Term insurance and life insurance are two types of financial plans that people take out to ensure they have a peaceful life. The key difference between the two is that term insurance offers coverage for a particular period, whereas life insurance provides coverage over your lifetime. Term insurance is generally more affordable than life insurance, but it does not offer any maturity benefits. Life insurance, on the other hand, provides both death and maturity benefits.

| Characteristics | Term Insurance | Life Insurance |

|---|---|---|

| Coverage | Particular period | Lifetime |

| Price | Affordable | More expensive |

| Benefits | Death and tax-saving | Death, maturity, survival and tax-saving |

| Maturity | No maturity benefits | Maturity benefits |

Explore related products

What You'll Learn

![]()

Term insurance is more affordable than life insurance

Term insurance is also more customisable than life insurance. Term policies can be tailored to your needs, whereas life insurance policies are more rigid. Term insurance does not have any surrender value or paid-up value, which gives it less flexibility than life insurance. However, term insurance can still be a good option for those who want to create a financial safety net for their family in the event of their death.

Another key difference between term and life insurance is that the former offers coverage for a particular period (the term) while the latter provides coverage over your lifetime. This means that term insurance may be a more cost-effective option for those who only need coverage for a specific period, such as the duration of a mortgage or until children become financially independent.

Term insurance typically only offers death benefits, whereas life insurance provides both death and maturity benefits. This means that with term insurance, your family will receive a payout if you die within the term period, but there are generally no additional benefits if you outlive the policy term. However, there are a few types of term insurance plans, like term return of premium plans and 100% refund of premium plans, that return the premiums paid at the end of the policy term.

Cancer and Cobra: Understanding Retroactive Insurance Coverage

You may want to see also

Explore related products

![]()

Term insurance only offers death benefits

Term insurance is often more affordable than life insurance, which means that there will be less of a financial burden on your family should you pass away while the policy is in force. Term insurance policies are also customisable to your needs, and can be tailored to help your family.

There are a few types of term insurance plans that return the premiums paid at the end of the policy term, such as term return of premium plans and 100% refund of premium plans. However, most term insurance plans do not have any surrender value or paid-up value, and do not offer any maturity benefits.

BDO Life Insurance: Checking Your Policy Status

You may want to see also

Explore related products

![]()

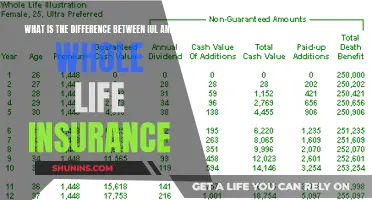

Life insurance offers maturity benefits

Term insurance and life insurance are both types of financial plans that citizens can take out to ensure a more secure life. However, there are some key differences between the two. Term insurance is associated with a more affordable price tag than life insurance, and it only offers coverage for a particular period, whereas life insurance provides coverage over your lifetime. Term insurance also does not offer any maturity benefits, whereas life insurance does.

Maturity benefits are a key advantage of life insurance over term insurance. These benefits are paid out to the policyholder if they outlive the policy term. This means that, in addition to providing financial security in the event of the policyholder's death, life insurance can also provide a source of income during retirement or other life stages.

There are a variety of life insurance plans available that offer different types of maturity benefits. For example, some plans may offer a lump-sum payment upon maturity, while others may provide regular income payments over a specified period. Additionally, some plans may offer the option to surrender the policy before maturity and receive a portion of the benefits.

When considering life insurance, it is important to carefully review the maturity benefits offered by different providers and choose a plan that best fits your needs and financial goals. By doing so, you can ensure that you have the necessary coverage and security for yourself and your loved ones.

Insurability Evidence: Life Insurance's Critical Requirement Explained

You may want to see also

Explore related products

![]()

Life insurance offers more flexibility

Term insurance is generally more affordable than life insurance, but it does not offer the same level of flexibility. Term insurance plans are highly customisable and can be tailored to your needs, but they do not offer the same level of financial security as life insurance plans.

Life insurance plans help you create wealth, protect your family for the entire policy term, and save on your yearly taxes. Most life insurance policies offer maturity benefits if you outlive the policy term. Life insurance also provides death, maturity, survival, and tax-saving benefits.

Term insurance plans, on the other hand, only offer death and tax-saving benefits. While there are a few types of term insurance plans that offer maturity benefits, such as term return of premium plans and 100% refund of premium plans, these are not as common as life insurance plans that offer maturity benefits.

Overall, life insurance offers more flexibility than term insurance because it provides coverage over your lifetime, offers a wider range of benefits, and can help you create wealth.

Understanding the Insured Name on Your Life Insurance Policy

You may want to see also

Explore related products

$8

$9.97 $19.99

![]()

Term insurance offers coverage for a particular period

There are a few types of term insurance plans, like term return of premium plans and 100% refund of premium plans, that return the premiums paid at the end of the policy term. However, most term insurance plans do not offer maturity benefits.

Life Insurance and Veteran Benefits: What's the Connection?

You may want to see also

Frequently asked questions

Term insurance is cheaper and covers you for a set period of time, while life insurance usually costs much more but can last your entire life.

Term insurance is a simple, affordable option for temporary coverage. It has an expiration date and doesn't include a cash value feature.

Life insurance provides lifelong protection and builds cash value, but at a higher cost. It can also act like a tax-advantaged retirement savings plan with a guaranteed rate of return.

The best choice depends on your financial goals, budget, and long-term needs. Term insurance is generally sufficient for most people, but you might want to explore life insurance if you have a lifelong dependent or have maxed out your tax-advantaged retirement accounts.