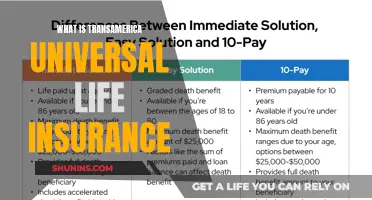

Total and Permanent Disablement Insurance (TPD) is a type of insurance that provides financial support to individuals and their families in the event of an unforeseen disability that prevents them from working. TPD insurance is generally used to cover debts and the ongoing living expenses of an individual to reduce the ongoing financial burden of loss of income.

| Characteristics | Values |

|---|---|

| What is it? | Total and Permanent Disablement Insurance (TPD) |

| What does it cover? | Provides a lump sum benefit to the life insured in the event of a medically diagnosed event that renders the claimant unable to work again |

| What is it used for? | Covering debts and the ongoing living expenses of an individual to reduce the ongoing financial burden of loss of income |

| Types | Own Occupation TPD, Any Occupation TPD, Standalone TPD, TPD as an add-on with personal accident cover |

Explore related products

What You'll Learn

![]()

TPD insurance as an add-on with personal accident cover

Total and Permanent Disability (TPD) insurance is a type of insurance that provides a lump sum benefit to the life insured in the event of a medically diagnosed event that renders the claimant unable to work again. TPD insurance is generally used to cover debts and the ongoing living expenses of an individual to reduce the ongoing financial burden of loss of income.

TPD insurance can be purchased as an add-on with personal accident cover. This type of policy provides coverage for both death and total permanent disability. It is usually less expensive than standalone TPD insurance, but the payout may be lower.

Standalone TPD insurance is a separate insurance policy that provides coverage specifically for total permanent disability. This type of policy typically provides a higher payout than TPD insurance as part of a life insurance policy.

There are three main types and definitions of TPD Insurance:

- Own Occupation TPD - the claimant must be unable to work in their own occupation ever again.

- Any Occupation TPD - the claimant must be unable to work in their occupation and also any occupation that they are suited to via education, training or experience ever again.

It is important to carefully review the product disclosure statement (PDS) and understand the terms and conditions before taking out a TPD insurance policy.

Flat Extra: Life Insurance's Additional Cost Explained

You may want to see also

Explore related products

![]()

Standalone TPD insurance

Total and Permanent Disablement Insurance (TPD) is designed to provide a lump sum benefit to the insured in the event of a medically diagnosed event that renders the claimant unable to work again. TPD insurance is generally used to cover debts and the ongoing living expenses of an individual to reduce the ongoing financial burden of loss of income.

TPD insurance, as an add-on with your personal accident cover, provides coverage for both death and total permanent disability. This type of policy is usually less expensive than standalone TPD insurance, but the payout may be lower. You may choose to buy either Standalone TPD Cover or a disability add-on cover along with your Personal Accident Cover.

There are three main types and definitions of TPD Insurance: Own Occupation TPD – the claimant must be unable to work in their own occupation ever again. Any Occupation TPD – the claimant must be unable to work in their occupation and also any occupation that they are suited to via education, training or experience ever again.

Life Insurance: A Secure Future for Loved Ones

You may want to see also

Explore related products

![]()

Own Occupation TPD

Total and Permanent Disablement Insurance (TPD) is designed to provide a lump sum benefit to the life insured in the event of a medically diagnosed event that renders the claimant unable to work again. TPD insurance is generally used to cover debts and the ongoing living expenses of an individual to reduce the ongoing financial burden of loss of income.

There are three main types and definitions of TPD Insurance: Own Occupation TPD, Any Occupation TPD, and Standalone TPD.

For example, let's say you are a surgeon and you have Own Occupation TPD insurance. If you become permanently disabled and are no longer able to perform surgery, your insurance policy will pay out. Even if you decide to pursue a different career, such as consulting or teaching, you will still receive the benefits of your TPD insurance policy.

