Whole life insurance and universal life insurance are both permanent life insurance policies that offer coverage for the entirety of the insured's lifetime. Whole life insurance policies have level premiums, meaning the amount paid every month remains the same, and feature a cash savings component that the policy owner can draw on or borrow from. Universal life insurance policies, on the other hand, offer flexible premiums that can be adjusted within certain limits and provide policyholders with the ability to accumulate cash value, make withdrawals, and take out policy loans. While whole life insurance guarantees a fixed interest rate on the cash value, universal life insurance interest rates are set by the insurer and can change frequently.

Explore related products

What You'll Learn

- Whole life insurance offers lifelong coverage and a guaranteed death benefit

- Universal life insurance is more flexible, allowing adjustments to premium payments and death benefits

- Whole life insurance has a fixed interest rate on the policy's cash value

- Universal life insurance offers the ability to customise your protection upfront and make adjustments over time

- Whole life insurance is more expensive than universal life insurance

![]()

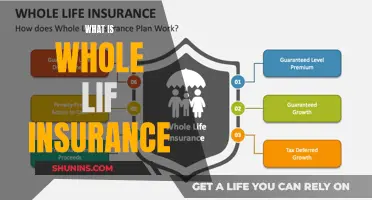

Whole life insurance offers lifelong coverage and a guaranteed death benefit

Whole life insurance is a type of permanent life insurance that offers lifelong coverage. It guarantees a death benefit to the policyholder's beneficiaries when they pass away, as long as the policy is active and premiums are paid. This death benefit amount is established when the policy is signed and remains the same throughout the policy's duration. Whole life insurance policies also offer a savings component called the "cash value", which can be withdrawn or borrowed from during the lifetime of the insured.

Whole life insurance is a permanent insurance policy that provides coverage until the insured's death. It is designed to offer financial confidence and protection for those who want coverage for their entire lives. The policy guarantees a death benefit payout to beneficiaries, along with level rates that won't increase over time. This is in contrast to term life insurance, which only covers a limited period, typically 10, 20, or 30 years, and does not provide a cash value component.

The "cash value" component of whole life insurance is an essential feature. This savings account grows over time and can be accessed by the policyholder for loans, withdrawals, or premium payments. The cash value offers a living benefit, allowing the policyholder to utilise the funds during their lifetime. This cash value grows tax-deferred, and any interest or dividends earned are generally not taxed until withdrawal. Over time, the dividends and interest earned can exceed the total amount of premiums paid.

Whole life insurance policies offer guaranteed coverage, with fixed premium payments that do not change over the life of the policy. This predictability provides stability and assurance to policyholders, knowing that their premiums will remain level. Additionally, the death benefit and cash value growth are guaranteed, ensuring that beneficiaries will receive the promised payout upon the insured's death. This guarantee comes at a cost, as whole life insurance premiums are typically higher than those of term life insurance policies.

Whole life insurance is a comprehensive and stable option for individuals seeking lifelong coverage and guaranteed benefits. It provides peace of mind, knowing that loved ones will be financially protected, and offers the added benefit of a cash value component that can be utilised during the policyholder's lifetime. While it may be more expensive than term life insurance, whole life insurance offers the certainty of fixed premiums, a guaranteed death benefit, and a savings account that grows over time.

Instant Issue Life Insurance: Quick, Easy, and Convenient

You may want to see also

Explore related products

![]()

Universal life insurance is more flexible, allowing adjustments to premium payments and death benefits

Universal life insurance and whole life insurance are both permanent life insurance policies that offer lifelong coverage. However, they differ in terms of flexibility. Universal life insurance is more flexible than whole life insurance, allowing adjustments to premium payments and death benefits.

Whole life insurance has fixed premium payments, a guaranteed death benefit, and a fixed interest rate on the policy's cash value. It offers permanent, stable protection and is designed for those who want a simple and predictable policy that doesn't require active monitoring.

On the other hand, universal life insurance offers flexibility throughout the duration of the policy. It allows you to adjust your premium payments and, in some cases, your death benefit as your income and needs change. This adaptability makes it suitable for individuals with fluctuating incomes or those who want to adapt their policy as their life circumstances change.

The cash value of a universal life insurance policy is based on market conditions and can change over time. While it offers a guaranteed minimum interest rate, the cash value accumulation can vary based on factors such as funding methods and investment choices. This flexibility allows policyholders to customise their protection and make adjustments as needed.

Universal life insurance provides the ability to fully customise your coverage upfront and make changes later. You can design your policy to last for a specific duration or your lifetime, depending on your preferences. This flexibility allows you to tailor the policy to your specific needs and circumstances.

Life Insurance: Irrevocable Beneficiary, Possible?

You may want to see also

Explore related products

![]()

Whole life insurance has a fixed interest rate on the policy's cash value

Whole life insurance and universal life insurance are both permanent life insurance policies that offer lifelong coverage. However, whole life insurance is generally simpler and more predictable, while universal life insurance offers more flexibility.

