A contracted discount in insurance billing refers to a reduction in the amount charged for a service by a medical provider. This occurs when the provider has agreed to accept a lower rate as part of their contract with the insurer. The difference between the original charge and the contracted rate is known as a contractual adjustment. For example, if a provider charges a practice fee of $100 for a certain service, but the contracted rate with the insurer is $80, the patient will only be responsible for paying the contracted rate, and the remaining $20 will be adjusted off their account as a contractual discount. These contracted rates are typically kept confidential and are often lower than the rates charged to patients without insurance.

| Characteristics | Values |

|---|---|

| Definition | A contractual adjustment is a discount on a patient's bill that a doctor or hospital must write off because of billing agreements with the insurance company. |

| Who is involved | The insurance company, the insured person, and the provider. |

| Who benefits | All three parties involved in the insurance process benefit from the established provider network arrangement. |

| Who decides the discount | Insurance carriers negotiate discounted rates with healthcare providers. |

| Who pays the discounted amount | The insurance company pays the discounted amount. |

| Who is not eligible | A patient who requires a certain medical service that the insurance company does not cover will end up paying the full amount charged by the medical provider with no contractual adjustment to limit the cost. |

| What does it aim to do | Contracted discounts aim to reduce the amount of the service charge, thus reducing the amount owed on the claim. |

| How does it work | The provider usually submits the bill for the provider's standard rate for the service. Assuming the service is covered by the insurance contract, the insurer processes the claim at the agreed-upon service rate. The reduced amount between the provider bill and contract rate is discounted and called a contractual adjustment. |

| Why do providers agree to this | Participating health care providers typically agree to become part of an insurance network in exchange for contractually agreed-upon rates for certain services. Providers that participate believe the broader access to members is worth the contracted rates on services. |

| What is the result | The insurer and provider have a contractual arrangement. When providers agree to accept an insurance plan, the contract will include many details including the amount the insurance company will pay the provider for certain procedures. |

Explore related products

What You'll Learn

- A contractual adjustment is a discount on the amount owed on a claim

- Insurers often pay less than patients think

- Insurers may intentionally confuse patients with unclear explanations of benefits

- Insurers sometimes omit procedure names and codes from bills

- Insurers may not pay anything despite applying a discount

![]()

A contractual adjustment is a discount on the amount owed on a claim

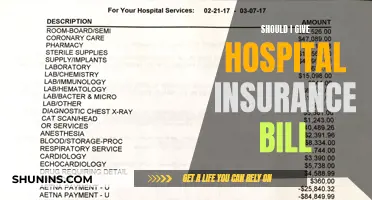

The contractual adjustment is the difference between the billing amount and the maximum allowable charge. The maximum allowable charge is usually paid by the insurance company and is lower than the billing amount charged to the patient. This is because the insurance company has already set this amount beforehand. The hospital is prohibited from charging the remaining amount from the patient.

The contractual adjustment is a write-off that a doctor or hospital must make because of billing agreements with the insurance company. It is the most common type of adjustment. The adjustment is the amount reduced from the medical bill because the patient has a contract with the insurance company.

For example, if a provider charges $100 for a service, and the insurance company's allowance for that service is $80, with the insurer paying $64, or 80%, the remaining 20% of the contracted rate amount is paid by the patient. The $20 difference between the $100 charged by the provider and the $80 collected is adjusted off the patient account as a contractual adjustment.

Contractual adjustment percentages and amounts vary by the type of service provided. They are calculated by dividing the total contractual adjustments made by the provider by the total amount of charges billed for services. This metric helps healthcare providers understand how much revenue they are losing due to contractual adjustments.

Navigating the Insurance Billing Process: Understanding Patient Copays

You may want to see also

Explore related products

![]()

Insurers often pay less than patients think

Patients often assume that their insurance companies are fighting on their behalf for the best prices. However, this is not always the case. Saving patients money is often not their top priority.

The Complicated World of Insurance Billing

The insurance company's "explanation of benefits" is often confusing and misleading. Insurers are paying a lot less than people think they are, and the EOB is designed to perpetuate that confusion. For example, insurers will often impose a discount off the billed price, then add the "discounted amount" and payment together, making it look like the discount and the payment add up to the insurer's contribution. In reality, this is not true.

Insurers also often leave out the procedure name and code, only providing the date of service and the provider name. This makes it difficult for patients to understand what procedure they are being charged for and whether the charge is accurate.

The Middleman Problem

Insurance companies act as middlemen between patients and healthcare providers. They are supposed to negotiate lower prices for their customers, but they don't always do this effectively. In some cases, they agree to pay high prices and then pass those costs on to patients.

This dynamic is particularly problematic when it comes to hospital bills, which can be extremely high. Patients often have no way of knowing how much a procedure will cost until they receive the bill. Even when they try to get an estimate beforehand, they may be given inaccurate or incomplete information.

The Role of Healthcare Providers

Healthcare providers also play a role in this issue. They often charge higher prices for patients with insurance, knowing that the insurance company will cover most of the cost. This practice is known as "cost-shifting".

In some cases, providers may even charge more than the insurance company is willing to pay, resulting in the patient being billed for the remaining amount. This is known as "balance billing".

The Bottom Line

The complex relationship between insurers and healthcare providers can result in higher costs for patients. Patients may end up paying more than they expected, even with insurance. It is important for patients to be aware of these dynamics and to carefully review their bills to ensure they are not being overcharged.

