When an insured individual selects the extended term nonforfeiture option, they are able to use the cash value from their original policy to purchase a term insurance policy. This new policy will have the same face amount, or level of insurance protection, as the original policy. The insured individual will not need to pay any additional premium and will maintain the same level of coverage as before, but only for a limited time. It is important to remember that term insurance is temporary and not permanent. This option is particularly useful when a policy lapses due to non-payment or when the policyholder chooses to surrender their coverage, as it helps protect the accumulated cash value.

| Characteristics | Values |

|---|---|

| Face amount of term insurance purchased | Equal to the original policy |

| Duration of term insurance purchased | As long as the cash values will purchase |

| Additional premium due from the insured | None |

| Coverage | Same as the original policy |

| Duration of coverage | Limited |

Explore related products

$14.97 $30

What You'll Learn

- The insured's cash value will be used to purchase term insurance

- The face amount of the term insurance will be equal to the original policy

- There will be no additional premium due from the insured

- The insured will have the same coverage as the original policy

- The term insurance will only be for a limited time

![]()

The insured's cash value will be used to purchase term insurance

When an insured person selects the extended term nonforfeiture option, their cash value will be used to purchase term insurance. This means that the cash value from their original policy will be used to buy a term policy that will have the same face amount (or insurance protection) as the original policy.

The insured person will not have to pay any additional premium and will have the same coverage as they did in the original policy, but only for a limited time. Term insurance is not permanent and will eventually expire.

The length of the term insurance policy will depend on the amount of cash value that has been accumulated in the original permanent life insurance policy. The more cash value available, the longer the term insurance policy will last.

This extended term nonforfeiture option is one of several options available to policyholders if they stop paying premiums or choose to surrender their policy. It allows them to continue receiving coverage for a limited time without paying any additional premiums.

Other options include cashing in the policy for its surrender value or using the cash value to purchase a reduced paid-up whole life insurance policy, which provides permanent coverage but at a reduced amount.

The extended term nonforfeiture option is a good choice for those who want to continue their coverage for a limited time without having to pay any additional premiums. However, it's important to note that term insurance is not permanent and will eventually expire.

Explore related products

![]()

The face amount of the term insurance will be equal to the original policy

When an insured person selects the extended term nonforfeiture option, they are able to protect the cash value of their life insurance policy in the event of lapsed payments. This means that the policyholder can receive their policy's cash value, either as a lump sum or by applying it to continuing coverage.

The extended term nonforfeiture option is a good choice for those who can no longer pay their premiums but want to retain the value of their life insurance policy. It is important to note that this option may adversely impact coverage, for example, by reducing the face amount or cancelling the policy completely.

The insured person should carefully consider the pros and cons of this option with their insurance agent to make an informed decision about their coverage. The extended term option is often the insurance company's default option.

Explore related products

![]()

There will be no additional premium due from the insured

When an insured person chooses the extended term nonforfeiture option, they are provided with a unique benefit that guarantees the continuation of their insurance coverage over an extended period, typically for the lifetime of the policy, without any further payment of premiums. This option is particularly advantageous for individuals who have diligently paid premiums for a substantial period but now find themselves in a situation where they are unable to continue making regular payments.

The extended term nonforfeiture option serves as a safety net, ensuring that the policy remains active and providing peace of mind to the policyholder. This means that the insurance company will uphold its end of the bargain and provide coverage as outlined in the policy, even though the insured person is no longer paying premiums. This can be particularly reassuring, as it guarantees a continued financial safeguard for loved ones or beneficiaries in the event of an unforeseen incident.

Typically, the duration of the extended coverage is dependent on the policy's cash value and the age of the insured at the time of policy issuance. The insurance company utilizes these factors to calculate an extended term insurance period, ensuring that the cash value covers the policy's cost over that specific period. This calculation is a technical aspect of the process and is carefully performed by insurance experts to provide an accurate and reliable extended term.

During this extended term period, the policy remains active, and the insured individual continues to enjoy the benefits and coverage as if they were still paying premiums. This includes death benefits, which remain intact and are provided to the beneficiaries upon the insured person's demise during the extended term. It is worth noting that the policy's cash value is no longer accessible to the insured during this period, as it is utilized to fund the extended coverage.

