Life insurance proceeds are often overlooked when calculating estate tax. Even if the benefits are paid to a third party, they are still considered part of the estate for tax purposes. According to IRC Section 2042, the term insurance means life insurance of every description. There are, however, ways to ensure that life insurance benefits are not included in the estate and are therefore not subject to estate tax. Proceeds are typically included in the gross estate when they are payable to the insured's estate or for its benefit, or when the insured has incidents of ownership in the policy at the time of death.

Explore related products

What You'll Learn

![]()

The beneficiary of the insurance proceeds

When the beneficiary is not the spouse, the proceeds are still included in the gross estate if the decedent possessed "incidents of ownership" at the time of death. Incidents of ownership refer to the practical power to control or influence the policy, such as the ability to change beneficiaries, surrender or cancel the policy, borrow against the policy, or withdraw policy dividends. If the decedent had such power, then the entire value of the insurance proceeds is typically taxed and included in the insured's estate.

It is important to note that the definition of life insurance for estate tax purposes has specific criteria. The policy must be considered a life insurance contract under applicable state law, and its cash value must not exceed the net single premium cost for the coverage provided. Additionally, the premiums must not go beyond a guideline premium limitation, and the benefits must fall within the "cash value corridor," meaning the benefit amount cannot be less than a certain percentage of the specified cash value range.

In summary, the beneficiary of the insurance proceeds can vary depending on the circumstances. If the beneficiary is the spouse, they are typically treated as a joint owner, and only half of the proceeds are taxable. If the beneficiary is someone other than the spouse, and the decedent had control over the policy, the full amount of the proceeds is usually included in the gross estate and taxed accordingly.

Life Insurance: Is a $100,000 Payout Enough?

You may want to see also

Explore related products

![]()

Incidents of ownership

A person (including a trustee) has incidents of ownership if they have the right to change beneficiaries on a life insurance policy, to borrow from the cash value, or to change or modify the policy in any manner. This occurs even if the person chooses not to act on it and even if they don't borrow from the policy. Simply having the ability to do so gives the insured person incidents of ownership.

The question of incidents of ownership is relevant when determining tax responsibility in cases where a person gifts a life insurance policy to another person or entity. When transferring a policy, the original owner must forfeit all legal rights and must not pay the premiums to keep the policy in force. If the insured or transferor dies within three years of the date of the policy transfer, the life insurance proceeds will be included in the gross value of the original owner's estate (as per the three-year rule).

Proceeds of life insurance policies on the decedent's life are includable in the gross estate if the proceeds are payable to the decedent's estate or for its benefit. This is also the case if the proceeds are payable to any other beneficiary, but only if the decedent possessed incidents of ownership in the policy at the time of death. This includes the practical power to control the existence of the policy, rearrange the economic interests, or affect the benefits payable.

The term "incidents of ownership" is not limited in its meaning to ownership of the policy in the technical legal sense. It generally refers to the right of the insured or their estate to the economic benefits of the policy. This includes the power to change the beneficiary, surrender or cancel the policy, assign the policy, revoke an assignment, pledge the policy for a loan, or obtain a loan against the surrender value of the policy, among other things.

Additionally, incidents of ownership include a reversionary interest in the policy or its proceeds, whether arising from the express terms of the policy or other instruments, or by operation of law. This is only the case if the value of the reversionary interest immediately before the death of the decedent exceeded 5% of the policy's value.

Life Insurance: AmFam's Comprehensive Coverage for Peace of Mind

You may want to see also

Explore related products

$252 $252

![]()

Community property funds

In the US, there are nine community property states: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin. In addition, Puerto Rico is a community property jurisdiction. In these states, property accumulated during marriage is to be split equally between both partners in the event of a divorce. However, property owned by either spouse before marriage or after separation is considered separate property.

Community property laws apply to life insurance policies depending on various factors, such as when the policy was purchased and how the premiums were paid. If the insurance was paid for with funds acquired during the marriage or with community property assets, then the insurance is considered community property. If the insurance was purchased prior to the marriage, then the benefits could be prorated based on the length of the marriage.

For example, if a couple uses community funds to purchase a policy and the insured spouse dies, one-half of the proceeds will be included in the insured’s federal gross estate. If the insured spouse dies owning the policy and names their probate estate as the beneficiary, the insured’s executor receives the full amount of the policy proceeds, but only one-half is includable in the insured’s gross estate. The surviving spouse has a legal claim to one-half of the proceeds under community property principles, as this half is deemed to belong to them.

A strange situation can occur when community funds are used to purchase a policy and the surviving spouse is not made the beneficiary of the full proceeds. In this case, although one-half of the proceeds are includable in the deceased spouse’s federal gross estate, the surviving spouse may have made a gift of their half of the proceeds to the named beneficiary.

