Medigap, also known as Medicare Supplement Insurance, is a type of health insurance sold by private insurance companies to fill the gaps in Original Medicare Plan coverage. It helps cover out-of-pocket costs, such as deductibles, copays, and coinsurance, that are not covered by Medicare Parts A and B. Medigap policies are standardized and must follow federal and state laws, providing the same benefits regardless of the insurance company. Individuals typically need to have Original Medicare Part A and Part B to purchase a Medigap policy, and separate policies must be purchased for spouses. Medigap plans are available in all 50 states and Washington, D.C., with varying premiums and enrollment eligibility.

| Characteristics | Values |

|---|---|

| Type of Insurance | Medicare Supplement Insurance |

| Who sells it | Private insurance companies |

| Who can buy it | People with Original Medicare Plan (Part A and Part B) |

| What it covers | Healthcare costs not covered by Medicare, including deductibles, copays, and coinsurance |

| Where it's accepted | Anywhere that Medicare is accepted, with some plans covering foreign travel emergency services |

| Renewal | Guaranteed renewable as long as premiums are paid |

| Spouse coverage | Each spouse must buy a separate policy |

| Availability | Available in all 50 states and Washington, D.C., but specific plans may vary by area |

| Discounts | Discounts vary by state and insurance company |

Explore related products

What You'll Learn

- Medigap is extra insurance to cover out-of-pocket costs not covered by Original Medicare

- Medigap policies are sold by private insurance companies

- Medigap policies are standardized, meaning they must provide the same benefits

- Medigap policies are guaranteed renewable as long as premiums are paid

- Medigap plans cover foreign travel emergency services

![]()

Medigap is extra insurance to cover out-of-pocket costs not covered by Original Medicare

Medigap, also known as Medicare Supplement Insurance, is extra insurance that covers out-of-pocket costs not covered by Original Medicare (Parts A and B). Medigap policies are sold by private insurance companies and help fill the "gaps" in Original Medicare coverage. Generally, individuals must have Original Medicare (Part A and Part B) to purchase a Medigap policy. Medigap plans are available in all 50 states and Washington, D.C., with some variations in premiums and enrollment eligibility. These plans typically have no network limitations and are available anywhere that accepts Medicare.

Medigap policies help pay for healthcare costs such as deductibles, copays, and coinsurance that Original Medicare does not cover. The policies offered by different insurance companies must provide the same benefits, with the only difference usually being the cost. Individuals can compare Medigap policies to find the one that best suits their needs and budget. It is important to note that Medigap policies do not cover any healthcare costs for a spouse, and separate policies must be purchased for each individual.

Medigap policies are guaranteed renewable as long as the premiums are paid. This means that the policy will automatically renew each year, and coverage will continue as long as the premiums are up to date. However, there may be some exclusions and limitations to Medigap coverage, and individuals should carefully review the policy details before purchasing. Additionally, Medigap plans may offer additional benefits, such as foreign travel emergency services, which can provide valuable peace of mind when travelling.

Overall, Medigap insurance is a valuable option for individuals seeking to supplement their Original Medicare coverage and reduce their out-of-pocket expenses. By purchasing a Medigap policy, individuals can gain more comprehensive healthcare coverage and protect themselves from unexpected medical costs. Medigap plans offer flexibility, allowing individuals to choose their own doctors and hospitals that accept Medicare, ensuring they receive the care they need without being restricted to a specific network.

The Trust Factor: Examining the Reliability of AAA Insurance Adjusters

You may want to see also

Explore related products

![]()

Medigap policies are sold by private insurance companies

Medigap, also known as Medicare Supplement Insurance, is a type of health insurance sold by private insurance companies. It is designed to fill the gaps in the original Medicare Plan coverage by helping to pay for healthcare costs that the original plan does not cover. These costs can include deductibles, copays, and coinsurance. Medigap policies are available in all 50 states and Washington, D.C., and can vary in premiums and enrollment eligibility.

Private insurance companies like Blue Cross and Blue Shield (BCBS), Cigna, and Humana offer Medigap plans. These plans are standardized, meaning that all insurance companies must provide the same benefits. However, the costs of these plans can vary, and not all standardized plans may be available in every area. Medigap policies must follow federal and state laws, and the front of the policy must clearly identify it as "Medicare Supplement Insurance".

Individuals who are 65 years or older and enrolled in Medicare Parts A and B are typically eligible for Medigap plans. In some states, individuals under 65 who are eligible for Medicare due to disability or End-Stage Renal Disease may also be eligible for Medigap. It's important to note that Medigap policies are sold separately from Medicare Advantage and Prescription Drug Plans.

