $200 expense could effectively cost less if paid with pre-tax dollars. For someone in the 22% tax bracket, this reduces the "real" cost to $156.

A persuasive argument for HSAs lies in their long-term financial benefits, particularly for healthy individuals or those with predictable medical needs. For example, a family of four with no chronic conditions might save $2,400 annually on premiums with an HSA plan. Even if they incur $1,500 in out-of-pocket costs, they still save $900 yearly. Additionally, unused HSA funds roll over indefinitely, allowing you to build a tax-free health savings fund for future expenses, unlike traditional plans where unused benefits expire annually.

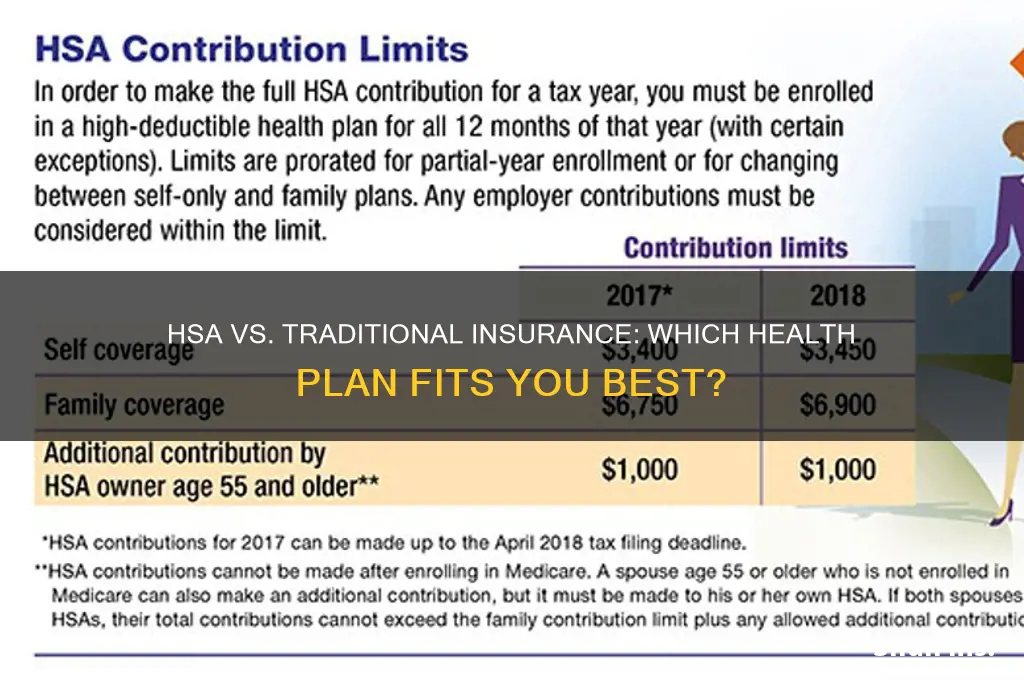

To maximize HSA benefits, consider these practical steps: first, estimate your annual medical expenses using past records. If they’re under $2,000, an HSA could save you money. Second, contribute the maximum allowed ($3,850 for individuals in 2023) to take full advantage of tax benefits. Third, pair your HSA with a high-deductible plan that covers catastrophic events, ensuring financial protection against major illnesses or accidents. Finally, use HSA funds for qualified expenses like prescriptions, dental care, or even over-the-counter medications, preserving taxable income for other needs.

In conclusion, while HSAs offer lower premiums and tax advantages, they require careful planning to manage higher out-of-pocket costs. Traditional insurance provides predictable expenses and immediate coverage for routine care but comes at a steeper monthly price. The choice depends on your health status, financial discipline, and willingness to self-insure for minor expenses. For those with low medical needs and a long-term savings mindset, HSAs often prove the better financial choice.

Protective Life Insurance: Exam-Free Option for Policyholders

You may want to see also

Explore related products

![]()

Flexibility: HSA’s tax advantages and investment potential versus fixed traditional plans

Health Savings Accounts (HSAs) offer a unique blend of tax advantages and investment potential that traditional insurance plans simply can’t match. Unlike fixed plans, HSAs allow individuals to contribute pre-tax dollars, reducing taxable income, and let earnings grow tax-free when used for qualified medical expenses. This triple tax benefit—contributions, growth, and withdrawals—positions HSAs as a powerful tool for both short-term healthcare costs and long-term financial planning. Traditional plans, while predictable, lack this flexibility, often limiting users to fixed premiums and coverage without the added benefit of investment growth.

