In the United States, it is not illegal to not bill insurance. In fact, patients can opt out of filing their health insurance, as long as they pay their healthcare provider in full. However, there are laws in place to protect patients from surprise medical bills, such as the No Surprises Act, which came into effect on January 1, 2022, and California's legislation, which came into effect on July 1, 2017. These laws protect patients from being billed for out-of-network costs when they receive care at an in-network facility.

| Characteristics | Values |

|---|---|

| Is it illegal to not have health insurance? | No federal law makes health insurance a legal requirement. However, some states require citizens to obtain coverage or pay a tax penalty. |

| What is a surprise medical bill? | An unexpected bill from an out-of-network provider or facility. |

| What is a good faith estimate? | A list of expected charges before you get healthcare items or services. |

Explore related products

What You'll Learn

![]()

Patients can opt out of insurance, but must pay in full

Patients can choose to opt out of using their health insurance, but they must pay in full. This is thanks to HIPAA/HITECH regulations, which allow patients to opt out of filing their health insurance. This is particularly useful for patients with high deductibles, as they may find that it is more affordable for them not to file their insurance.

In these cases, patients should sign an "Election to Self-Pay" form, which outlines the process. This form confirms that the patient has chosen to opt out of their insurance, and that the healthcare provider will not be filing a claim with their insurance company. If the patient were to file a claim on their own, there is no guarantee it will apply towards their deductible since they chose not to use their insurance.

It's important to note that this does not apply to Medicare patients. Doctors should not force or require patients to opt out of filing their insurance as a condition of treatment, but patients should be aware of the regulations that permit opting out.

Additionally, it's recommended that patients and healthcare providers review their insurance provider agreements, as there may be specific requirements or restrictions related to opting out of insurance.

Navigating Cobra Insurance: A Guide to Submitting Doctor Bills

You may want to see also

Explore related products

![]()

No federal law makes health insurance mandatory

Although there is no federal mandate, some states have implemented their own health insurance requirements. Certain states have individual mandates in place, requiring residents to obtain health insurance or face tax penalties. These states include California, Massachusetts, New Jersey, Rhode Island, Vermont, and Washington, D.C. The specifics of these mandates and penalties vary by state, so it is essential to check the regulations in your specific state to understand your legal obligations and potential consequences.

The importance of having health insurance cannot be overstated. While going without health insurance may save you money in the short term, it could put you at significant financial risk if you face unexpected medical expenses due to illness or injury. Health insurance provides financial security and access to essential medical care, helping individuals and families manage healthcare costs and promoting overall well-being.

The Intricacies of PIP Insurance: Unraveling the Benefits and Its Vital Role in Road Safety

You may want to see also

Explore related products

![]()

The No Surprises Act protects against surprise billing

Surprise medical bills are unexpected bills from an out-of-network provider or facility. They often occur after an accident or sudden illness, and consumers are rarely informed of the costs of medical treatment before emergency treatment. The No Surprises Act (NSA) is a federal law that went into effect on January 1, 2022, to protect consumers from surprise medical bills.

The NSA protects people covered under group and individual health plans from receiving surprise medical bills when they receive most emergency services, non-emergency services from out-of-network providers at in-network facilities, and services from out-of-network air ambulance service providers. It establishes an independent dispute resolution process for payment disputes between plans and providers and provides new dispute resolution opportunities for uninsured and self-pay individuals when they receive a medical bill that is substantially greater than the good faith estimate they get from the provider.

The NSA requires private health plans to cover out-of-network claims and apply in-network cost sharing. It prohibits doctors, hospitals, and other covered providers from billing patients more than the in-network cost-sharing amount for surprise medical bills. A penalty of up to $10,000 for each violation can be applied. The NSA also establishes a process for determining the payment amount for surprise, out-of-network medical bills, starting with negotiations between plans and providers and, if negotiations don't succeed, an independent dispute resolution (IDR) process.

The NSA also fills in gaps left by existing state-law protections, including key areas where other federal laws preempt state actions. The federal Employee Retirement Income Security Act of 1974 (ERISA) prohibits states from adopting surprise-billing protections for consumers in self-funded plans, though a few states allow self-funded plans to opt into state protections. Additionally, the Airline Deregulation Act blocks states from enacting effective protections for those using air ambulance services. The NSA establishes nationwide protections in both of these circumstances.

The NSA also offers protections for post-stabilization services administered after an emergency patient has been medically stabilized, as well as for facilities omitted from certain state laws (like critical access hospitals in Nevada) and excluded medical services (such as non-surgical, non-emergency services provided in Virginia facilities).

In conclusion, the No Surprises Act is a comprehensive federal law that protects consumers from surprise medical bills by addressing various scenarios, filling gaps in state-law protections, and establishing a process for resolving payment disputes.

The Mystery of Discontinuance: Unraveling the Insurance Terminology

You may want to see also

Explore related products

$82.49 $92.95

$15.99 $15.99

$112.62 $245.95

![]()

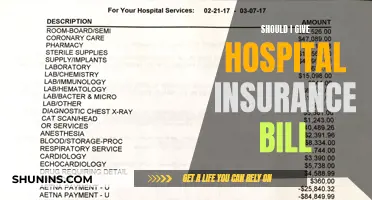

Patients can dispute bills over $400 more than the estimate

The No Surprises Act, which came into effect on January 1, 2022, protects patients from unexpected out-of-network medical bills. Under this Act, patients who don't have health insurance or choose not to use it are entitled to a "good faith estimate" of their expected charges before receiving care. This estimate is provided by the healthcare provider or facility when the patient schedules care at least three business days in advance or upon request.