Supplemental Insurance: Understanding the Added Layer of Protection

You may want to see also

Explore related products

![]()

Insurers may intentionally confuse patients with unclear explanations of benefits

One common issue is that insurers will impose a discount on the billed price of a service, but then add the "discounted amount" and the actual payment together on one line, making it seem like the insurance company contributed more than they did. Insurers also often leave out the name and code of the procedure performed, providing only the date of service and the provider's name. This makes it hard for patients to know what they are being charged for and whether the charges are correct.

Additionally, insurance companies sometimes make it difficult for patients to understand whether a service is covered by their plan. They may use vague or confusing language, or provide insufficient information about what is and is not covered. This can result in patients being surprised by unexpected charges or denied claims.

Another way that insurers confuse patients is by making it hard to compare prices and benefits across different plans. They may not disclose denial rates or other important information, making it difficult for consumers to make informed choices about their healthcare coverage.

Overall, the lack of transparency and clarity in insurance explanations of benefits can lead to financial stress and negative health outcomes for patients. It is important for patients to carefully review their explanations of benefits and seek clarification from their insurance company if needed.

Billing Insurance for Mini-Mental Examinations: Understanding Coverage and Reimbursement

You may want to see also

Explore related products

![]()

Insurers sometimes omit procedure names and codes from bills

Insurers often leave out the procedure name and code from bills, leaving the patient with only a date of service and a provider name. This can make it difficult for patients to understand what they are being charged for and can lead to confusion and frustration. It is important for patients to have access to this information so that they can ensure they are being charged correctly and so that they can track their expenses and understand their insurance benefits.

To avoid this issue, patients can request an itemized copy of their bill, which will list out each charge and corresponding procedure. This allows patients to review the charges and compare them to their health insurance plan to ensure they are being charged correctly. Additionally, patients can refer to the Explanation of Benefits (EOB) report from their insurance company, which provides details about the services performed, the associated charges, and how the charges are processed by the insurance company. The EOB can help patients understand what is covered by their insurance and what they are responsible for paying out-of-pocket.

It is also important for patients to keep detailed records of any communication with their insurance company or medical provider regarding their bills. This includes recording the dates of conversations, the names of the individuals they spoke with, and a summary of what was discussed. This information can be helpful if there are any disputes or discrepancies regarding the bill.

Furthermore, patients have the right to appeal a claim denial and can seek assistance from their insurance agent, HR department, or a medical advocacy agency if needed. They can also contact their state's insurance department for help with insurance-related issues. By taking these proactive steps, patients can better understand their medical bills and protect themselves from incorrect or excessive charges.

Instant Answer Term Insurance: Unraveling the Mystery of Speedy Coverage

You may want to see also

Explore related products

![]()

Insurers may not pay anything despite applying a discount

In some cases, insurers may apply a discount to the billed price but not pay anything at all towards the claim. This can happen when the insurance company determines that the claim is not covered by the policy, or there are specific exclusions or limitations in the policy that apply to the particular service or treatment. It is essential for policyholders to carefully review their insurance policies to understand what is and isn't covered.

Additionally, there may be instances where the insurance company suspects fraud or deems that the claim amount is inflated. In such cases, the insurer may deny the claim or offer a lower settlement amount. Policyholders should keep detailed records of their interactions with the insurer and the medical provider to protect themselves in case of disputes.

Furthermore, delays in claim payments are also common, and this can result in prolonged periods where the policyholder has to bear the financial burden. Issues with claim handling are the most common source of complaints against insurance companies, as per the National Association of Insurance Commissioners (NAIC).

Moreover, insurance policies often have deductibles, co-pays, and co-insurance requirements. In these cases, even if a discount is applied by the insurer, the policyholder may still have to pay the full amount of these out-of-pocket expenses, at least initially. It is important to understand the structure of your insurance policy, including any applicable deductibles and coverage limits, to avoid surprises when it comes to paying for medical services.

Lastly, in certain situations, the insurance company may apply a discount to the billed amount but not actually contribute any payment. This can occur when the insurance company processes the claim but determines that the policyholder is responsible for the entire amount due to specific policy terms or limitations. This situation can be confusing for policyholders, especially when the explanation of benefits (EOB) provided by the insurer is unclear or misleading.

The Ethical and Legal Conundrum of Billing Insurance: Exploring the Grey Areas

You may want to see also

Frequently asked questions

A contracted discount, also known as a contractual adjustment, is a term used in health insurance billing when an insured person is covered by an individual or group health plan that involves a network of providers contracted by the insurer. It generally refers to a reduction in the amount charged for a service, lowering the amount owed on a claim.

Insurance companies negotiate with healthcare providers to set discounted rates for certain services. This benefits the insurance company as it can pay less for services, and it benefits the providers as they gain broader access to members and are guaranteed a significant portion of their fee.

When a healthcare provider agrees to accept an insurance plan, they agree to a set rate for certain procedures. This rate is often lower than the standard rate charged to uninsured patients. The difference between the standard rate and the contracted rate is the contracted discount.

Services covered by your insurance plan and provided by a network provider will typically be eligible for a contracted discount. You can refer to your insurance plan details to see what services are covered and check with your insurance provider to confirm if a specific service is eligible for a discount.

On your bill or explanation of benefits (EOB) statement, look for a section called "Plan Discounts" or "Contractual Adjustments". This section will show the difference between the standard rate and the contracted rate, indicating the amount of the discount.