Whole life insurance offers coverage for the life of the policyholder, as long as premiums are paid. Whole life insurance interest rates are fixed, with a minimum guaranteed rate. Whole life insurance compound interest means that your money will grow steadily, but your rate of return may not be as significant as it would be with some other types of investment. Whole life insurance also comes with a savings feature called cash value, which you can borrow from while you're still alive. The average cost of whole life insurance is $440 per month. This is the amount a 30-year-old non-smoker in good health will pay for a $500,000 whole life insurance policy. The actual dividend interest rate has declined over the years to the current level of 5%.

| Characteristics | Values |

|---|---|

| Interest rates | Fixed |

| Interest rates | Minimum guaranteed rate |

| Interest rates | 3% to 5% |

| Average cost | $440 per month |

| Average cost for a 30-year-old female smoker in good health | $505.20 per month |

| Average cost for a 30-year-old male smoker in good health | $602.40 per month |

Explore related products

![The Telomere Effect, Lifespan [Hardcover], Hidden Healing Powers Of Super & Whole Foods, The Healthy Medic Food for Life Meals in 15 minutes 4 Books Collection Set](https://m.media-amazon.com/images/I/715Hy8lI8hL._AC_UY218_.jpg)

What You'll Learn

![]()

Whole life insurance interest rates are fixed

The average cost of whole life insurance is $440 per month. That’s the amount a 30-year-old who doesn’t smoke and is generally in good health will pay for a $500,000 whole life insurance policy. A 30-year-old female smoker who’s in otherwise good health can expect to pay $505.20 per month for the same coverage. A 30-year-old male smoker with a similar health profile can expect to pay $602.40 per month.

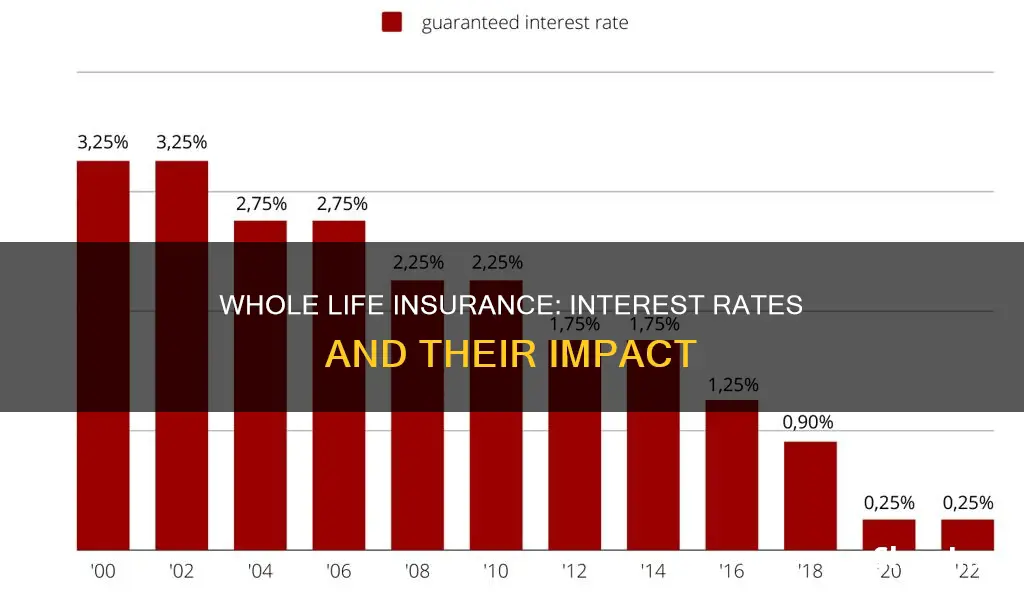

Whole life insurance policies contain minimum cash value interest rate guarantees. The older blocks of business have guarantees that range from 3% to 5%. The actual dividend interest rate has declined over the years to the current level of 5%, a reduction of 500 basis points from the original earnings assumptions.