When purchasing a Medigap policy, individuals must continue to pay their Part B premium and a separate premium for Medigap coverage. These policies are guaranteed renewable as long as the premium is paid, and they renew automatically each year. Medigap coverage generally has no network limitations and is available anywhere that Medicare is accepted. Some Medigap plans also cover foreign travel emergency services.

Overall, Medigap policies provided by private insurance companies offer valuable supplemental coverage to individuals with original Medicare plans, helping to reduce out-of-pocket costs and providing additional benefits.

Life Insurance and Taxes: What's the Verdict?

You may want to see also

Explore related products

![]()

Medigap policies are standardized, meaning they must provide the same benefits

Medigap, or Medicare Supplement Insurance, is an extra insurance policy that can be purchased from a private health insurance company to help pay for out-of-pocket costs in Original Medicare. Medigap policies are designed to fill in the "gaps" in Original Medicare Plan coverage, meaning they help pay for some healthcare costs that the Original Medicare Plan does not cover.

Medigap policies have been standardized across the United States since July 31, 1992, as a result of the Omnibus Budget Reconciliation Act of 1990. This means that all Medigap policies must provide the same benefits, regardless of the insurance company selling them. The standardization of Medigap policies makes it easier for consumers to compare benefits and premiums across different plans and insurance companies. It is important to note that Medigap policies are subject to both Federal and state laws, and while the benefits must remain the same, costs can vary.

The standardized Medigap benefit policies are labelled by letter, with Policy A containing the basic or "core" benefits. All other policies include the core benefits, with one or more additional benefits. For example, policies beyond A offer additional benefits such as Part A Skilled Nursing Facility Coinsurance for Days 21-100 and Preventive Medical Care. It is worth noting that some states have instituted consumer protections for Medigap that go beyond the minimum federal standards, and these may vary from state to state.

When purchasing a Medigap policy, individuals must already have Medicare Part A and Part B, and they must pay the monthly Medicare Part B premium, as well as a premium to the Medigap insurance company. Additionally, individuals can only have one Medigap policy at a time, and it will only cover the individual; spouses must purchase separate policies.

Profiting from Insurance Affiliate Marketing: A Beginner's Guide

You may want to see also

Explore related products

![]()

Medigap policies are guaranteed renewable as long as premiums are paid

Medigap, also known as Medicare Supplement Insurance, is health insurance sold by private insurance companies to fill the "gaps" in Original Medicare Plan coverage. It helps pay some of the out-of-pocket health care costs that the Original Medicare Plan doesn't cover. For example, it can help cover your Part A and B (Original Medicare) costs such as deductibles and coinsurance. Generally, you must have Original Medicare – Part A and Part B – to buy a Medigap policy.

It's important to note that Medigap policies must follow Federal and state laws, and insurance companies can only sell standardized Medigap policies. These policies must provide the same benefits, and the only difference between policies sold by different insurance companies is usually the cost. You and your spouse must buy separate Medigap policies, and your policy won't cover any health care costs for your spouse.

In some states, insurance companies may refuse to renew a Medigap policy bought before 1992. Additionally, those who were eligible for Medigap before January 1, 2020, but did not enroll, may still be able to buy certain plans that are no longer available to those who became eligible after that date.

FloridaBlue: Commercial or Private Insurance?

You may want to see also

Explore related products

![]()

Medigap plans cover foreign travel emergency services

Medigap, also known as Medicare Supplement Insurance, is health insurance sold by private insurance companies to fill the "gaps" in Original Medicare Plan coverage. Medigap policies help pay some of the healthcare costs that the Original Medicare Plan (Part A and Part B) does not cover. Generally, you must have Original Medicare Plan coverage to buy a Medigap policy.

Some Medigap plans offer foreign travel emergency healthcare coverage, providing peace of mind for international travellers. Medigap plans C, D, F, G, M, and N provide foreign travel emergency health coverage. However, it's important to understand the limitations of this coverage. There is a $50,000 lifetime limit on all Medigap travel plans, and coverage is limited to the first 60 days of travel outside the country. Medigap will cover 80% of the charges for "medically necessary emergency care" and may pay for ambulance rides or emergency transportation to a foreign hospital. Medigap does not cover routine care, such as regular check-ups or non-emergency treatments, and it will not pay for drugs outside of the US.

When choosing a Medigap plan for foreign travel emergency services, it is essential to carefully review the plan details to understand what is covered and what is not. Additionally, consider purchasing additional travel insurance to cover medical emergencies beyond the Medigap limits and for non-covered scenarios.

