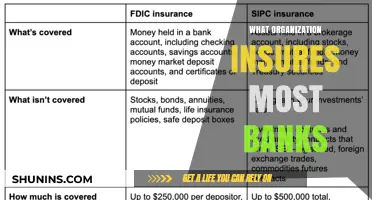

The Federal Deposit Insurance Corporation (FDIC) is a government agency that insures deposits at banks. Established in 1933 during the Great Depression, the FDIC was created to restore public confidence in the banking system by providing insurance for deposits made at banks and savings associations. The FDIC collects fees, known as insurance premiums, from banks and uses these funds to insure depositors' money up to a certain limit. This limit currently stands at $250,000 per account, and the FDIC's role in insuring deposits has helped reduce the occurrence of bank runs.

| Characteristics | Values |

|---|---|

| Name of the institution | Federal Deposit Insurance Corporation (FDIC) |

| Year of establishment | 1933 |

| Maximum insured amount per account | $250,000 |

| Maximum insured amount for beneficiaries | $1,250,000 |

| Types of accounts insured | Checking, savings, money market accounts, and certificates of deposit (CDs) |

| Types of accounts not insured | Investment products like stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities |

| Types of accounts insured for beneficiaries | Living or family trust accounts |

| Types of accounts not insured for beneficiaries | In-laws, cousins, and charities |

| Funding | Insurance premiums paid by banks and interest earned on the Deposit Insurance Fund |

Explore related products

What You'll Learn

![]()

The Federal Deposit Insurance Corporation (FDIC)

The FDIC is funded by insurance premiums paid by banks and from interest earned on the FDIC’s Deposit Insurance Fund, which is invested in US government obligations. The banks’ premiums depend on the size of the bank and bank regulators’ assessment of the riskiness of the bank. The FDIC insurance limit was initially US$2,500 per ownership category, and this has been increased several times over the years to accommodate inflation. Since the enactment of the Dodd–Frank Wall Street Reform and Consumer Protection Act in 2010, the FDIC insures deposits in member banks up to $250,000 per ownership category, i.e., per depositor, per insured bank, and for each account ownership category.

The FDIC also answers questions about federal deposit insurance coverage and handles complaints and inquiries about FDIC-insured state banks that are not members of the Federal Reserve System. The FDIC as a receiver is tasked with protecting the depositors and maximizing the recoveries for the creditors of a failed institution. The FDIC acting in its corporate role as a deposit insurer is legally separate from the FDIC acting as a receiver.

The FDIC has also been responsible for resolving failed thrifts since the Resolution Trust Corporation (RTC) was merged into the FDIC in 1995.

Depression Screening: CPT Code for Private Insurance Claims

You may want to see also

Explore related products

![]()

Deposit insurance covers up to $250,000 per account

Deposit insurance, provided by the Federal Deposit Insurance Corporation (FDIC), covers up to $250,000 per account. This limit applies to each depositor per insured bank and ownership category. The FDIC was established in 1933 during the Great Depression to restore public confidence in the banking system by insuring deposits. The FDIC collects insurance premiums from banks and is overseen by a five-member board.

The $250,000 limit applies to various account types, including savings, checking, and certificates of deposit (CDs). Single accounts with one owner and no beneficiaries are insured up to $250,000 per bank. Joint accounts provide $250,000 in coverage per owner, while retirement accounts like IRAs receive their own $250,000 in coverage, separate from other accounts. Business accounts are also covered up to $250,000, independent of personal accounts held at the same bank.

If a depositor has multiple accounts at the same bank, the FDIC will aggregate the balances and insure the total up to $250,000. For example, if a person has three savings accounts at the same bank, each with $100,000, the FDIC would insure a total of $250,000 across all three accounts. To insure larger deposits, individuals can open accounts at multiple institutions or use deposit networks that spread funds across multiple banks.

It's important to note that FDIC insurance does not cover investment products like stocks, bonds, mutual funds, or cryptocurrencies, even if purchased through an insured bank. The FDIC also does not insure the contents of safe deposit boxes, life insurance policies, annuities, or municipal securities.

Barclays Bank Delaware: Is Your Money Safe?

You may want to see also

Explore related products

![]()

FDIC is funded by insurance premiums paid by banks

The Federal Deposit Insurance Corporation (FDIC) was established in 1933 during the Great Depression to restore public confidence in the banking system. It provides insurance for deposits made at banks and savings associations. The FDIC is an independent agency of the federal government that receives no Congressional appropriations. Instead, it is funded by insurance premiums paid by banks and savings associations for deposit insurance coverage. The FDIC insures deposits in U.S. banks and thrifts, covering virtually every bank and savings association in the country. The standard insurance amount is $250,000 per depositor, per insured bank, for each account ownership category. This limit was raised from $100,000 to $250,000 in 2008 and made permanent in 2010.