Standalone TPD insurance is a separate insurance policy that provides coverage specifically for total permanent disability. This type of policy typically provides a higher payout than TPD insurance as part of a life insurance policy. It offers broad-ranged coverage for permanent illness or accidental injuries.

Life Insurance Payouts After Suicide: What You Need to Know

You may want to see also

Explore related products

![THE TORTURED POETS DEPARTMENT: THE ANTHOLOGY [Explicit]](https://m.media-amazon.com/images/I/61n4O1WTGAL._AC_UY218_.jpg)

![THE TORTURED POETS DEPARTMENT [Explicit]](https://m.media-amazon.com/images/I/519B2Y-lWDL._AC_UY218_.jpg)

![]()

Any Occupation TPD

Total and Permanent Disablement Insurance (TPD) is designed to provide a lump sum benefit to the life insured in the event of a medically diagnosed event that renders the claimant unable to work again. TPD Insurance is generally used to cover debts and the ongoing living expenses of an individual to reduce the ongoing financial burden of loss of income.

There are three main types and definitions of TPD Insurance: Own Occupation TPD and Any Occupation TPD. Any Occupation TPD is when the claimant must be unable to work in their occupation and also any occupation that they are suited to via education, training or experience ever again. This is different from Own Occupation TPD, where the claimant must be unable to work in their own occupation ever again.

Standalone TPD insurance is a separate insurance policy that provides coverage specifically for total permanent disability. This type of policy typically provides a higher payout than TPD insurance as part of a life insurance policy. TPD insurance, as an add-on with your personal accident cover, provides coverage for both death and total permanent disability. This type of policy is usually less expensive than standalone TPD insurance, but the payout may be lower.

Life Insurance and Pregnancy Loss: What Coverage is Offered?

You may want to see also

Explore related products

![]()

How to claim TPD insurance

Total and Permanent Disablement Insurance (TPD) is designed to provide a lump sum benefit to the life insured in the event of a medically diagnosed event that renders the claimant unable to work again. TPD insurance is generally used to cover debts and the ongoing living expenses of an individual to reduce the ongoing financial burden of loss of income.

- Review your policy: Before making a claim, carefully review your TPD insurance policy to understand the terms and conditions, including any exclusions or limitations. Make sure you are familiar with the definition of "total and permanent disability" as outlined in your policy.

- Consult a medical professional: Seek appropriate medical attention and obtain a diagnosis from a qualified healthcare provider. Ensure that your medical records accurately document your condition and its impact on your ability to work.

- Gather evidence: Collect and organise all relevant documentation to support your claim. This may include medical reports, treatment records, employment history, and financial information. The more comprehensive your evidence, the stronger your claim will be.

- Submit your claim: Contact your insurance provider and initiate the claims process. Follow their instructions carefully and provide all the required information and documentation. Be thorough and accurate in your submissions to avoid delays or complications.

- Stay organised: Keep a record of all communications with your insurance provider, including emails, letters, and phone calls. Note the dates, times, and content of these interactions. This will help you track the progress of your claim and address any potential issues that may arise.

- Seek support: If needed, consider seeking assistance from a financial advisor, insurance broker, or legal professional who has experience with TPD insurance claims. They can guide you through the process, ensure your rights are protected, and help you navigate any complexities or disputes that may arise.

Remember, the specific steps and requirements for claiming TPD insurance may vary depending on your insurance provider and the terms of your policy. Always refer to your policy documents and consult with your insurance company for detailed instructions on how to make a claim.

California Teachers' Life Insurance: What's Covered?

You may want to see also

Frequently asked questions

TPD stands for Total and Permanent Disability.

TPD life insurance is a type of insurance that provides financial support to individuals and their families if they become totally and permanently disabled and are unable to work.

TPD life insurance covers the ongoing living expenses of an individual to reduce the financial burden of loss of income.

The amount of money paid out by TPD life insurance varies considerably. Standalone TPD insurance typically provides a higher payout than TPD insurance as part of a life insurance policy.

It is important to carefully review the product disclosure statement (PDS) and understand the terms and conditions before taking out a TPD life insurance policy.