Life insurance is an important component of a financial plan, but it is also a difficult and uncomfortable topic to discuss. Financial advisors may push life insurance policies because they receive higher commission payments for these policies. In some cases, advisors may prioritize their own financial gain over their clients' best interests. It is important to be cautious and do your own research before purchasing any financial product, including life insurance. Seeking advice from a fee-only financial planner who does not sell insurance can help ensure that you receive unbiased recommendations.

| Characteristics | Values |

|---|---|

| Financial advisors push life insurance because they get a bigger commission payment on these policies | Whole life insurance policies have expensive fees |

| Financial advisors are salespeople who operate on the suitability standard | The profit margins for insurance are better than for standard investments |

| Financial advisors are not fiduciaries | A fiduciary is legally required to act in the client's best interest |

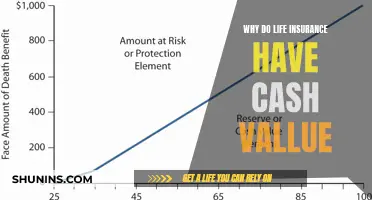

| Whole life insurance is a combined insurance and investment product |

Explore related products

What You'll Learn

- Financial advisors push life insurance because it's a lucrative industry with high profit margins

- They earn higher commissions from whole life policies

- They are incentivised to sell insurance products as investments

- It's an uncomfortable topic for clients, so they may not seek it out themselves

- It's a critical component of a financial plan, so advisors may genuinely believe it's in a client's best interest

![]()

Financial advisors push life insurance because it's a lucrative industry with high profit margins

Financial advisors push life insurance because it is a lucrative industry with high-profit margins. Life insurance is often viewed as a boring and uncomfortable topic to discuss, but it is a critical component of financial planning. People generally do not like talking about life insurance because it reminds them of their mortality and involves spending money without seeing any direct benefits.

Financial advisors, on the other hand, are incentivized to sell life insurance due to the high commissions they can earn. Whole life insurance policies, in particular, tend to result in larger commission payments for advisors, which may explain why they are often pushed onto clients even when it may not be the best option for the client's needs. The profit margins in the life insurance industry are significantly better than those in standard investments, making it an attractive prospect for financial advisors.

It is important to recognize that not all financial advisors operate solely with their financial interests in mind. Fee-only financial planners, for example, charge a flat fee for their services and do not sell insurance, providing advice that is not influenced by potential commissions. However, fee-based financial advisors may end up taking a significant portion of investment profits in the form of fees, which can sometimes amount to as much as 33%.

When considering life insurance, it is recommended to seek advice from a trusted source, such as a fiduciary advisor, and to be cautious of advisors who are overly pushy about specific products. It is also generally advised to keep insurance and investments separate, opting for term life insurance instead of whole life insurance, as the latter often carries expensive fees.

Borrowing Against AFBA Life Insurance: Is It Possible?

You may want to see also

Explore related products

$6.97 $19.97

![]()

They earn higher commissions from whole life policies

Financial advisors push life insurance because they earn higher commissions from whole life policies. While whole life insurance policies can be beneficial in some cases, financial advisors may prioritize their own financial gain over their clients' best interests by recommending these policies. This conflict of interest can result in clients being steered towards unnecessary or unsuitable products.

Whole life insurance policies are often promoted by financial advisors because they offer higher commissions than other types of insurance or investment products. Commissions are a significant source of income for financial advisors, and the potential for higher earnings can influence the products they recommend to their clients. In some cases, financial advisors may even be incentivized or pressured by their companies to prioritize the sale of certain products, such as whole life insurance, over others. This creates a conflict of interest where the advisor's recommendations may not always align with the client's best interests.

The profit margins on whole life insurance policies are significantly higher than those on traditional investments. As a result, financial advisors may be motivated to sell these policies to maximize their earnings, regardless of whether it is the most suitable option for their clients. This practice can lead to unethical behavior, as advisors may prioritize their own financial gain over providing unbiased advice and suitable recommendations.

Furthermore, whole life insurance policies often come with expensive fees and conservative investment portfolios, which can reduce the overall profitability of the investment for the client. While financial advisors may benefit from the higher commissions, clients may find that their investment profits are significantly reduced due to the fees associated with these policies. Therefore, it is essential for individuals to carefully consider their options and seek advice from multiple sources before committing to any financial product, especially those that are heavily pushed by advisors.

To avoid falling prey to biased advice, individuals should consider seeking advice from fee-only financial planners who do not sell insurance. By paying a flat fee for advice, individuals can ensure that the recommendations they receive are not influenced by potential commissions or other financial incentives. Additionally, it is important to remember that insurance and investments are usually best kept separate, and that term life insurance is often a more cost-effective and suitable option for most individuals.

Renewing Health Insurance: Lifetime Coverage Options

You may want to see also

Explore related products

![]()

They are incentivised to sell insurance products as investments

Financial advisors may push life insurance because they are incentivised to sell insurance products as investments. Life insurance, particularly whole life insurance, is often pitched as an investment opportunity by financial advisors. This is because they can earn higher commissions from selling these policies compared to other investment products.

Whole life insurance policies are a combined insurance and investment product, and financial advisors are incentivised to sell them because they can earn larger commissions. These commissions can sometimes amount to a significant proportion of the profits made on the investment. For example, a fee of 1.5% or 2% for fee-based financial advisors can end up taking up to 33% of investment profits. Thus, financial advisors may be motivated to recommend whole life insurance policies to their clients to increase their earnings.