The FDIC generates its income from premiums that banks pay for deposit insurance. The amount of the premium depends on the size of the bank and the bank regulators' assessment of the riskiness of the bank. The FDIC has the authority to raise premiums as needed and to develop a system of risk-based deposit insurance premiums. In addition to premiums, the FDIC also earns interest on its Deposit Insurance Fund, which is invested in U.S. government obligations. As of December 31, 2022, the Deposit Insurance Fund had $128.2 billion, or about 1.27% of all insured deposits. The FDIC is working to increase this ratio to meet its target of 2% of insured deposits over the long run.

The FDIC plays a crucial role in maintaining stability and public confidence in the nation's financial system. It directly supervises and examines over 5,000 banks and savings associations for operational safety and soundness. The FDIC also examines banks for compliance with consumer protection laws and the Community Reinvestment Act. When a bank fails, the FDIC responds immediately to protect insured depositors. The FDIC has several options for resolving institution failures, including selling the bank to a willing buyer or paying off insured deposits and liquidating the failed bank's assets. Since the start of FDIC insurance in 1934, no depositor has lost any insured funds due to a bank failure.

Single Payer Insurance: Private Insurance's End?

You may want to see also

Explore related products

![]()

Foreign deposits are not insured

The Federal Deposit Insurance Corporation (FDIC) was established in 1933 during the Great Depression to restore public confidence in the banking system by providing insurance for deposits made at banks and savings associations. The FDIC is a government agency that collects fees, or insurance premiums, from banks. The FDIC insures deposits up to a limit of $250,000 per depositor, per insured bank, and for each account ownership category.

However, foreign deposits, or deposits made at domestic banks outside the United States, are not insured by the FDIC and are thus not subject to deposit insurance premiums. This means that if you make a deposit in a foreign branch of a U.S. bank, your deposit is not subject to the same protection as it would be if made in a U.S. branch. In many cases, foreign deposits are only payable in the country in which the deposit was made.

There are some exceptions to this rule. Deposits in an insured branch of a foreign bank that are payable by contract in the U.S. are entitled to FDIC insurance coverage. Additionally, the FDIC clarified that foreign depositors who make deposits in bank branches on U.S. soil enjoy federal deposit insurance. All deposits made to U.S. bank branches located in the U.S. are treated equally, regardless of whether the depositor is a foreign national.

It is important to note that the availability of deposit insurance is not limited to citizens and residents of the United States. Any person or entity that maintains deposits in an IDI (unless the branch is located outside the United States) is eligible for deposit insurance coverage.

Insurance Forms: Private Practice Essentials

You may want to see also

Explore related products

![]()

FDIC deposit insurance is automatic

The Federal Deposit Insurance Corporation (FDIC) is an independent agency created by Congress to maintain stability and public confidence in the nation's financial system. FDIC deposit insurance is automatic when you open a deposit account at an FDIC-insured bank. This insurance covers deposits in all types of accounts at FDIC-insured banks, including savings, checking, and certificates of deposit (CDs). FDIC deposit insurance covers up to $250,000 per depositor, per FDIC-insured bank, for each account ownership category. This limit was raised from $100,000 to $250,000 in 2008 and made permanent in 2010.

If you have a single ownership account at an FDIC-insured bank and a joint ownership account at the same bank, you will be insured for up to $250,000 for your single ownership account deposits and separately for your ownership interest up to $250,000 for your joint ownership account deposits. Similarly, if you have a single ownership account in one FDIC-insured bank and another single ownership account in a different FDIC-insured bank, you will be insured for up to $250,000 for your single account deposits at each bank.

The FDIC provides tools and resources to help consumers understand and calculate their deposit insurance coverage, such as the Electronic Deposit Insurance Estimator (EDIE) available on their website. Since its founding in 1933, the FDIC has ensured that no depositor loses their insured funds, fostering trust and confidence in the banking system.

Bank of New York: Insurance Services and Solutions

You may want to see also

Frequently asked questions

The Federal Deposit Insurance Corporation (FDIC) insures deposits at banks.

The FDIC insures up to $250,000 per depositor, per FDIC-insured bank, per ownership category.

The FDIC covers checking, savings, money market accounts, and certificates of deposit (CDs).

You can ask a bank representative, look for the FDIC sign at your bank, or use the FDIC's BankFind tool.