The fixed interest rate on the cash value of a whole life insurance policy provides a stable and consistent increase in value over time. This accumulation of cash value is guaranteed and is not dependent on market conditions or the performance of investments. The cash value can be used to cover unexpected expenses, provide additional income during retirement, or even be used for education costs.

In contrast, universal life insurance offers a variable interest rate that is based on market conditions and the performance of investments. While universal life insurance may offer a guaranteed minimum interest rate, the cash value can fluctuate over time. This flexibility allows policyholders to adjust their premium payments and death benefits as their circumstances change.

Ultimately, the decision between whole life and universal life insurance depends on an individual's specific needs and preferences. Whole life insurance may be preferable for those who want guaranteed premiums, death benefits, and cash values, while universal life insurance offers the advantage of flexibility and the ability to adapt the policy over time.

Canceling CIBC Mortgage Life Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

$15.95

![]()

Universal life insurance offers the ability to customise your protection upfront and make adjustments over time

Universal life insurance is a form of permanent life insurance that offers lifelong protection and the flexibility to adjust your policy coverage as needed. It is a highly customisable policy that allows you to adjust your coverage to fit your budget and goals. This flexibility makes it a good fit for individuals with growing families, fluctuating incomes, or long-term financial goals.

The key difference between whole life and universal life insurance is the level of flexibility offered. Whole life insurance is generally simpler and more predictable, with fixed premium payments, a guaranteed death benefit, and a fixed interest rate on the policy's cash value. On the other hand, universal life insurance allows for more flexibility in premium payments, death benefits, and interest rates.

With universal life insurance, you can customise your protection upfront by choosing the benefits you want and setting your own payment schedule and level of coverage. This upfront customisation allows you to design your coverage duration, ranging from as little as fifteen years to your entire lifetime.

Additionally, universal life insurance offers the ability to make adjustments over time. You can modify your premium payments, death benefit amounts, and the accumulation rate of cash value within the policy. These adjustments can be made in response to changing financial needs, significant life events, or fluctuations in income. It is important to note that adjusting the coverage may impact your premium payments and the overall performance of the policy.

By offering upfront customisation and the ability to make adjustments, universal life insurance provides a flexible solution that adapts to the evolving needs of individuals and their families.

Life Insurance for Underground Miners: Is It Possible?

You may want to see also

Explore related products

![]()

Whole life insurance is more expensive than universal life insurance

Whole life insurance and universal life insurance are both permanent life insurance policies that provide lifelong coverage and a death benefit to your heirs when you die. However, whole life insurance is more expensive than universal life insurance. This is because whole life insurance offers a guaranteed death benefit, predictable premiums, and a cash value that is guaranteed to grow. On the other hand, universal life insurance offers flexibility in premium payments and death benefits, and an interest rate that varies based on market conditions.

Whole life insurance has fixed premium payments that are guaranteed not to change, and you can pay them over your lifetime. The cash value of a whole life insurance policy grows at a fixed rate, making it simpler and more predictable than other permanent life insurance types. The money can be used whenever you need it, for whatever you choose, such as covering unexpected medical costs or providing additional income in retirement. Whole life insurance also often earns dividends, which can be used to pay premiums, increase the cash value, or be taken as cash. These features make whole life insurance more expensive than universal life insurance.

Universal life insurance, on the other hand, offers flexible premium payments and death benefits. You can adjust the amount and timing of premium payments to fit your needs, allowing you to build up cash value quickly or slow your contributions as your income and expenses change. Universal life insurance also offers an interest rate that varies based on market conditions, which can lead to higher returns but also carries more risk. While universal life insurance can build cash value, it may fluctuate over time based on factors such as how you fund the policy and the investments your insurance company chooses. Universal life insurance does not typically earn dividends, which can make it less expensive than whole life insurance.

The choice between whole life and universal life insurance depends on your unique situation and needs. Whole life insurance is best for those who want a permanent policy that they don't need to monitor closely, with guaranteed benefits and a growing cash value. Universal life insurance, on the other hand, is better for those who want the flexibility to adjust their coverage and premium payments over time as their needs change.

Contacting MetLife: Insurance Claims and Queries

You may want to see also

Frequently asked questions

Whole life insurance is a permanent life insurance plan that provides coverage for the insured's entire lifetime, as long as the required premiums are paid. Whole life insurance has a cash savings component, known as the cash value, which the policy owner can draw on or borrow from. Whole life insurance premiums tend to be higher than those of term life insurance, but they are level and do not change over time.

Universal life insurance is a form of permanent life insurance that has a cash value element and offers lifetime coverage as long as you pay your premiums. Universal life insurance is flexible, allowing you to raise or lower your premiums within certain limits. It can be cheaper than whole life insurance. However, if your investments underperform or you underpay for too long, it could affect your death benefit or cause your policy to lapse.

Whole life insurance premiums are typically fixed for the duration of the policy, whereas universal life insurance premiums can be adjusted within certain limits. Whole life insurance also guarantees a fixed interest rate on the cash value, while universal life insurance interest rates can change frequently, although there is usually a minimum rate.