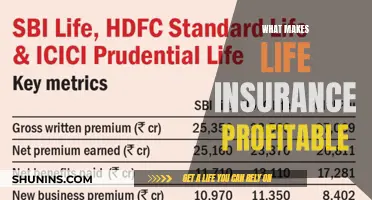

When it comes to life insurance, there are a few key considerations to keep in mind. Firstly, it's important to decide if you truly need it, what type of policy is best suited to your needs, and how much coverage you should opt for. The mode of premium payment, or the frequency of payments, can also significantly impact the overall cost of your life insurance. While paying annually may require a larger upfront sum, it often works out to be more cost-effective than paying monthly, quarterly, or semi-annually. This is because insurance companies need to offset the uncertainty and higher collection costs associated with more frequent payments. Additionally, factors such as age, gender, health, and lifestyle can influence the premium rates offered by insurance providers. Ultimately, the best approach is to carefully review your options, seek expert advice, and choose a policy that aligns with your budget and financial considerations.

| Characteristics | Values |

|---|---|

| Least expensive premium | Term life insurance |

| Most secure form of insurance | Whole life insurance |

| Most flexible form of insurance | Universal life insurance |

| Least frequent payment mode | Annual |

| Most frequent payment mode | Monthly |

| Cost per year for annual payment | $1,250 |

| Cost per year for semi-annual payment | $1,400 |

| Cost per year for quarterly payment | $1,600 |

| Cost per year for monthly payment | $1,800 |

| Factors influencing premium | Age, sex, health rating, assumed rate of return, payment mode, additional riders, death benefit |

Explore related products

What You'll Learn

- Annual premium payments are the cheapest mode for a year's coverage

- Less frequent payments are more cost-effective overall

- Monthly payments are more manageable but cost more in total

- Universal life insurance offers flexibility on premium payments

- Whole life insurance is the most secure form of insurance

![]()

Annual premium payments are the cheapest mode for a year's coverage

Life insurance is an important financial product that can provide peace of mind and security for individuals and their loved ones. When considering life insurance, it is essential to think about not only the level of coverage but also the mode of premium payments. The mode of premium payment refers to the frequency with which an individual pays their life insurance premiums, and it can have a significant impact on the overall cost of the policy.

While at first glance, it may seem more manageable to pay life insurance premiums monthly, quarterly, or semi-annually, the annual premium payment option is the most cost-effective in the long run. This is because insurance companies offer discounts for larger, upfront payments, and there are fewer administrative costs involved. For example, an annual premium payment of $1,250 would cost less than paying $150 per month, $400 per quarter, or $700 semi-annually. While the upfront cost of an annual payment is higher, it is the cheapest option for a full year's coverage.

The reason more frequent payment modes tend to be more expensive is that insurance companies need to offset the uncertainty and higher collection costs associated with more frequent payments. By receiving a full year's worth of payments upfront, insurance providers can worry less about late or missing payments in the future, improving their cash flow and making it easier to predict their financial status. Additionally, they can use the extra money to make larger, earlier investments.

It is worth noting that the mode of premium payment is usually flexible, and individuals can often switch between different payment frequencies. However, insurance providers typically align the new payment mode with pre-existing payment dates. For example, if an individual switches from semi-annual to monthly payments, their first monthly payment will likely be due on the next scheduled semi-annual payment date.

When deciding on the mode of premium payment, it is essential to consider opportunity costs and liquidity. While annual premium payments result in the lowest overall cost, this option may not be feasible for those with limited cash reserves. In such cases, a more frequent payment mode may be more suitable, even if it results in a higher total cost over the policy's life.

In conclusion, while there are various payment options available for life insurance policies, annual premium payments are the cheapest mode for a year's coverage. However, individuals should carefully consider their financial situation and choose a payment mode that aligns with their budget and cash flow.

Retirement Funds for Life Insurance: A Smart Move?

