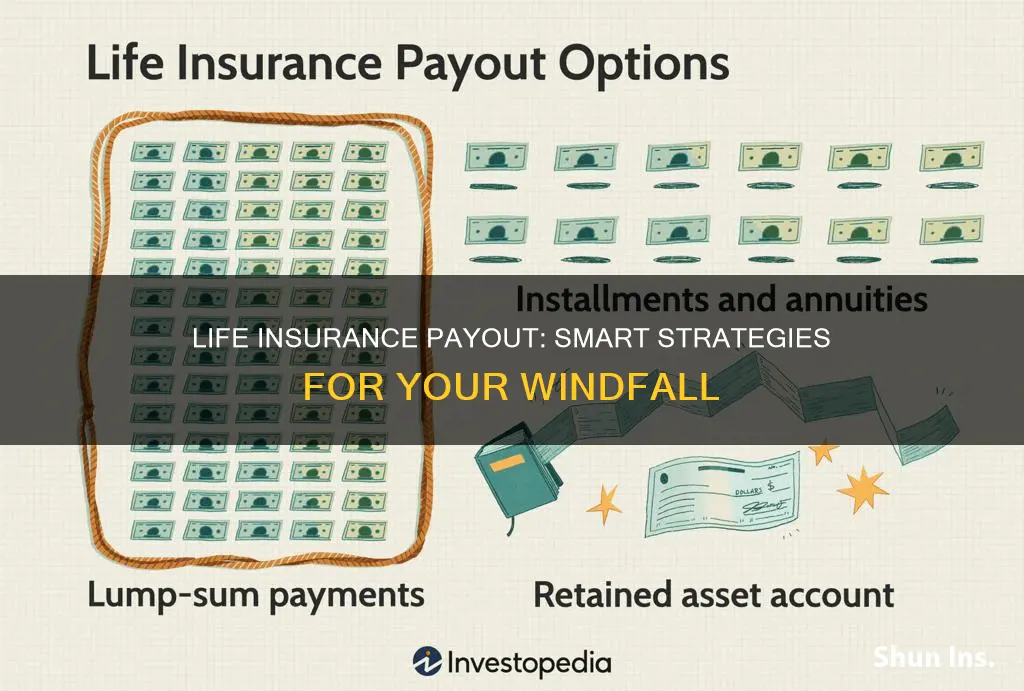

Life insurance is a contract between a policyholder and an insurance company that pays out a death benefit when the insured person passes away. There are several types of life insurance, including term and permanent plans, and the death benefit can be paid out in different ways. The most common way is a lump-sum payment, where the beneficiary receives the entire death benefit at once. This gives the beneficiary the most flexibility, but it can be overwhelming to receive such a large amount of money at once. Other options include installment payments, annuities, and retained asset accounts. Installment payments are made on a regular schedule, such as monthly or annually, over a certain period of time. Annuities provide a steady income stream to the beneficiary, while retained asset accounts allow the beneficiary to withdraw funds as needed. It's important to understand the different payout options and their potential tax implications before choosing how to receive a life insurance payout.

| Characteristics | Values |

|---|---|

| Number of Payouts | One-time or Installments |

| Payout Amount | Full amount or Percentage |

| Payout Period | Immediate or Fixed Period or Lifetime |

| Payout Mode | Lump-sum or Annuity or Retained Asset Account |

Explore related products

What You'll Learn

![]()

Paying off debt

If you're buried in debt, it might make sense to take the lump-sum payout and rid yourself of high-interest credit card balances or student loans. This will free up disposable income that can be redirected to a retirement account or a savings account for short-term goals, such as a down payment for a house.

There are two types of life insurance policies that can be used to pay off debt: term life insurance and permanent life insurance. Term life insurance is usually more affordable, but permanent life insurance can offer added benefits such as cash value accumulation. With term life insurance, you can choose a term length that matches the length of the loan. For example, if you have a 20-year mortgage, you can buy a 20-year term life policy. Permanent life insurance, on the other hand, lasts your entire life and can be used to pay off debt at any time.

If you have whole or universal life insurance coverage, your policy accumulates a cash value that you can withdraw and use to pay off debt. This can save you hundreds or even thousands in total interest. However, anything you withdraw will eventually be deducted from the death benefit, and you may have to pay taxes on the withdrawn amount, depending on how much you take out.

Before using your life insurance payout to pay off debt, consider how it will affect your family's financial needs. If you're still working and have existing debts, you should figure out how much coverage you need and how to supplement it if your cash value is reduced. You could purchase a term life policy to maintain life insurance coverage while paying lower monthly premiums.

Life Insurance and Grand Mal Seizures: What You Need to Know

You may want to see also

Explore related products

![]()

Creating an emergency fund

The amount you need in your emergency fund depends on your situation. Most experts recommend saving at least $1,000, while some suggest saving four to eight months' worth of income. You can also aim to cover essential expenses, such as housing, transportation, and food, for three to six months.

To build your emergency fund, consider creating a budget and a sustainable savings plan. Put aside a small amount each month and, if possible, automate the savings transfer. Keep your emergency fund in a separate account to make it harder to spend the money on non-emergencies. You can also protect your retirement savings by accumulating an emergency fund of at least six months' worth of living expenses.

