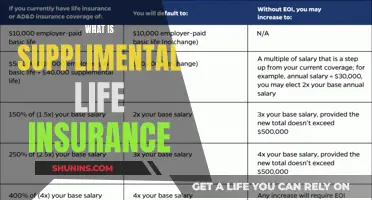

Group term life insurance is tax-free for the employee up to a certain amount. If employer-provided coverage is greater than $50,000, the excess amount is considered a non-cash fringe benefit, and the premiums for that extra coverage become taxable income for the employee. There can also be tax implications if employer-provided group term life insurance is offered for an employee's spouse or dependents. If the amount of coverage is $2,000 or less, then it's not taxable to the employee.

| Characteristics | Values |

|---|---|

| Taxable amount | Greater than $50,000 |

| Taxable amount for employee's spouse or dependents | Greater than $2,000 |

| Taxable amount for employee's spouse or dependents if less than $2,000 | Not taxable |

| Taxable amount for employee's spouse or dependents if greater than $2,000 | Taxable |

Explore related products

What You'll Learn

- Group term life insurance is tax-free for the employee up to $50,000

- If employer-provided coverage is greater than $50,000, the excess amount is considered a non-cash fringe benefit, and the premiums for that extra coverage become taxable income for the employee

- If the amount of coverage is $2,000 or less, then it's not taxable to the employee

- The premiums on coverage for spouses or dependents over $2,000 could be treated as taxable income for the employee

- The determination of whether the premium charges straddle the costs is based on the IRS Premium Table rates, not the actual cost

![]()

Group term life insurance is tax-free for the employee up to $50,000

If employer-provided coverage is greater than $50,000, the excess amount is considered a non-cash fringe benefit, and the premiums for that extra coverage become taxable income for the employee. This means that if you have a family or other financial dependents, the non-taxable amount of $50,000 in life insurance may not be adequate.

There can also be tax implications if employer-provided group term life insurance is offered for an employee's spouse or dependents. If the amount of coverage is $2,000 or less, then it's not taxable to the employee. However, the premiums on coverage for spouses or dependents over that amount could be treated as taxable income for the employee.

At the end of the year, your employer will report the total cost of any group insurance you received that was in excess of $50,000 on your W-2 form.

Life Insurance: A Necessary Protection or Guilt Trip?

You may want to see also

Explore related products

$9.99 $14.95

![]()

If employer-provided coverage is greater than $50,000, the excess amount is considered a non-cash fringe benefit, and the premiums for that extra coverage become taxable income for the employee

Group term life insurance is tax-free for the employee up to a certain amount. If employer-provided coverage is greater than $50,000, the excess amount is considered a non-cash fringe benefit, and the premiums for that extra coverage become taxable income for the employee. This is because the employer is affecting the premium cost through its subsidising and/or redistributing role, and so there is a benefit to employees. This benefit is taxable even if the employees are paying the full cost they are charged.

The amount shown on your paycheck or pay stub for group term life insurance represents the taxable benefit. When you receive a W-2 form from your employer at the end of the year, it will report the total cost of any group insurance you received that was in excess of $50,000. This means that if you have employer-provided coverage of $51,000, the extra $1,000 will be taxed.

There can also be tax implications if employer-provided group term life insurance is offered for an employee's spouse or dependents. If the amount of coverage is $2,000 or less, then it's not taxable to the employee. The premiums on coverage for spouses or dependents over that amount, however, could be treated as taxable income for the employee.

Life Insurance in the 21st Century: What's Changed?

You may want to see also

Explore related products

![]()

If the amount of coverage is $2,000 or less, then it's not taxable to the employee

Group term life insurance is tax-free for the employee up to a certain amount. If the amount of coverage is $2,000 or less, then it's not taxable to the employee. This is because it is considered a de minimis fringe benefit, which is excluded from tax. The cost of employer-provided group-term life insurance on the life of an employee's spouse or dependent is also not taxable to the employee if the face amount of the coverage does not exceed $2,000. However, if the coverage exceeds $2,000, then the entire amount of the premium is considered taxable.

The non-taxable amount of $50,000 in life insurance may not be adequate if you have a family or other financial dependents. Group term life insurance is taxed after the first $50,000. If employer-provided coverage is greater than $50,000, the excess amount is considered a non-cash fringe benefit, and the premiums for that extra coverage become taxable income for the employee. There can also be tax implications if employer-provided group term life insurance is offered for an employee's spouse or dependents.

Life Insurance Options with Bicuspid Aortic Valve

You may want to see also

Explore related products

![]()

The premiums on coverage for spouses or dependents over $2,000 could be treated as taxable income for the employee

Group term life insurance is tax-free for the employee up to a certain amount. If employer-provided coverage is greater than $50,000, the excess amount is considered a non-cash fringe benefit, and the premiums for that extra coverage become taxable income for the employee. There can also be tax implications if employer-provided group term life insurance is offered for an employee's spouse or dependents. If the amount of coverage is $2,000 or less, then it's not taxable to the employee. However, the premiums on coverage for spouses or dependents over that amount could be treated as taxable income for the employee.

The determination of whether the premium charges straddle the costs is based on the IRS Premium Table rates, not the actual cost. If part of the coverage for a spouse or dependent is taxable, the same Premium Table is used as for the employee. In some cases, an amount greater than $2,000 of coverage could be considered a de minimis benefit. This depends on all the facts and circumstances.

Group term life insurance is a form of term life insurance, usually offered by the employer tax-free for up to $50,000. The non-taxable amount of $50,000 in life insurance may not be adequate if you have a family or other financial dependents. The amount shown on your paycheck or pay stub for group term life insurance represents the taxable benefit. When you receive a W-2 form from your employer at the end of the year, it will report the total cost of any group insurance you received that was in excess of $50,000.

Who Can Get Life Insurance on Your Behalf?

You may want to see also

Explore related products

![]()

The determination of whether the premium charges straddle the costs is based on the IRS Premium Table rates, not the actual cost

Group term life insurance is tax-free for the employee up to a certain amount. If employer-provided coverage is greater than $50,000, the excess amount is considered a non-cash fringe benefit, and the premiums for that extra coverage become taxable income for the employee. Similarly, if the amount of coverage for an employee's spouse or dependents is $2,000 or less, then it's not taxable to the employee. However, the premiums on coverage for spouses or dependents over that amount could be treated as taxable income for the employee.

The IRS Premium Table is also used if part of the coverage for a spouse or dependent is taxable. It is important to note that a policy that is not considered carried directly or indirectly by the employer has no tax consequences to the employee. As such, group term life insurance is referred to as a non-cash earning on an employee's paystub.

While group term life insurance is usually offered by the employer tax-free for up to $50,000, this amount may not be adequate if an employee has a family or other financial dependents. Additionally, it is important to remember that group term life insurance cannot be taken with an employee if they leave their job or are fired.

Foresters Life Insurance: Borrowing Against Your Policy?

You may want to see also

Frequently asked questions

Group term life insurance is a form of term life insurance, usually offered by an employer tax-free for up to $50,000.

If employer-provided coverage is greater than $50,000, the excess amount is considered taxable income for the employee.

If the amount of coverage is $2,000 or less, then it's not taxable to the employee. The premiums on coverage for spouses or dependents over that amount could be treated as taxable income for the employee.

The taxable amount of group term life insurance is based on the IRS Premium Table rates, not the actual cost.