Life insurance is a contract between an insurance company and a policy owner, in which the insurer guarantees to pay a sum of money to the policy's beneficiaries when the insured person dies. The purpose of life insurance is to provide financial security for the policyholder's loved ones after their death. It can be used to cover living expenses, pay off debts, fund children's education, and more. There are two main types of life insurance: term life insurance, which runs for a fixed period, and whole life insurance, which pays out regardless of when the policyholder dies, provided they have kept up with premium payments. Life insurance is particularly important for those with dependents, such as parents with minor children, who would suffer financial hardship in the event of the policyholder's death.

| Characteristics | Values |

|---|---|

| Purpose | Provide financial security for loved ones, income replacement, debt payoff, college education for children, funeral costs, retirement income supplement |

| Policy Types | Term life insurance, permanent life insurance (whole life insurance, universal life insurance), burial insurance, survivorship life insurance |

| Beneficiaries | Spouse, children, other family members, business |

| Cost Factors | Age, sex, health, lifestyle, driving history, occupation |

| Payout Options | Lump sum, retained asset account, life income, life income with period certain, specific income |

Explore related products

What You'll Learn

![]()

Peace of mind for you and your loved ones

Life insurance provides peace of mind for you and your loved ones by offering financial protection in the event of your death. It ensures that your loved ones will have the financial resources they need to maintain their standard of living and cover essential expenses. Here are some key reasons why life insurance is important for peace of mind:

Income Replacement

Life insurance provides income replacement for your loved ones, especially if you are the primary breadwinner. It helps your dependents, such as your spouse or children, maintain their standard of living by covering daily living expenses, childcare, healthcare, and other essential costs. This financial cushion allows them to grieve and adjust to their new situation without immediate financial worries.

Debt and Expense Coverage

Life insurance can help pay off any outstanding debts, such as mortgages, credit card bills, medical bills, or car loans. It ensures that your loved ones are not burdened with these financial obligations and can maintain their financial stability during a difficult time.

Funeral and Final Expenses

Funeral and final expenses can be significant, and life insurance provides funds to cover these costs. This ensures that your loved ones don't have to worry about finances during their time of grief and can honour your passing with dignity.

Education Funding

Life insurance can be used to fund your children's education, ensuring they have the resources they need to pursue their academic goals without taking on excessive student debt.

Retirement Support

Life insurance can supplement retirement savings, providing additional financial security for your spouse or dependent children during their golden years.

Tax-Free Benefits

In most cases, the death benefit from a life insurance policy is tax-free, allowing your beneficiaries to receive the full amount without tax liabilities. This maximizes the value of the benefit and ensures your loved ones receive the full intended financial support.

Life insurance is a valuable tool for protecting your loved ones financially and providing peace of mind for yourself and your family. It ensures that your dependents will have the resources they need to maintain their standard of living, cover essential expenses, and pursue their goals even after your passing.

Term Life Insurance: Early Cash-Out Options?

You may want to see also

Explore related products

![]()

Financial security for your family

Life insurance is a contract between an insurance company and a policy owner. The policyholder pays premiums to the insurer during their lifetime, and in exchange, the insurer guarantees to pay a sum of money to the policy's beneficiaries when the insured person dies. This payout is known as a death benefit and can be used to cover the deceased's living expenses, pay off any outstanding debts, and provide financial security for their family.

Life insurance is especially important if you have a family or dependents who rely on your income. The death benefit from a life insurance policy can help your loved ones maintain their standard of living, even after you're gone. It can be used to cover everyday living expenses, such as childcare, healthcare, or education costs. It can also help eliminate household debt and preserve a family business.

The death benefit from a life insurance policy is generally not subject to federal income taxes, so your beneficiaries will receive the full amount. This tax-free benefit ensures that your family can make the most of the money and maintain their financial stability.

In addition to the death benefit, some life insurance policies, such as whole life insurance, also offer a cash value component. This means that the policy builds cash value over time, which can be accessed by the policyholder during their lifetime. This cash value can be used to supplement retirement income, fund a child's education, or establish an emergency fund.

When choosing a life insurance policy, it's important to consider your family's financial needs and goals. A financial professional can help you calculate the amount of coverage you need and present potential options that suit your specific circumstances.

By purchasing life insurance, you can have peace of mind knowing that your family will be financially secure, even in your absence. It ensures that your loved ones will have the resources they need to maintain their quality of life and achieve their financial goals.

Utah Life Insurance: Annuities and Their Coverage

You may want to see also

Explore related products

![Property and Casualty Insurance License Exam Study Guide: Property Casualty Insurance Book and Practice Test Questions [3rd Edition]](https://m.media-amazon.com/images/I/71MhA+5nDML._AC_UY218_.jpg)

![]()

Help with paying off debts and living expenses

Life insurance is a contract between an insurance company and a policy owner. The insurer guarantees to pay a sum of money to one or more named beneficiaries when the insured person dies. In exchange, the policyholder pays premiums to the insurer during their lifetime.

The primary purpose of life insurance is to replace your income after you die. The payout can help your loved ones maintain their lifestyle and cover essential living expenses. It can also be used to pay off any outstanding debts, such as credit card debt, personal loans, or mortgages.

- Debt Coverage: Life insurance can be used to pay off various types of debt, including credit card debt, personal loans, or mortgages. It ensures that your loved ones are not burdened with these financial obligations in the event of your death.

- Income Replacement: Life insurance provides a lump-sum payout that can replace your income, enabling your dependents to maintain their standard of living. This is especially important if you are the primary breadwinner in your family.