Consider the investment potential of HSAs, a feature absent in traditional insurance. Once an HSA balance exceeds immediate needs, funds can be invested in mutual funds, stocks, or other vehicles, potentially compounding wealth over time. For example, a 30-year-old contributing $3,000 annually with a 7% annual return could amass over $300,000 by age 65, even if only half of contributions are invested. Traditional plans, in contrast, offer no such opportunity; premiums are spent on coverage, with no mechanism for wealth accumulation. This makes HSAs particularly appealing for younger, healthier individuals who can maximize investment growth while maintaining a safety net for unexpected medical expenses.

However, leveraging HSAs for investment requires discipline and a long-term perspective. It’s crucial to maintain a buffer for current healthcare costs while investing the surplus. For instance, a family of four might keep $2,000 liquid for annual deductibles and prescriptions, investing the remainder in low-cost index funds. Traditional plans, while less dynamic, provide immediate predictability—a fixed premium and known out-of-pocket maximums, which may suit those prioritizing stability over growth. The choice hinges on risk tolerance and financial goals: HSAs demand active management, while traditional plans offer passive certainty.

Practical tips can help maximize HSA flexibility. First, treat your HSA as a long-term investment account, not just a spending account. Automate contributions to take full advantage of annual limits ($3,850 for individuals, $7,750 for families in 2023). Second, pair an HSA with a high-deductible health plan (HDHP) to qualify for contributions and ensure catastrophic coverage. Finally, avoid dipping into HSA funds for non-medical expenses, as withdrawals are taxed and penalized if made before age 65. By contrast, traditional plans require no such strategy—premiums are paid, and benefits are used as needed, with no focus on long-term growth.

In conclusion, the flexibility of HSAs lies in their ability to serve as both a healthcare financing tool and an investment vehicle, thanks to unparalleled tax advantages and growth potential. Traditional plans, while reliable, lack this dual functionality, making them less adaptable to evolving financial needs. For those willing to manage their healthcare spending proactively, HSAs offer a pathway to greater financial resilience and wealth accumulation. Traditional plans remain a viable option for those seeking simplicity and predictability, but they forfeit the dynamic benefits HSAs provide. The choice ultimately depends on individual priorities: flexibility and growth versus fixed, straightforward coverage.

Mastering Secondary Insurance Write-Offs: A Step-by-Step Guide for Success

You may want to see also

Explore related products

![]()

Coverage scope: Preventive care, catastrophic events, and network restrictions in both options

Preventive care is a cornerstone of health management, and both HSAs (Health Savings Accounts) paired with high-deductible plans and traditional insurance aim to cover it, but with distinct approaches. Traditional insurance often fully covers preventive services like annual check-ups, vaccinations, and screenings (e.g., mammograms, colonoscopies) without requiring a deductible to be met first. This immediate access encourages early detection and wellness. HSAs, however, typically require policyholders to pay out-of-pocket for preventive care until the deductible is met, though recent regulations allow HSA-compatible plans to cover some preventive services upfront. For a 30-year-old individual, this means a traditional plan might cover a flu shot at no cost, while an HSA plan could require payment until the deductible (often $1,500 or more) is reached. The trade-off? HSAs offer tax advantages and long-term savings potential, but preventive care costs are front-loaded.

Catastrophic events—major illnesses, accidents, or surgeries—test the limits of any insurance plan. Traditional insurance typically caps out-of-pocket costs (around $8,000 for an individual) once the deductible and coinsurance are met, providing a predictable financial ceiling. HSAs, paired with high-deductible plans, expose individuals to higher initial costs (deductibles often exceed $2,000) before coverage kicks in. For instance, a $50,000 hospital stay under a traditional plan might cost $8,000 out-of-pocket, while an HSA plan could require paying the full deductible plus a percentage of costs until the out-of-pocket maximum (often $7,000–$8,000) is reached. However, HSAs allow tax-free withdrawals for medical expenses, and unused funds roll over annually, offering a safety net for those who can afford to save. The choice hinges on risk tolerance and financial preparedness.