How Much Coverage? Understanding 6 Units of Life Insurance

You may want to see also

Explore related products

![]()

Whole life insurance features a cash value

Whole life insurance policies contain minimum cash value interest rate guarantees. The dividend interest rate has declined over the years to the current level of 5%, which is a reduction of 500 basis points from the original earnings assumptions. This means that earnings today are 50% of the assumed rate that was depicted in the original sales illustration.

Whole life insurance offers coverage for the life of the policyholder, as long as premiums are paid. When the policyholder dies, a death benefit is paid out to a beneficiary or beneficiaries. There are several forms that whole life insurance can take, with each one catering to different financial needs and preferences.

The average cost of whole life insurance is $440 per month. This is the amount a 30-year-old who doesn't smoke and is generally in good health will pay for a $500,000 whole life insurance policy.

Life Insurance: A Necessary Investment for Peace of Mind?

You may want to see also

Explore related products

![]()

Whole life insurance doesn't expire

Whole life insurance offers coverage for the life of the policyholder, as long as premiums are paid, with a death benefit paid out to a beneficiary or beneficiaries when the policyholder dies. Whole life features a cash value, which is held in an account that accumulates over time. This cash value can be borrowed from while the policyholder is still alive.

Universal and whole life policies contain minimum cash value interest rate guarantees, with older blocks of business guaranteed to range from 3% to 5%. The actual dividend interest rate has declined over the years to the current level of 5%, a reduction of 500 basis points from the original earnings assumptions.

The average cost of whole life insurance is $440 per month for a 30-year-old non-smoker in good health. A 30-year-old female smoker in good health can expect to pay $505.20 per month for a whole life insurance policy with a $500,000 payout. A 30-year-old male smoker with a similar health profile can expect to pay $602.40 per month for the same coverage.

Changing Life Insurance Tax Laws: Who Benefits?

You may want to see also

Explore related products

![]()

Whole life insurance compound interest

Whole life insurance is a type of permanent life insurance that offers coverage for the entire life of the policyholder, provided that the premiums are paid. When the policyholder dies, a death benefit is paid out to their chosen beneficiary or beneficiaries. Whole life insurance also features a cash value, which is held in an account that accumulates over time. This cash value is guaranteed to grow at a minimum interest rate, which is often fixed.

The guaranteed minimum interest rate for whole life insurance policies can vary, but it is typically between 3% and 5%. This rate is often lower than the interest rates offered by other types of investments, such as stocks or mutual funds. However, it is important to note that whole life insurance provides a guaranteed rate of return, which means that policyholders can be confident that their money will grow at a steady rate, even if it may not be as significant as other investment options.

Whole life insurance policies are designed to cater to different financial needs and preferences. For example, some policies may offer a higher interest rate in exchange for a higher premium, while others may have a lower interest rate but provide additional benefits, such as disability income protection or long-term care coverage. It is important for individuals to carefully consider their financial goals and priorities when choosing a whole life insurance policy to ensure that they select the option that best meets their needs.

Overall, whole life insurance compound interest provides policyholders with a steady and guaranteed growth of their cash value over time. While the rate of return may not be as high as other investment options, whole life insurance offers the security and peace of mind of knowing that the policyholder's loved ones will be provided for in the event of their death, along with the added benefit of a savings component that can be borrowed against during their lifetime.

Mortgage and Life Insurance: Which is the Better Option?

You may want to see also

Explore related products

![]()

Whole life insurance rates vary based on age, gender, and health

Whole life insurance offers coverage for the life of the policyholder, provided that premiums are paid. It features a cash value that accumulates over time and can be borrowed from while the policyholder is still alive. Whole life insurance interest rates are fixed, with a minimum guaranteed rate. The minimum cash value interest rate guarantee for whole life policies is typically between 3% and 5%.

Who Gets the Payout? Ex-Wife's Rights to Life Insurance

You may want to see also

Frequently asked questions

Whole life insurance interest rates are fixed, with a minimum guaranteed rate. The minimum cash value interest rate guarantees range from 3% to 5%.

The minimum interest rate for whole life insurance is 3%.

The maximum interest rate for whole life insurance is 5%.