Variable Life Insurance: Invest and Insure

You may want to see also

Explore related products

![]()

Purchasing an annuity

Annuities are a type of insurance contract designed to turn your money into future income payments. You can buy an annuity with either a lump sum payment or several payments over time. You can set up the annuity with a growth period, where it builds your savings. The return depends on the type of annuity. For example, a fixed annuity pays a guaranteed interest rate, while a variable annuity lets you invest your savings in mutual funds.

When you're ready, you can start collecting income payments from the annuity. You can set these up over a fixed period or have them guaranteed for life. Annuities can be a form of insurance against outliving your savings.

You can set up a death benefit on an annuity contract. With this feature, the annuity would give your heir a payout based on the contract terms and your balance. For example, if you bought an annuity for $500,000 and collected $300,000 of income payments, the annuity death benefit might pay the remaining $200,000 to your heirs.

There are several types of annuity payouts. The most common death benefit is the contract value or the premiums paid, whichever is greater. You can also select the amount you want to receive each month, but the insurance company does not guarantee that you won't outlive your income payments. You can choose a defined period (e.g. 10, 15, or 20 years) to receive the payout, and payments after your death may go to your designated beneficiary. The company can also pay you or your survivor for as long as either of you lives, although the amount of the regular payments is typically smaller.

If you receive a life insurance payout, especially a large one, it's best to delay any immediate financial decisions. Taking time to research options and gather advice from knowledgeable sources can help you make an informed decision.

U.S. Military Life Insurance: War Clause Coverage?

You may want to see also

Explore related products

![]()

Investing for growth

If you don't need the money from your life insurance payout immediately, you may want to consider investing it for growth. This means buying investments that focus on capital appreciation. You won't receive money until you sell the investment, but if you hold it long enough, you have the potential to make much more money than you spent.

- Growth stocks: These are stocks of growth-oriented businesses, including industries such as technology, healthcare, and consumer goods. Growth companies traditionally work well for investors focused on the future potential of companies. While growth stocks can be volatile, they tend to provide the best return on investment over time. Some popular growth companies include firms like Google, Apple, and Tesla.

- Index funds: Index funds are considered low-risk because they are highly diversified. You can usually get an S&P 500 index fund or another index for a low price and minimal fees. Index funds also tend to be tax-efficient and have high returns that beat most actively managed mutual funds.

- Real estate: Real estate can be an excellent way to create a passive income. You could buy properties to rent out to tenants, or invest in online real estate investment platforms such as Fundrise or YieldStreet. Another option is to buy real estate investment trusts (REITs), which are companies that pool investors' money to buy and manage real estate properties.

- Alternative investments: Some alternative investments, such as cryptocurrency or fine wine, can have higher gains than standard investments. However, don't make your entire investment portfolio consist of alternative investments.

When investing for growth, you can store your investments in taxable brokerage accounts and tax-advantaged accounts. Retirement accounts are either tax-deferred or funded with post-tax money that grows tax-free. Taxable brokerage accounts have no contribution limits and the money is liquid, but you will need to pay taxes on any gains when you sell.

Travelers' Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Paying off a mortgage

Life insurance can be used to pay off your mortgage if you die. This strategy often involves a decreasing-term policy, meaning that your payout reduces as you gradually pay off your mortgage. A life insurance claim is typically paid out as a lump sum.

There are two main options for using life insurance to pay off your mortgage:

Option 1: Using one policy

You can purchase a term life insurance policy with a benefit amount that matches the outstanding balance of your mortgage. This policy lasts for the full term of your mortgage (usually 30 years). In the event of your passing, your family can use the death benefit to either pay off the mortgage or make continued mortgage payments.

Option 2: Using two policies

You can purchase a whole life insurance policy to provide long-term coverage that fits your financial situation. Additionally, you can buy a term life insurance policy to cover the balance of your mortgage for the early period (10 to 15 years) when the amount owed is the highest. This will allow your family to pay off the mortgage or continue making payments if something happens to you.

It is important to remember that you have financial obligations beyond your mortgage. Therefore, you will probably want any coverage to cover additional expenses, such as childcare, saving for retirement, and medical expenses. Your coverage should take your entire range of financial needs into account.

Shopping for Life Insurance? Compare Policies to Save

You may want to see also

Frequently asked questions

You can receive your life insurance payout in a few different ways, depending on the insurer. The most common is a lump-sum payment, where you receive the entire payout all at once. You can also choose to receive your payout in installments, either for a set period of time or for life. Another option is a retained asset account, where the insurer holds onto your payout and you can withdraw funds as needed.

A lump-sum payment gives you the most flexibility to use the money as you see fit. However, receiving a large amount of money at once can be overwhelming, and it's up to you to make the money last. Additionally, if your payout is large, you may need to spread it across multiple accounts to ensure it's all protected by deposit insurance.

An installment plan can provide a steady income stream, making financial planning easier. However, the insurance company is just guessing how much money to give you based on how long they think you'll live, and if you pass away before you receive the entire payout, the remaining money goes back to the insurance company.

A retained asset account offers flexibility and easy access to your funds, and it earns interest. However, the interest earned may be subject to taxes, and you have no control over how the insurance company chooses to invest your money.

There is no time limit to claim life insurance, but it's best to file a claim as soon as you can. The insurance company will then review your claim, which can take up to 30 days in most states. If your claim is approved, you will typically receive the payout within 60 days, but there may be delays due to issues such as incomplete paperwork or if the policyholder died within the first two years of the policy.