You may want to see also

Explore related products

![]()

Less frequent payments are more cost-effective overall

When it comes to life insurance, the mode of premium payment reflects how often you pay your premiums. The frequency of payment is different from the payment method, which refers to how you pay, such as by cheque or credit card.

While more frequent modes of premium payment tend to cost less per payment, they tend to cost more in total over the long term. This is because insurance companies need to offset the uncertainty and higher collection costs associated with more frequent payments. For example, an insurer might charge you $150 per month, $400 per quarter, $700 every six months, or $1,250 per year. While the annual payment option has the highest upfront cost, it is the cheapest mode for an entire year's worth of coverage.

Monthly payment plans typically result in higher overall costs compared to other payment modes due to the additional fees and administrative costs associated with processing more frequent payments. For instance, if the total annual premium for insurance is $1,200, paying it monthly might incur an extra $100 in fees, resulting in a total of $1,300 for the year. In contrast, paying annually would only be $1,200 without any extra charges.

Therefore, if you're looking to minimise your insurance costs, choosing a less frequent payment mode like annual payments is usually more cost-effective. However, it's important to consider your liquidity, which is the amount of cash you have ready to make premium payments. If you only have a small amount of money in the bank, it may not be wise to choose a large annual premium payment option.

Mental Illness: Life Insurance Options and Obstacles

You may want to see also

Explore related products

![]()

Monthly payments are more manageable but cost more in total

When it comes to life insurance, the mode of premium payment reflects how often you pay your premiums. It's worth noting that the more frequent the payments, the lower each individual payment will be. However, due to fees, more frequent payments will generally cost more over the long term. This means that while monthly payments can make premiums more manageable, they will also cost more in total.

Let's take a look at an example to illustrate this point. Suppose an insurer charges $150 per month, $400 per quarter, $700 semi-annually, or $1,250 for an annual payment. While the monthly option may seem like the most manageable option, it will cost you $1,800 over the year. In contrast, the annual payment option will cost you $1,250 for the entire year, making it the cheapest mode for a year's worth of coverage. This is because insurance companies value receiving a full year's worth of payments upfront, reducing the uncertainty of late or missing payments in the future.

It's important to consider your liquidity when choosing a payment mode. Liquidity refers to the amount of cash you have readily available to make premium payments. If you don't have much money in the bank, choosing a high annual premium payment option may not be feasible. In such cases, a monthly payment plan can provide more flexibility by allowing you to budget your insurance costs as part of your monthly expenses.

Additionally, it's worth noting that some insurers offer discounts for larger, less frequent payments, such as annual premium payments. This is because they require less administrative work for the insurer. However, if you decide to terminate your policy early, keep in mind that many insurance providers will not refund portions of premiums already paid. Therefore, choosing a monthly payment plan can provide more flexibility if you're unsure about committing to a long-term policy.

Who is a Payor in Life Insurance and Why?

You may want to see also

Explore related products

![]()

Universal life insurance offers flexibility on premium payments

When it comes to life insurance, there are several factors to consider, such as the purpose of the insurance, the amount of coverage needed, and the mode of premium payment. The mode of premium payment refers to the frequency of payments, which can be annual, semi-annual, quarterly, or monthly. While more frequent payment modes tend to cost more per payment, less frequent payments, such as annual payments, result in a lower overall cost for the year. Therefore, to secure the lowest cost for life insurance, choosing a less frequent mode of premium payment is generally recommended.

Universal life insurance is a type of permanent life insurance that offers flexible premium payments, lifelong coverage, and the ability to build cash value over time. Unlike whole life insurance policies, which have fixed premiums, universal life insurance allows policyholders to adjust their premium payments within certain limits. This flexibility can be advantageous for those with fluctuating incomes or changing financial responsibilities.

One of the key features of universal life insurance is its investment savings component. Policyholders can pay more than the cost of insurance, and the excess premium is added to the cash value of the policy, earning interest over time. This cash value can then be borrowed against or withdrawn in the form of loans. Additionally, universal life insurance provides the option to increase or decrease coverage without purchasing a new policy, making it a flexible option for those whose insurance needs may change over time.

