Life insurance is worth considering if your death would place a financial burden on your dependents. The payout from a valid life insurance claim could provide a financial lifeline for your family, helping them maintain their standard of living in your absence. However, if your death wouldn't financially impact anyone, the money spent on premiums may be better invested elsewhere. Additionally, if the cost of coverage exceeds the potential payout, as is often the case for older individuals or those with serious health conditions, life insurance may not be a worthwhile investment.

| Characteristics | Values |

|---|---|

| If your death would place a financial burden on others | Life insurance is worth it |

| If you want to cover your own burial costs | Life insurance is worth it |

| If you want to replace your income | Life insurance is worth it |

| If you want to cover your debts | Life insurance is worth it |

| If you're older or have a serious health condition | Life insurance may not be worth it |

| If your death wouldn't leave someone in a financial bind | Life insurance may not be worth it |

| If you don't have anyone depending on you financially | Life insurance may not be worth it |

| If you're retired and well-off financially | Life insurance may not be worth it |

| If you're not the breadwinner | Life insurance can still be worth it |

| If you want to build wealth | Life insurance may not be worth it |

Explore related products

What You'll Learn

![]()

If you have financial dependents

If you have people in your life who are financially dependent on you, life insurance is probably worth considering. This is true whether you are the primary breadwinner or not. If your death would place a financial burden on your dependents, then life insurance can help alleviate that burden. For example, if you are a stay-at-home parent, your working spouse might need to hire a nanny or cleaner if you were to pass away. Life insurance could help cover these costs.

The same is true if you have minor children who are financially dependent on you. If your income were to suddenly disappear, your children could be put at a major disadvantage. A life insurance policy can help cover these expenses and provide for your children's future. This is also the case if you are helping to cover college costs or providing support for someone with a disability.

Life insurance can also help cover funeral costs, which can be significant, as well as any debts you may have, such as a mortgage, car loans, or student loans. By taking out a life insurance policy, you can ensure that your loved ones are not left with these financial burdens in the event of your death.

It's important to note that life insurance is not a savings or investment product and should not be treated as such. The primary purpose of life insurance is to provide financial protection for your dependents in the event of your death. If you don't have any financial dependents, then life insurance may not be necessary, and you may be better off investing your money elsewhere.

When considering life insurance, it's crucial to factor in the cost of the policy. The younger and healthier you are, the better rates you are likely to get. If you are older or have a serious health condition, the potential payout may not be worth the cost of the policy. In such cases, you may be better off putting your money into a savings account or other long-term investments.

Switching from Group Insurance to Whole Life: What's Involved?

You may want to see also

Explore related products

![]()

If you want to cover funeral costs

If you want to ensure your funeral costs are covered, you may want to consider taking out a life insurance policy. Funerals can be expensive, with the average cost of a funeral being $8,300, and your loved ones may not have the funds to cover the bill.

There are a few different types of life insurance policies that can help cover funeral costs. One option is burial insurance, also known as funeral or final expense insurance, which is a type of whole life insurance policy designed to cover funeral, burial, and other end-of-life expenses. Burial insurance is often more affordable than other types of life insurance, even for older applicants, due to its lower coverage amounts. It also doesn't usually require a medical exam to qualify, making it accessible to those without health insurance or with pre-existing conditions. Another option is term life insurance, which can provide coverage for a specific period, such as 10, 20, or 30 years. This may be a more feasible option if you're on a tight budget, as the premiums for permanent life insurance can run into several hundred dollars a month.

When deciding on the type of policy and the coverage amount, it's important to consider your monthly expenses, immediate needs, and potential funeral expenses. You can use an online calculator to estimate the cost of your funeral and burial services, which can help you determine the coverage amount you need. It's also worth noting that the younger and healthier you are, the cheaper the coverage will be, so it may be beneficial to lock in a lower rate when you're younger.

In addition to covering funeral costs, life insurance policies can also provide financial support for your loved ones by replacing your income, covering any debts or outstanding loans, and paying off medical bills. However, it's important to consider your financial situation and budget before taking out a life insurance policy. If the premiums are not within your long-term budget, it may not be worth the potential payout.

Does AARP's Guaranteed Life Insurance Offer Cash Value?

You may want to see also

Explore related products

![Property and Casualty Insurance License Exam Study Guide: Property Casualty Insurance Book and Practice Test Questions [3rd Edition]](https://m.media-amazon.com/images/I/71MhA+5nDML._AC_UY218_.jpg)

![]()

If you want to replace your income

Life insurance is a way to help replace your income and protect your family if you are no longer around to contribute financially. It is a crucial safety net for many families, ensuring they have financial support if you cannot work due to illness, injury, or death. Income replacement insurance offers financial stability by covering essential expenses, such as mortgage payments, groceries, and utility bills, and helps to maintain the family's standard of living.

When calculating how much life insurance you need to replace your income, a common guideline is to multiply your annual salary by the number of years you want to cover. For example, if your annual salary is $60,000 and you want to provide your beneficiaries with five years of coverage, you will need a $300,000 policy. This calculation only reflects your base salary, and it is important to also consider any anticipated raises, inflation, and additional expenses like college fees or medical expenses.