Network restrictions can significantly impact care accessibility and costs. Traditional insurance plans often have narrower networks, limiting provider choices but offering negotiated rates within those networks. For example, a PPO might require staying in-network to avoid higher out-of-pocket costs, while an HMO may require a primary care physician referral for specialists. HSAs, particularly when paired with high-deductible plans, often provide more flexibility in choosing providers, both in and out of network. However, out-of-network care typically costs more, and without negotiated rates, expenses can escalate quickly. A 45-year-old with an HSA might pay $300 for an out-of-network specialist visit, compared to $50 in-network under a traditional plan. For those prioritizing provider choice, HSAs offer freedom, but traditional plans provide cost predictability within their networks.

In practice, the coverage scope of HSAs and traditional insurance reflects differing philosophies. HSAs incentivize cost-conscious decision-making and long-term savings, making them ideal for healthy individuals or those with stable finances. Traditional insurance prioritizes immediate access and cost predictability, particularly for preventive care and catastrophic events, suiting those with chronic conditions or higher healthcare needs. For a family of four, an HSA might save thousands annually in taxes and unused funds, but a traditional plan could prevent financial strain from unexpected emergencies. Ultimately, the better option depends on individual health status, financial flexibility, and willingness to manage healthcare costs proactively.

Protect Your Precious: A Guide to Insuring Diamond Engagement Rings

You may want to see also

Explore related products

![]()

Long-term savings: HSA’s rollover benefits vs. traditional insurance’s annual resets

One of the most compelling advantages of Health Savings Accounts (HSAs) over traditional insurance plans lies in their rollover benefits, which fundamentally alter the long-term savings landscape. Unlike traditional insurance plans that operate on an annual reset model—where unused funds are forfeited at the end of the year—HSAs allow unspent dollars to roll over indefinitely. This feature transforms healthcare spending into a strategic, long-term investment rather than a use-it-or-lose-it gamble. For example, a 30-year-old who contributes $3,000 annually to an HSA and uses only $1,000 per year for medical expenses could accumulate over $90,000 in tax-free savings by age 65, assuming a modest 5% annual growth rate. This compounding effect is a game-changer for individuals planning for future healthcare costs or retirement.

Consider the mechanics of this rollover benefit in contrast to traditional insurance. In a typical PPO or HMO plan, any funds allocated to a Flexible Spending Account (FSA) must be used within the plan year, often leading to rushed end-of-year spending on unnecessary medical items or services. HSAs, however, operate on a completely different principle. Funds grow tax-free, can be invested in mutual funds or other vehicles, and remain accessible for qualified medical expenses at any time. This flexibility not only encourages prudent healthcare spending but also fosters a disciplined savings habit. For instance, a family of four with an HSA could save for major expenses like braces, surgeries, or even long-term care in retirement, without the pressure of an annual deadline.

The rollover benefit of HSAs also provides a psychological edge over traditional insurance. Knowing that unused funds aren’t lost creates a mindset shift from consumption to preservation. Traditional insurance plans, with their annual resets, often incentivize overspending to avoid forfeiture. In contrast, HSAs align with long-term financial goals, making them particularly attractive for younger individuals or those in good health who may not require frequent medical care. A 25-year-old, for example, could start an HSA early in their career, allowing decades for their contributions to grow, while simultaneously reducing taxable income through pre-tax contributions.

However, maximizing the rollover benefits of HSAs requires strategic planning. First, pair your HSA with a high-deductible health plan (HDHP) to qualify for contributions. Second, prioritize funding the HSA to the annual limit ($4,150 for individuals and $8,300 for families in 2023) to take full advantage of tax benefits and growth potential. Third, invest HSA funds in growth-oriented options like index funds or ETFs, especially if you’re decades away from retirement. Finally, resist the temptation to spend HSA funds on non-essential medical expenses early on; instead, pay out-of-pocket for minor costs and let the account grow.

In conclusion, the rollover benefits of HSAs offer a clear advantage over traditional insurance’s annual reset model, particularly for long-term savings. By eliminating the use-it-or-lose-it pressure and enabling tax-free growth, HSAs empower individuals to build substantial healthcare reserves. Whether you’re planning for future medical expenses, retirement, or simply seeking a tax-efficient savings vehicle, the rollover feature of HSAs makes them a superior choice for those with a long-term financial horizon.