If a patient receives a bill that is at least $400 more than the good faith estimate, they may be able to dispute the charges through the patient-provider dispute resolution process. This process involves an independent third-party reviewer who examines the good faith estimate, the final bill, and any other relevant information to determine an appropriate payment amount. It is important to note that the dispute must be initiated within 120 days of receiving the initial bill, and a $25 non-refundable administrative fee is required to start the process.

During the dispute process, the healthcare provider is restricted from taking certain actions, such as moving the bill into collections or threatening to do so. If the patient and provider reach an agreement on the payment amount before the dispute resolution is finalized, the provider must notify the third-party reviewer. It is worth noting that the dispute resolution process is not applicable if the patient used health insurance.

In addition to federal protections, some states like New York have implemented their own laws to protect consumers from surprise medical bills. For instance, New York consumers are safeguarded from surprise bills when treated by an out-of-network provider at an in-network hospital or ambulatory surgical center within their health plan's network.

To summarize, patients have the right to dispute bills that exceed the good faith estimate by $400 or more through the patient-provider dispute resolution process. This process is designed to protect patients from unexpected charges and ensure fair payment determinations.

Understanding the Personal Articles Floater: Customized Insurance for Your Prized Possessions

You may want to see also

Explore related products

![]()

Balance billing is prohibited in some states

Balance billing is the difference between a healthcare provider's charge and the amount allowed by the insurance company based on your policy. It is a common occurrence when visiting out-of-network providers, who are not subject to the terms and rates set by providers who are in-network. However, in some states, balance billing is illegal, meaning you do not have to pay the balance if you visit an in-network provider that accepts your insurance and your policy covers the services rendered.

Balance billing is prohibited in the following states:

- California: In California, a law protects consumers who use in-network hospitals or other health facilities from being charged with surprise bills after receiving care from a provider who has not contracted with their insurer. In these scenarios, the patient is only responsible for the copayment owed or other cost-sharing expenses that they would have normally paid if they had seen an in-network provider. This law applies to both emergency and non-emergency services.

- Connecticut: According to Connecticut's law No. 15-146, which took effect on July 1, 2016, patients who receive surprise bills from their health insurer for out-of-network services performed at an in-network facility are only responsible for paying the co-payment, co-insurance, deductible, or other out-of-pocket expenses that would typically apply.

- Florida: Florida law outlines a process in which healthcare providers and insurance companies can work out billing disputes without putting patients under additional financial strain. If a patient in Florida is seen by an out-of-network provider at an in-network hospital, the law states that the patient is only responsible for paying the provider the in-network fee. It is then the responsibility of providers and insurance companies to negotiate the remainder of the fees.

- Illinois: The Illinois Balance Billing Law brings relief to patients who receive services at an in-network hospital or ambulatory surgery center. The law prohibits out-of-network facility-based providers from billing patients for expenses other than the deductible and copay that they would have normally paid if they had seen an in-network provider. Out-of-network providers must accept the fee negotiated with the insurance company, and the patient is not involved in this process.

- Maryland: In Maryland, healthcare providers are prohibited from performing balance billing on HMO consumers for covered services such as emergency services. HMOs must also hold patients harmless for covered services provided by out-of-network providers and provide payments at a prescribed rate. PPO laws also grant protections to patients who assign benefits to their physicians.

- New Hampshire: The state of New Hampshire enacted a law in July 2018 to prevent out-of-network health providers who perform services in in-network hospitals or ambulatory surgical centers from sending balance bills to patients. This law aims to protect consumers by preventing healthcare providers and insurance companies from holding patients responsible for balance bill charges.

- New York: New York was the first state to enact a balance billing law, which protects patients from the financial responsibility of surprise bills. Under this law, patients are not required to pay out-of-network provider charges for out-of-network services that are higher than the patient's in-network deductible, copayment, or coinsurance rate.

- Oregon: In March 2018, Oregon passed a law protecting citizens from having to pay surprise out-of-network medical bills from providers not chosen by the patient. This law also requires out-of-network healthcare providers to inform patients of their increased financial responsibility.

While the above states offer comprehensive protection against balance billing, other states have a more limited approach. For example, in Mississippi, a state law prohibits balance billing, but providers are not penalised for doing so in practice. Additionally, Congress is working on legislation that may change how balance billing is handled, focusing on reducing the power given to insurance companies.

Risk Mitigation: Strategies for Hazard Elimination in Insurance Policies

You may want to see also

Frequently asked questions

No, it is not illegal to not bill insurance. However, if you don't have insurance or choose not to use it, you will be required to pay your healthcare provider in full.

A good faith estimate is a list of expected charges before you receive healthcare services. It is not a bill, but rather an estimate of how much your care will cost.

You can get a good faith estimate when you schedule care at least 3 business days in advance or if you ask your provider for one.

A good faith estimate should include expected charges for healthcare items and services, including facility and hospital fees.

If you receive a bill that is at least $400 more than the good faith estimate, you may be able to dispute the charges. You can use the new dispute resolution process to determine the final payment amount.