Additionally, some financial advisors may be employed by companies that earn money from advertisers, including financial professionals and firms that pay to be featured. This creates a conflict of interest when promoting certain products over others, as they may favour the advertisers' products regardless of whether they are suitable for the client.

Furthermore, some financial advisors work on a commission basis, meaning they earn a percentage of the sales they make. In this case, selling life insurance policies can be more profitable than selling other investment products with lower commission rates. This incentive structure can motivate advisors to push life insurance products to increase their income.

It is important to note that while financial advisors may be incentivised to sell life insurance as an investment, it may not always be in the best interest of the client. Suze Orman, a financial advisor, advises against using whole life insurance as an investment vehicle. She recommends keeping investments and insurance separate and opting for term life insurance instead of whole life insurance. Orman suggests that individuals should invest through other avenues, such as retirement plans or the stock market, rather than through insurance policies.

Understanding Indexation in Life Insurance Policies: Maximizing Your Benefits

You may want to see also

Explore related products

![]()

It's an uncomfortable topic for clients, so they may not seek it out themselves

Life insurance is a critical component of a financial plan, but it is also a boring and uncomfortable topic for many people. The mere mention of life insurance is a reminder of mortality, which is a buzz kill and a conversation stopper. It also means having less money to spend each month, and the buyer will never directly benefit from the policy. Given these factors, clients may avoid seeking out life insurance policies themselves, which is why financial advisors push them.

Financial advisors are salespeople who are incentivized to sell life insurance policies because they receive higher commission payments on these policies than on other products. They are not fiduciaries, and they are not legally required to act in the client's best interest. While it is not illegal for a fiduciary to sell whole life insurance, it is uncommon, and the odds of a client recovering damages from a fiduciary for selling them whole life insurance are slim.

Fee-based financial advisors who are registered with the SEC are held to a higher standard and are a better option for those seeking unbiased financial advice. These advisors charge a flat fee for their services and do not take a significant portion of the client's profits. However, the fees for these advisors can sometimes amount to a large percentage of investment profits.

It is essential to understand that insurance and investments should be kept separate. While whole life insurance policies are pitched as investment opportunities, they often have expensive fees and are overly conservative. Term life insurance is generally a better option, as the premiums are cheaper, and most people do not need life insurance to cover them for their entire lives.

When considering life insurance, it is crucial to do your homework and buy a policy that is best for your family, not your insurance agent. Seek out a fee-based fiduciary advisor who can provide unbiased advice and help you navigate the complex world of life insurance and investments.

Beneficiary Life Insurance: Taxable or Not?

You may want to see also

Explore related products

![]()

It's a critical component of a financial plan, so advisors may genuinely believe it's in a client's best interest

Life insurance is a critical component of a financial plan, so advisors may genuinely believe it is in a client's best interest. It is a boring and uncomfortable topic to discuss, as it forces people to confront the reality of their mortality. However, it is essential to have a financial plan that includes life insurance to ensure that loved ones are provided for in the event of a tragedy.

Financial advisors may push life insurance because they believe it is necessary for their clients' financial security. They may also recommend specific types of life insurance, such as term life insurance, which is generally considered a better option than whole life insurance due to its cheaper premiums. Term life insurance provides coverage for a specified period, typically sufficient to cover most people during their primary income-earning years.

While financial advisors may have their clients' best interests at heart, it is important to remember that some advisors are incentivized by commissions on certain products. In the case of life insurance, advisors may receive higher commissions for selling whole life insurance policies, which could influence their recommendations. It is always advisable to do your research and understand the different types of life insurance before making a decision.

When considering life insurance, it is essential to seek advice from a trusted and qualified professional, such as a fee-only financial planner who does not rely on commissions from insurance sales. By finding a fiduciary advisor, you can ensure that the advice you receive is unbiased and aligned with your best interests.

Additionally, it is crucial to remember that life insurance should not be treated as an investment vehicle. While it provides essential protection, investing your money in the stock market or real estate is generally a better strategy for building wealth. Keeping your investments and insurance separate allows you to make more informed and effective decisions about your financial future.

Life Insurance for Military Members: Private Options Explored

You may want to see also

Frequently asked questions

Financial advisors push life insurance because it is a lucrative source of income for them. Life insurance policies often come with high commissions, and advisors may prioritize their own financial gain over their clients' best interests.

Term life insurance provides coverage for a specified period, whereas whole life insurance covers an individual's entire life. Term life insurance premiums are generally cheaper, and most people do not need lifelong coverage.

Whole life insurance policies offer higher commissions to advisors, incentivizing them to recommend these products to their clients. Whole life insurance also combines insurance and investment, making it a product that falls under the purview of financial advisors.

No. Financial experts like Suze Orman advise against using life insurance, especially whole life insurance, as an investment. Investment portfolios for whole life policies typically carry expensive fees and may not offer attractive returns.

When seeking a financial advisor for life insurance, it is recommended to find a fee-only financial planner who does not sell insurance. A fee-only Certified Financial Planner (CFP) professional who does not sell insurance will provide advice without the conflict of interest that arises when advisors earn commissions from insurance sales.