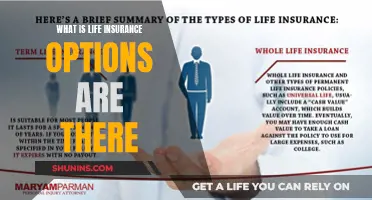

Term life insurance is a type of life insurance that has no cash value. This means that it does not have a savings-like component that can build over time. Instead, term life insurance provides a death benefit to the policyholder's beneficiaries. Whole life, variable life, and universal life insurance, on the other hand, are examples of cash value life insurance.

Explore related products

$15.95

$0.99

What You'll Learn

![]()

Term life insurance has no cash value

Term life insurance is different from whole life, variable life, and universal life insurance, which are all examples of cash value life insurance. With cash value life insurance, the policyholder can access funds during their lifetime to fund retirement, cover premiums, increase a death benefit, or for other purposes.

Withdrawals from the cash value of a policy are tax-free, but any cash value growth beyond what was paid in premiums is taxed as income. In most cases, beneficiaries will not receive any cash value after the policyholder's death. The money accumulated in the cash value becomes the property of the insurer.

Term life insurance, on the other hand, does not have this savings-like component. It provides only life insurance coverage, without the additional benefit of a cash value that can be accessed during the policyholder's lifetime.

Life Insurance: AmFam's Comprehensive Coverage for Peace of Mind

You may want to see also

Explore related products

![]()

Whole life insurance is a type of cash value life insurance

Term life insurance is a type of life insurance that has no cash value. Cash value life insurance, on the other hand, provides both life insurance and a savings-like component that can build over time. This cash value component typically earns interest or other investment gains and grows tax-deferred.

In most circumstances, your beneficiaries will not receive any cash value after you die. The cash value component serves as a living benefit for policyholders from which they may access funds.

Understanding Ledger Selling in Life Insurance

You may want to see also

Explore related products

![]()

Universal life insurance is also a type of cash value life insurance

Term life insurance is the type of life insurance that has no cash value. Cash value life insurance is a policy that provides both life insurance and a savings-like component that can build over time. This cash value component typically earns interest or other investment gains and grows tax-deferred.

Whole life and variable life insurance are also examples of cash value life insurance.

Joint Life Insurance: How Long Does It Last?

You may want to see also

Explore related products

![]()

Term life insurance is a permanent type of insurance

Term life insurance is a type of insurance that does not have a cash value. This means that it does not have a savings-like component that can build over time. Instead, term life insurance provides a death benefit to the policyholder's beneficiaries.

In contrast, term life insurance provides coverage for a specified term or period. It is designed to provide financial protection for a limited duration, such as during the policyholder's working years or until their dependents become financially independent. While term life insurance does not have a cash value, it can still be a valuable form of protection for individuals and families.

One of the key advantages of term life insurance is its affordability. Compared to permanent life insurance, term life insurance typically offers lower premiums for a higher level of coverage. This makes it a cost-effective option for individuals seeking financial security for their loved ones in the event of their death. Additionally, term life insurance can be tailored to meet specific needs and budgets, with various term lengths and coverage amounts available.

Overall, while term life insurance does not have a cash value component, it is a permanent type of insurance that offers long-term financial protection. It provides peace of mind and security by ensuring that the policyholder's beneficiaries receive a death benefit during the specified term. By understanding the features and benefits of term life insurance, individuals can make informed decisions about their financial planning and ensure their loved ones are taken care of.

Get Licensed: Health and Life Insurance Basics

You may want to see also

Explore related products

![Short Term 12 [Blu-ray]](https://m.media-amazon.com/images/I/71Lb114AFoL._AC_UY218_.jpg)

![]()

Cash value life insurance can be used to fund retirement

Term life insurance does not have a cash value. However, permanent life insurance policies, such as whole life, variable life, and universal life insurance, do have a cash value component that can be used to fund retirement.

Cash value life insurance is a policy that provides both life insurance and a savings-like component that can build over time. This cash value component typically earns interest or other investment gains and grows tax-deferred. The cash value can be accessed during your lifetime to fund retirement, cover premiums, increase a death benefit, or for other purposes. Withdrawals from the cash value of a policy are tax-free, but any cash value growth beyond what you paid in premiums is taxed as income.

For example, consider a policy with a $25,000 death benefit. The policy has no outstanding loans or prior cash withdrawals and an accumulated cash value of $5,000. Upon the death of the policyholder, the insurance company pays the full death benefit of $25,000. The money accumulated in the cash value becomes the property of the insurer, reducing the real liability cost to the life insurance company. In this case, the real liability cost would be $20,000 ($25,000 - $5,000).

It is important to note that in most circumstances, your beneficiaries will not receive any cash value after you die. Therefore, if you are considering using cash value life insurance to fund your retirement, it is essential to understand how the policy works and what options are available to you.

While cash value life insurance can provide a source of funding for retirement, it may not be the best option for everyone. It is important to carefully consider your financial goals, risk tolerance, and other factors before deciding if cash value life insurance is the right choice for you. Consulting with a financial advisor or insurance professional can help you make an informed decision.

Using Life Insurance Money: When and How to Access Funds

You may want to see also

Frequently asked questions

Term life insurance.

Cash value life insurance is a policy that provides both life insurance and a savings-like component that can build over time.

Whole life, variable life, and universal life insurance are all examples of cash value life insurance.

The cash value component serves as a living benefit for policyholders from which they may access funds during their lifetime to fund retirement, cover premiums, increase a death benefit or for other purposes.

![Short Term 12 [DVD] [2013] [Region 1] [US Import] [NTSC]](https://m.media-amazon.com/images/I/51jC+xMaCBL._AC_UY218_.jpg)

![End of Term [DVD]](https://m.media-amazon.com/images/I/61zb8XLHPXL._AC_UY218_.jpg)

![End of Term [Blu-ray]](https://m.media-amazon.com/images/I/61C-da10mXL._AC_UY218_.jpg)