Community property laws also apply to the cash value portion of a permanent life insurance policy since it counts as an asset. The cash value can be used during divorce proceedings, but the agreement of both spouses or court approval may be needed, depending on the state.

Life Insurance and Drug Overdoses: What's the Verdict?

You may want to see also

Explore related products

![]()

Buy-sell agreements

A buy-sell agreement is a legally binding contract that outlines how a partner's share of a business may be reassigned if that partner dies or leaves the business. It is also known as a buyout agreement, business will, or business prenup.

Life insurance policies are commonly used to fund a potential buyout in the event of a partner's death. Each partner takes out a life insurance policy on the lives of the others, with the partners named as beneficiaries. Upon the death of a partner, the life insurance death benefit is paid out to the remaining partners, who use the funds to purchase the deceased's shares from their estate. This ensures business continuity and prevents legal battles for control with surviving spouses or children.

There are two common types of buy-sell agreements:

- Cross-purchase agreement: The remaining owners or partners purchase the share of the business that is for sale.

- Entity-purchase agreement (redemption agreement): The business entity itself buys the deceased's share of the business.

Some key considerations for a buy-sell agreement include:

- A list of partners or owners and their current equity stakes

- A recent business valuation to determine the value of each partner's interest

- Events that trigger a buyout, such as death, disability, bankruptcy, or retirement

- A breakdown of who buys and acquires what

- How the buyout will be funded, e.g. via insurance policies

- Tax and estate planning considerations for partners and beneficiaries

It is important to work with an attorney, certified public accountant, and a life insurance professional when crafting a buy-sell agreement. While buy-sell agreements offer many advantages, there are also some disadvantages, such as making it harder for owners to sell their interests to those not mentioned in the agreement and the potential for the purchase price to become outdated.

Understanding Tax Implications of Life Insurance Cash Surrender

You may want to see also

Explore related products

![]()

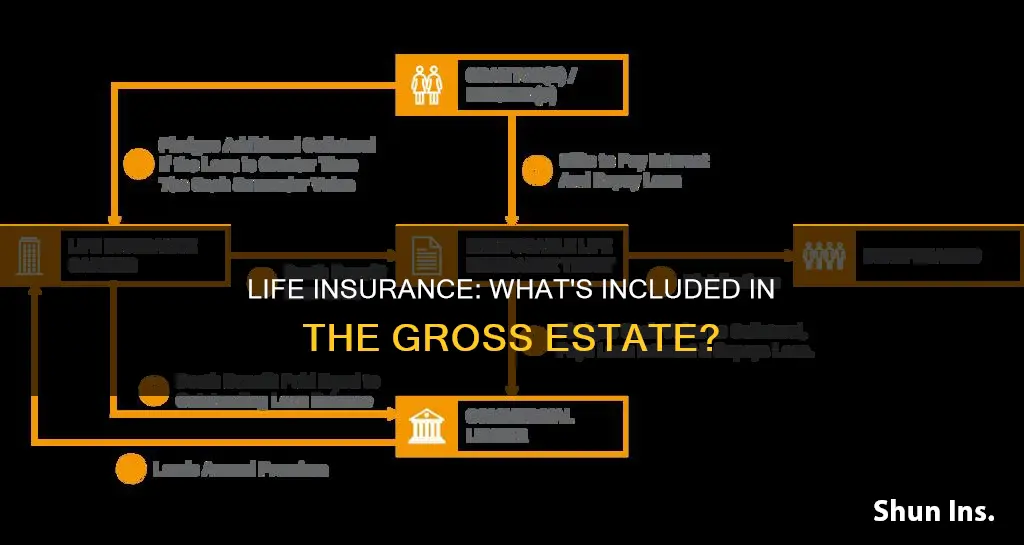

Life insurance trusts

There are three key parties involved in a life insurance trust: the grantor (creator of the trust), the trustee (who manages the trust and pays insurance premiums), and the beneficiary/beneficiaries (who will receive the assets). The trust itself is the primary beneficiary of the life insurance proceeds, and the grantor must name an independent trustee to take advantage of any estate tax savings.

There are a few important considerations to keep in mind. Firstly, the trust must be irrevocable, you cannot be the trustee, and the trust must exist for at least three years before your death. Secondly, if you die within three years of transferring your policy to the trust, the Internal Revenue Service will consider the trust invalid, and the value of the policy will be included in your estate. Lastly, there may be gift tax concerns relating to Crummey withdrawal powers, which you should discuss with a legal professional.

Whole Life Insurance: Better Investment Option than Bonds?

You may want to see also