Navigating Insurance Coverage for Hormone Therapy: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Eligibility and suitability: HSA’s high-deductible requirement vs. traditional plan accessibility

Health Savings Accounts (HSAs) are only available to individuals enrolled in a high-deductible health plan (HDHP), which in 2023 requires a minimum deductible of $1,500 for self-only coverage or $3,000 for family coverage. This eligibility criterion immediately narrows the pool of potential HSA users, as it excludes those who cannot afford or are unwilling to shoulder such high out-of-pocket costs before insurance kicks in. Traditional insurance plans, on the other hand, often have lower deductibles, making them accessible to a broader population, including those with chronic conditions or families with frequent medical needs. For example, a 35-year-old with diabetes might find an HDHP’s high deductible prohibitive, opting instead for a traditional plan with a $500 deductible that covers insulin and regular check-ups from day one.

Consider the suitability of HSAs through a comparative lens: while the high-deductible requirement may deter those with immediate or predictable medical expenses, it positions HSAs as a strategic tool for healthy individuals or those with sufficient emergency savings. A 28-year-old with no pre-existing conditions and a stable income might view the HDHP’s lower premiums as an opportunity to save on monthly costs, funneling the difference into an HSA for tax-free growth. Conversely, traditional plans offer predictability and immediate coverage, making them more suitable for individuals with known health risks or those who prioritize peace of mind over potential long-term savings.

From a practical standpoint, determining eligibility and suitability involves a three-step process: first, assess your annual healthcare expenses, including prescriptions, specialist visits, and preventive care. Second, compare the total out-of-pocket costs of an HDHP (deductible plus out-of-pocket maximum) to those of a traditional plan. Finally, evaluate your financial resilience—can you afford to pay the HDHP’s deductible if an unexpected medical issue arises? For instance, a family of four with annual medical expenses of $2,000 might find an HDHP with a $3,000 deductible too risky, whereas a single professional with $500 in yearly expenses could benefit from the lower premiums and HSA tax advantages.

A persuasive argument for HSAs lies in their long-term potential as both a healthcare and retirement savings vehicle. Contributions are tax-deductible, grow tax-free, and can be withdrawn tax-free for qualified medical expenses at any time. For those who rarely meet their deductible, the HSA becomes a triple-tax-advantaged investment account. However, this benefit hinges on the ability to meet the HDHP’s high deductible without financial strain. Traditional plans, while lacking these investment perks, provide immediate accessibility and are often paired with employer contributions, reducing overall costs for employees.

In conclusion, the HSA’s high-deductible requirement is both a barrier and a benefit, depending on individual health status, financial stability, and long-term goals. Traditional plans offer accessibility and immediate coverage, making them a safer choice for those with ongoing medical needs or limited savings. HSAs, however, reward those who can navigate the HDHP’s upfront costs with significant tax advantages and investment potential. The key lies in aligning your choice with your current health, financial situation, and future priorities.

Life Insurance Payout: How Long Are the Checks Valid?

You may want to see also

Frequently asked questions

An HSA (Health Savings Account) is a tax-advantaged savings account paired with a high-deductible health plan (HDHP). Unlike traditional insurance, which typically has lower deductibles and copays, an HSA allows you to save pre-tax dollars for medical expenses and invest the funds for potential growth.

An HSA can be better for long-term savings because contributions are tax-deductible, grow tax-free, and can be carried over indefinitely. Traditional insurance, while offering more immediate coverage, does not provide the same tax advantages or investment potential.

Yes, you can use an HSA if you have a pre-existing condition, as long as you are enrolled in a qualifying high-deductible health plan (HDHP). The HSA itself is not dependent on your health status but on your insurance plan type.

Yes, HSAs offer more flexibility because you can use the funds for qualified medical expenses at any time, invest the money for growth, and even use it in retirement for non-medical expenses (though taxes may apply). Traditional insurance plans typically restrict how and when you can use benefits.

An HSA can be an excellent option if you rarely visit the doctor because it allows you to save money tax-free for future medical expenses while paying lower premiums for a high-deductible plan. Traditional insurance might be less cost-effective in this scenario due to higher premiums for broader coverage.