Explore related products

![]()

The insured will have the same coverage as the original policy

When an insured individual chooses the extended term nonforfeiture option, they are provided with a crucial safeguard that ensures their insurance coverage persists even if they encounter challenges in paying their premiums. This option is typically available for life insurance policies and offers policyholders a sense of security and peace of mind. By selecting this provision, the insured can maintain the same level of coverage as outlined in their original policy, safeguarding their loved ones' financial well-being.

The extended term nonforfeiture option comes into effect when a policyholder decides to discontinue premium payments for their insurance policy. At this point, the insurance company utilizes the policy's cash value to purchase extended term insurance. This means that the policy's death benefit remains unchanged, providing the insured individual with continuous coverage for a specific period. This period is calculated based on the available cash value and the amount required to cover the policy's face value.

During this extended term period, the insured maintains the same benefits and protections afforded by the original policy. This includes the same level of coverage, ensuring that their beneficiaries will receive the full death benefit should the insured pass away during this time. It is worth noting that the policy does not accumulate any further cash value during this extended term, as the cash value has been utilized to fund the extended coverage. Nonetheless, the insured can rest assured that their original coverage remains intact.

For example, consider an individual with a $100,000, 20-year term life insurance policy. If, after several years, they opt for the extended term nonforfeiture option due to financial constraints, the insurance company will use the policy's accumulated cash value to extend the coverage. Let's say the cash value is sufficient to extend the coverage for another 10 years. During these next 10 years, the insured still enjoys the full $100,000 coverage, and their beneficiaries will receive this amount as a death benefit if needed.

It is important to emphasize that the insured is not required to undergo additional medical exams or provide further evidence of insurability to maintain this coverage. The insurance company simply extends the original policy's terms for a specified duration. This provision offers a valuable safety net for individuals who may be facing temporary financial difficulties or those who wish to redirect their funds elsewhere without sacrificing the security provided by their life insurance policy.

In summary, selecting the extended term nonforfeiture option guarantees that the insured will retain the exact coverage outlined in their original policy, providing a seamless continuation of protection for themselves and their loved ones. This feature is especially beneficial for those who want to ensure their life insurance policy remains active during times of financial readjustment or shifting priorities. By understanding and utilizing this option, policyholders can make informed decisions that align with their long-term financial goals and overall peace of mind.

Explore related products

![]()

The term insurance will only be for a limited time

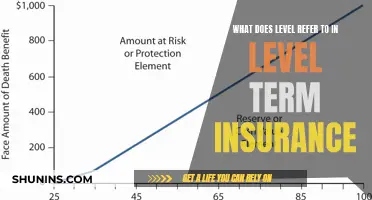

Term insurance is a type of life insurance policy that provides coverage for a certain period of time, or a specified "term" of years. If the insured dies during the specified time period and the policy is active, a death benefit will be paid. Term insurance is much more affordable than permanent life insurance, such as whole life or universal life, as it is not designed to last through old age, when insurance premiums are at their highest.

Term insurance is only for a limited time and does not accumulate cash value. It is a temporary form of insurance. When the insured selects the extended term nonforfeiture option, the cash value is used to purchase term insurance with a face amount equal to the original policy. This means that the insured will have the same coverage as they did previously, but only for a limited time.

The extended term nonforfeiture option is one of three nonforfeiture options available to the owner of a life insurance policy that has accumulated cash value. The other two options are cash surrender and reduced paid-up. With the cash surrender option, the policy is cancelled and the insurer pays out the cash value to the policy owner. The reduced paid-up option uses the cash value from the original policy as a single premium to purchase a paid-up whole life policy with reduced coverage.

The extended term option is the cheapest form of life insurance and does not accumulate cash value. It is a good choice for those who can't or won't pay the much higher monthly premiums associated with whole life insurance. However, it is important to note that if the insured outlives the term and still needs coverage, the price of term insurance typically increases significantly.

Frequently asked questions

A non-forfeiture clause is an element included in standard life insurance and long-term care insurance. It stipulates that the policyholder will receive a partial or full refund of premiums paid if the policy lapses after a defined period due to missed premium payments.

The three non-forfeiture options are: Cash Surrender, Extended Term, and Reduced Paid-up.

The Extended Term option enables the policyholder to use the cash value from the original policy to purchase term life insurance coverage. The length of the term will depend on the amount of cash value accumulated in the original permanent life policy.

The Extended Term Option is often the insurance company's default option.

The Extended Term option helps the policy owner to quit paying premiums for the original policy, but they will still retain the equity accumulated in the policy.