However, it is important to note that universal life insurance policies typically do not have fixed interest rates, which can make them less predictable. Policyholders need to monitor the cash value of their policies to ensure they remain adequately funded. If the policy becomes underfunded, large payments may be required to keep the coverage active. Additionally, the performance of investments and the level of premium payments can impact the death benefit.

Overall, universal life insurance offers flexibility in premium payments, allowing policyholders to adjust their payments within certain limits. This flexibility can be beneficial for those seeking lifelong coverage with the ability to adapt their insurance to changing circumstances. However, it is important to carefully consider the pros and cons of universal life insurance and consult with insurance providers to determine the best option for one's specific needs.

Universal Life Insurance: More Problems Than Solutions?

You may want to see also

Explore related products

![]()

Whole life insurance is the most secure form of insurance

When it comes to life insurance, there are a variety of options to choose from, each with its own set of advantages and disadvantages. Whole life insurance is one such option that stands out for its comprehensive coverage and long-term financial security. It is widely regarded as the most secure form of insurance, offering a range of benefits that provide peace of mind and stability for individuals and their families.

One of the key advantages of whole life insurance is its longevity. Unlike term life insurance, which only covers a specified period, whole life insurance provides coverage for an individual's entire lifetime, as long as the premiums are paid regularly. This means that policyholders can rest assured that their loved ones will be financially protected, regardless of when the unexpected occurs. The policy includes a savings component, known as the "cash value," which grows over time and can be accessed or borrowed against to fund significant purchases, such as a home, or to supplement retirement income.

Whole life insurance also offers a guaranteed death benefit, ensuring that beneficiaries receive a payout upon the insured's death. This benefit remains intact even if the insured becomes disabled or critically ill and is unable to continue making premium payments. Additionally, the death benefit continues to earn interest until it is paid out, providing even greater financial support to the beneficiaries. This level of security and predictability is especially valuable for families who rely on the income of a single breadwinner, as it helps maintain their standard of living in the event of an untimely loss.

Furthermore, whole life insurance provides stability through its level premium payments. Unlike other insurance types, whole life insurance premiums remain consistent throughout the policy's duration, making it easier for policyholders to plan their finances without worrying about unexpected increases in premium costs. The cash value component of whole life insurance also guarantees growth over time, allowing policyholders to build wealth and access funds when needed. This feature makes whole life insurance not just a safety net but also a valuable investment tool.

While whole life insurance is generally considered the most secure form of insurance, it is important to remember that the best insurance plan depends on an individual's specific needs and circumstances. Factors such as age, health, financial obligations, and long-term goals should be carefully considered when choosing an insurance policy. Consulting with a knowledgeable insurance agent or financial advisor can help individuals make informed decisions and tailor their insurance plans to their unique situations.

Life Insurance and Mortgages: What's the Connection?

You may want to see also

Frequently asked questions

Annual payments are the cheapest mode for a year's worth of coverage. Monthly, quarterly, and semi-annual modes would cost $1,800, $1,600, or $1,400 per year, respectively, versus the $1,250 annual payment.

The minimum amount of coverage you need depends on your personal situation. Financial experts often recommend purchasing at least 10 times your annual income in coverage. You should also consider any debts you want to be paid off, such as mortgages, loans, and credit cards, as well as future expenses like your children's tuition and funeral expenses.

Term life insurance provides coverage for a specific period, whereas permanent life insurance provides coverage for your entire life. Term insurance is usually the least expensive option, but permanent insurance offers more flexibility and the possibility of building cash value.

Younger people generally pay lower premiums than older people because they are less likely to have health problems. The cost of life insurance tends to increase with age as health risks become higher.

Yes, most insurers allow policyholders to change the mode of premium payments during the life of the policy. You may need to plan ahead and confirm the new payment schedule with your insurer.