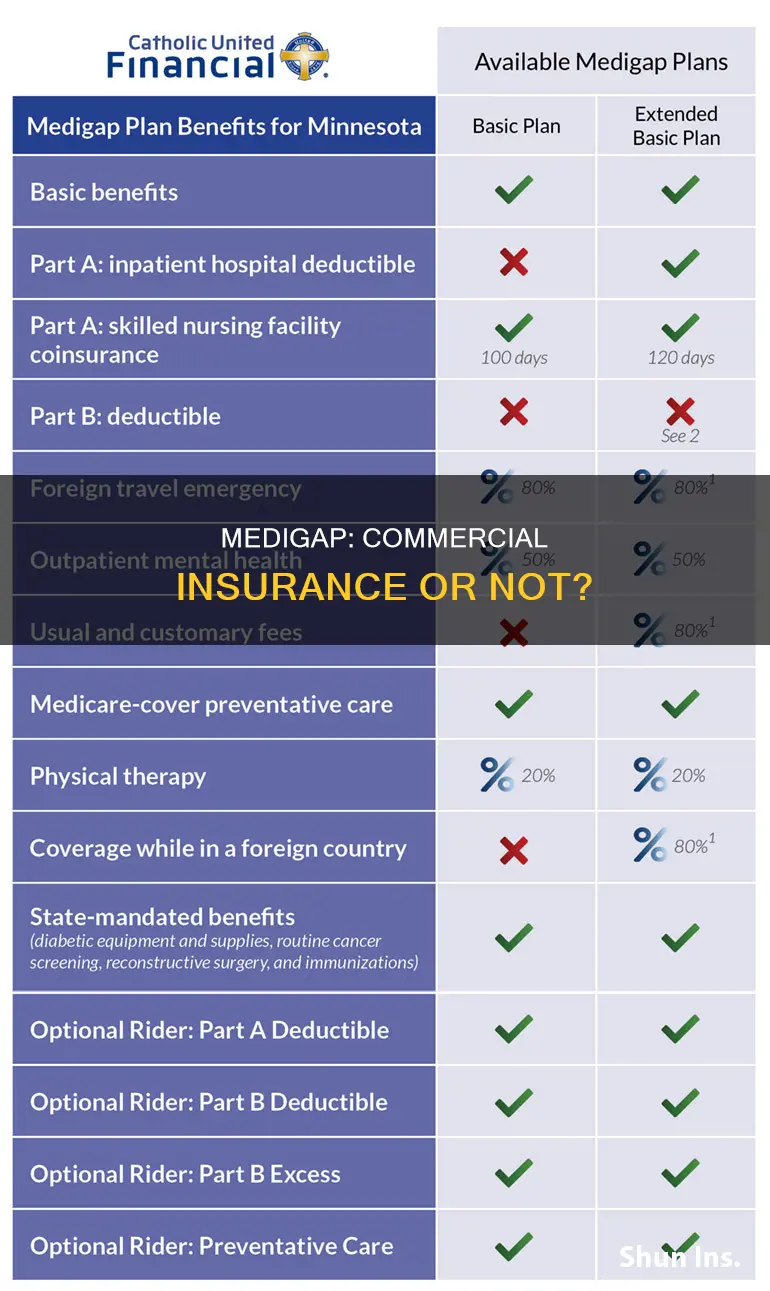

Medigap policies E, H, I, and J previously offered foreign-travel emergency healthcare coverage but are no longer available for new buyers. However, those who already have these policies can keep them. It is worth noting that Medigap plans in certain states, such as Massachusetts, Minnesota, and Wisconsin, may differ from those available in other states. For example, in Minnesota, the Basic and Extended Basic plans pay 80% of foreign-travel emergency costs.

In summary, Medigap plans can provide valuable coverage for foreign travel emergencies, but travellers should be aware of the limitations and consider supplementing with additional travel insurance to ensure comprehensive protection during their international journeys.

Unraveling the Art of Roof Damage Assessment: A Guide to Insurance Adjusters' Methods

You may want to see also

Frequently asked questions

Medigap is extra insurance that can be purchased from a private health insurance company to help pay for out-of-pocket costs not covered by Original Medicare (Parts A and B).

Yes, Medigap is a type of commercial insurance sold by private insurance companies.

Medigap covers some of the healthcare costs that Original Medicare doesn't, such as coinsurance, copayments, deductibles, and foreign travel emergency services.

Generally, you must have Original Medicare (Part A and Part B) to buy a Medigap policy. Some states also offer Medigap to those under 65 who are eligible for Medicare due to disability or End-Stage Renal Disease.

Medigap plans are sold by private insurance companies like Blue Cross Blue Shield, Cigna, and Humana. You can compare plans and prices from different providers and choose the one that best suits your needs.