It is worth noting that there is no one-size-fits-all approach to income replacement life insurance. While a common recommendation is to have coverage worth 5 to 10 times your gross annual salary, this may not be suitable for everyone. Other factors to consider include your age, occupation, health status, and income level. Additionally, if you have older dependents, you may not need as many years of income replacement compared to those with younger dependents.

Term life insurance is the cheapest type of coverage and is typically sufficient for most families. You can match the term policy length to the length of time you want coverage, such as a 20-year term policy to cover your income while your children are still at home. On the other hand, whole life insurance provides permanent coverage and pays out a death benefit regardless of when you pass away. While it tends to be more expensive, it offers more living benefits, such as accumulating cash value that can be borrowed against for emergencies or large purchases.

Income replacement insurance is not just for those in high-risk jobs but is an essential part of financial planning for anyone who relies on their income, including sole breadwinners, dual-income families, the self-employed, and employees without employer coverage. It provides peace of mind and ensures that your loved ones will have financial security if something unexpected happens to you.

Life Insurance: Choosing the Right Coverage Duration

You may want to see also

Explore related products

![]()

If you want to cover debts

Life insurance is a financial safety net for your loved ones in the event of your death. It can be a valuable tool to protect your family from financial difficulties. If you have debts that would be burdensome for your family if you were to die, life insurance is likely a smart move. It can be used to cover final expenses, such as a burial or cremation, and to pay off any outstanding debts.

The cost of life insurance increases with age. The younger and healthier you are, the cheaper the coverage. So, it may be worth getting a life insurance policy when you are younger to lock in a lower rate. If you are older or have a serious health condition, the potential life insurance payout may not be worth the cost. For example, an older person may pay more in insurance premiums over a certain number of years than the eventual payout. In this case, they may be better off putting their money in a savings account.

Term life insurance offers coverage for a limited period, and if you outlive that term, the policy expires without any benefit payout. Term life insurance is typically less expensive than other types of life insurance. Permanent life insurance policies generally do not expire as long as you keep up with premium payments. Permanent life insurance policies also typically accumulate cash value on a tax-deferred basis. However, permanent life insurance is considerably more expensive and may not be a good fit for everyone.

If you are considering life insurance to cover debts, it is important to weigh the pros and cons based on your personal circumstances before choosing a policy. Alternatives such as investments or self-funding can offer comparable benefits without the commitment that comes with life insurance. If you are retired and well-situated financially, for example, you may want to focus on estate planning or prepaying funeral costs instead of purchasing life insurance.

Individual vs Group Life Insurance: What's the Difference?

You may want to see also

Explore related products

$9.97 $19.99

$8

![]()

If you're a stay-at-home parent

Life insurance for stay-at-home parents is crucial as it helps cover household expenses, childcare costs, provides options for the surviving spouse, and ensures a financial cushion for the family's future. While stay-at-home parents may not have a salary, their contributions to the family are invaluable and often underestimated. From childcare and homeschooling to cooking and grocery shopping, the work of a stay-at-home parent would cost a family hundreds or even thousands of dollars a month.

The death benefit from a life insurance policy can assist in covering these costs in the event of the stay-at-home parent's passing. It can also help with other household expenses, such as food, utilities, and mortgage or rent payments. The surviving spouse would likely have more responsibilities and would need to balance family and work obligations during an already stressful time. Life insurance can provide the financial support needed for the spouse to stay at home for a longer period.

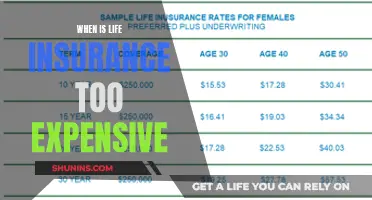

When considering life insurance for a stay-at-home parent, it's important to factor in the cost of covering all the unpaid work they do, as well as future expenses such as childcare and college tuition. While there is no one-size-fits-all answer, a general guideline is to get a 15- to 20-year policy of at least $250,000 to $400,000. It's also worth considering Fixed Indexed Universal Life (FIUL) products, which provide coverage in the case of unexpected death and may include benefits for critical, chronic, or terminal illness.

By securing a life insurance policy, you recognize the invaluable contributions of the stay-at-home parent and ensure that your family's needs will be taken care of in the unfortunate event of their absence. It's a way to provide a financial cushion for your family when they need it most.

Who Should You Name as Your Life Insurance Beneficiary?

You may want to see also

Frequently asked questions

Life insurance is worth it if your death would place a financial burden on other people.

Here are some reasons to get life insurance:

- You want to cover your own burial costs

- You want to replace your income if your salary is relied upon by a child or spouse

- You want to cover your debts

Here are some reasons to avoid life insurance:

- You don't have anyone who relies on you financially

- You're retired and well-situated financially

- You're unable to afford the premiums

Some factors to consider include your age, gender, health status, and coverage amount.

There are two main types of life insurance policies: term life insurance and whole life insurance. Term life insurance provides coverage for a set term, typically between 10 and 30 years, while whole life insurance is a permanent policy that provides coverage for the rest of your life.