- Living Expenses: The payout from life insurance can help cover essential living expenses for your beneficiaries, such as rent or mortgage payments, utility bills, and daily living costs. It provides financial security during a difficult time.

- Education Costs: Life insurance can assist in funding your children's education. It ensures that they have the financial resources to pursue their educational goals, even in your absence.

- Final Expenses: Life insurance can cover funeral expenses and other end-of-life costs, ensuring that your loved ones do not bear this financial burden.

- Supplemental Income: In some cases, life insurance policies may offer additional benefits, such as disability income riders, which provide a monthly income if the policyholder becomes unable to work due to an illness or injury.

- Loan Repayment: If you have co-signed loans or shared debts with someone else, life insurance can help them repay those obligations. It protects your loved ones from shouldering the entire debt burden.

- Estate Planning: Life insurance can be used as a tool for estate planning, ensuring that your heirs receive the full value of your estate. It can also provide funds to cover estate taxes, if applicable.

- Peace of Mind: Life insurance offers peace of mind, knowing that your loved ones will be financially secure in the event of your untimely death. It alleviates the stress and anxiety associated with financial uncertainty.

It is important to carefully consider your financial situation, including any debts and living expenses that your loved ones may need to address in your absence. Consulting with a financial advisor or insurance expert can help you determine the appropriate level of coverage to meet these needs.

Having Two Life Insurance Policies: Wise or Wasteful?

You may want to see also

Explore related products

![]()

Tax-free benefits for your beneficiaries

Life insurance is a contract between an insurance company and a policy owner, where the insurer guarantees to pay a sum of money to one or more named beneficiaries when the insured person dies. The policyholder must pay a single premium upfront or regular premiums over time for the life insurance policy to remain in force.

The death benefit of a life insurance policy is usually tax-free. However, if the death benefit is paid out in instalments and the remaining portion earns interest, that interest is taxable. The death benefit might also be taxable if paid to the insured's estate instead of an individual or entity.

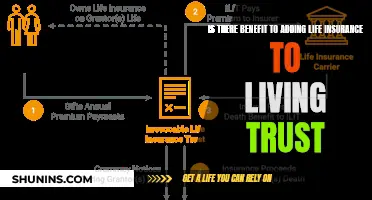

- Transfer policy ownership: Note that value beyond what was paid for the policy will be regarded as taxable. If you transfer the policy within three years of your death, the IRS will treat it as though it still belongs to you.

- Create an irrevocable life insurance trust (ILIT): Transfer ownership of the policy from yourself to an ILIT to remove it from your estate. However, be aware that this kind of trust cannot be revoked after you set it up.

- Be aware of gift tax limits: In 2024, the annual gift tax exemption is $18,000, and the lifetime exclusion amount is $13.61 million. If you're careful that your policy's cash value does not exceed these limits, you may be able to avoid taxation.

It is important to review your policy and ensure that your beneficiary designations are up-to-date to avoid any tax complications.

Changing Life Insurance Beneficiaries During Divorce

You may want to see also

Explore related products

$8

$9.67 $12.99

![]()

Protection for your business

Life insurance is an important consideration for business owners, as it can help protect their company and loved ones financially. Here are some ways life insurance can be used as protection for your business:

Keep Your Business Running

Life insurance can help keep your company afloat by paying off business debts, supplementing cash flow, and covering expenses needed to find your replacement if you pass away. The death benefit can be used to support your family or keep the business running as you wish.

Fund Partnership Agreements

If you have business partners, a partnership agreement is typically in place. This agreement stipulates that if one partner dies or becomes incapacitated, the surviving partners have the right to buy out their share of the business. Life insurance can provide the necessary funds for this buyout, ensuring the business can continue as planned.

Equalize an Estate

Life insurance can be used to ensure that all heirs receive an equal inheritance, even if one child works in the family business while another does not. The insurance payout can allow the child in the business to inherit the corporation's shares, while the other child receives an insurance payout, resulting in an equal distribution.

Protect Your Family

Life insurance can replace your income and provide financial security for your family if you pass away unexpectedly. It can help cover expenses, such as your children's education, your spouse's retirement, and any business or personal debts, ensuring your family can maintain their standard of living.

Key Person Life Insurance

Key person life insurance, also known as key man or key woman insurance, is designed to protect your business if you lose a vital owner, executive, or employee. It can help cover business loans or losses, buy back the deceased's shares, cover the cost of replacing the employee, and even provide severance to staff if the business needs to close.

Buy-Sell Agreements

A buy-sell agreement is a legally binding contract between business owners that outlines what will happen to the business if one owner dies, becomes disabled, or wants to sell their interest. Life insurance is often used to fund these agreements, ensuring the surviving owners have the financial means to buy out the deceased owner's share and maintain business continuity.

Individual Life Insurance for Small Business Owners

As a small business owner, individual life insurance can provide financial protection for your loved ones and your business. In the event of your death, it can help pay the bills, fund a new key employee's salary, and ensure your business can keep its doors open.

Beneficiary Basics: Understanding Life Insurance Beneficiary Rights

You may want to see also

Frequently asked questions

Life insurance is a contract between an insurance company and a policy owner in which the insurer guarantees to pay a sum of money to one or more named beneficiaries when the insured person dies. In exchange, the policyholder pays premiums to the insurer during their lifetime.

Life insurance provides financial security for your loved ones after you're gone. It can help pay off debts, living expenses, medical or final expenses, and can also be used to provide income replacement for your family.

There are two primary types of life insurance: term life insurance and permanent life insurance. Term life insurance provides protection for a certain period and is usually the cheapest option. Permanent life insurance provides lifetime coverage and is more expensive, but it can also include a cash value component that accumulates on a tax-deferred basis.