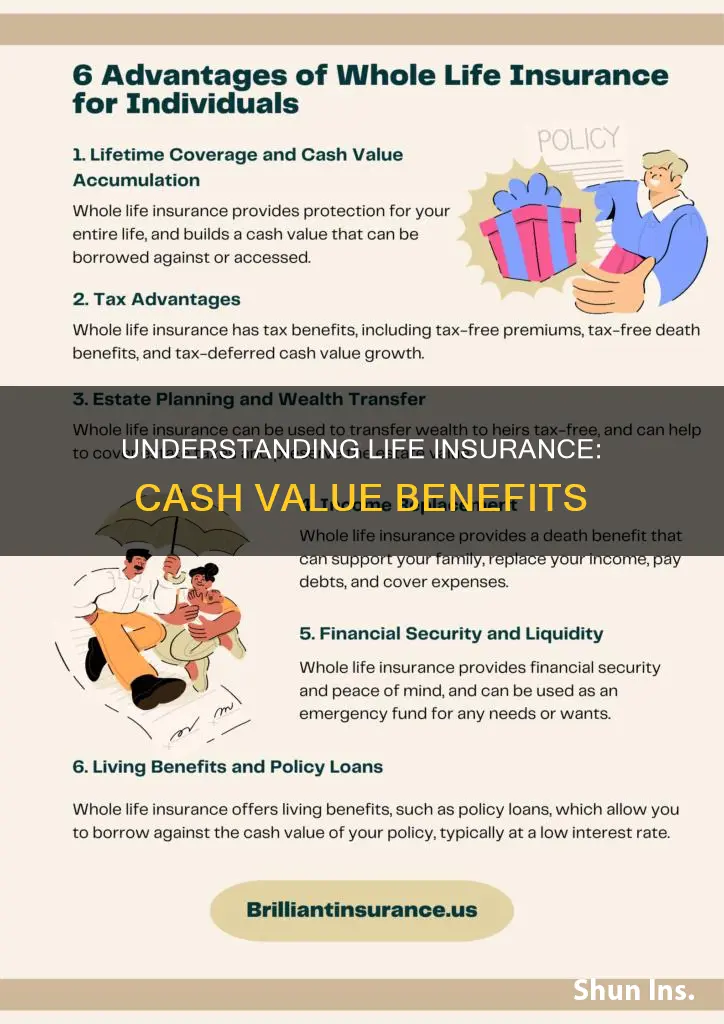

Cash value life insurance is a feature included in permanent life insurance types like whole life insurance and universal life insurance. It allows policyholders to access the cash value of their plan while they are still alive, providing a savings option and a loan mechanism. This cash value is accumulated through regular premium payments, with interest and dividends credited to the policy. The cash value feature offers flexibility, allowing funds to be withdrawn or borrowed against, although this may impact the death benefit and policy terms. It is important to understand the specific plan and insurance company's offerings, as well as the associated risks, before deciding on a cash value life insurance policy.

Explore related products

What You'll Learn

![]()

Permanent life insurance types with cash value

Permanent life insurance policies provide coverage for the entirety of the policyholder's life, as opposed to term insurance, which only provides coverage for a specified period. Permanent life insurance policies also build cash value over time, which can be used to borrow against, withdrawn, or used to pay premiums.

Whole life insurance is a type of permanent life insurance that offers lifelong coverage and builds cash value in a secure account. It is one of the most popular choices in the life insurance market due to its high-growth potential and competitive rates. Whole life insurance policies grow their cash value via a fixed interest rate.

Universal life insurance is another type of permanent life insurance that offers flexible premium payments, allowing you to scale the death benefit up or down depending on your circumstances. The cash value of universal life insurance can be used to pay for premiums or other expenses.

Variable universal life insurance offers flexible premiums and a savings component, with the savings portion, or cash value, growing based on the investment methods chosen. This type of plan involves more risk, as the cash value will fluctuate based on the performance of the chosen investments.

Indexed universal life insurance is a type of permanent life insurance where the cash value grows based on a chosen stock market index. Premiums can vary within a certain range, and cash value growth is tied to the performance of a broad market index, such as the S&P 500, with minimum and maximum caps to limit investment risk.

Navigating Life Insurance: Making Changes to Your Policy

You may want to see also

Explore related products

$2.99 $13.95

$11.25 $15.95

![]()

Borrowing against cash value

Borrowing against the cash value of a life insurance policy can be a quick and easy way to get cash in hand when you need it. However, there are a few things to consider before borrowing.

Firstly, it's important to understand that only permanent life insurance policies, such as whole life and universal life, have a cash value component that can be borrowed against. Term life insurance policies, on the other hand, generally do not have a cash value and, therefore, cannot be borrowed against.

When you borrow against a life insurance policy with cash value, the loan is taken out directly with the life insurance company, and the value of the policy is used to guarantee the loan's repayment. The loan amount is typically limited to a maximum of 90% of the policy's cash value, and the insurer sets the specific limit. It's worth noting that the cash value may take several years to accrue before it is sufficient to borrow against.

One advantage of borrowing against the cash value of a life insurance policy is that it does not require collateral in the form of other assets, such as your house or car. The policy itself serves as collateral. Additionally, life insurance loans usually have flexible repayment schedules, allowing repayment at the borrower's convenience. However, it is important to ensure that the loan amount does not exceed the cash value, as this could result in a lapse in coverage.

Life insurance loans are generally tax-free and often have lower interest rates compared to personal loans or credit cards. However, it's important to consult a financial advisor to understand the tax implications specific to your situation. In the event of the policyholder's death before full repayment of the loan, the outstanding loan amount, including interest, will typically be deducted from the death benefit.

Life Insurance Riders: Applicant Flexibility and Customization

You may want to see also

Explore related products

![]()

Withdrawing from cash value

Withdrawing from the cash value of a life insurance policy is a feature of permanent life insurance types like whole life insurance and universal life insurance. Term life insurance, on the other hand, does not include a cash value component and expires after a specific number of years.

There are several ways to withdraw from the cash value of a life insurance policy. One way is to take out a loan against the policy, which is typically provided at a lower interest rate than a bank loan and does not require credit checks or affect your credit rating. Repaying the loan is usually optional, but if you choose not to, the outstanding loan balance will be deducted from the death benefit.

Another option is to withdraw funds directly from the cash value, either in a lump sum or through payments. Withdrawing money in this way is often tax-free as long as it's not more than the amount you've paid into the policy. However, it's important to note that withdrawing funds will likely result in a reduction in the death benefit, and this reduction may be greater than the amount withdrawn depending on the specific terms of the policy.

Finally, you can choose to surrender the policy altogether, which means cancelling the policy and receiving the cash value. This option should be considered a last resort, as it also results in the loss of life insurance coverage. Surrendering the policy may also incur taxes and fees, which can significantly reduce the cash value.

Heart Disease and Life Insurance: What's the Deal?

You may want to see also

Explore related products

$15.95 $15.95

![]()

Cash value and death benefits

Cash value life insurance is a feature included in permanent life insurance types like whole life insurance and universal life insurance. Term life insurance, on the other hand, does not include a cash value component. Cash value insurance policies don't expire after a specific number of years, unlike term life insurance.

The cash value feature is a significant selling point for permanent life insurance policies. Policyholders can borrow against the cash value, make partial withdrawals, or withdraw all the cash value and surrender the policy. However, it's important to note that outstanding loan amounts and withdrawals will reduce the death benefit, and withdrawing all the cash value will terminate the policy.

The cash value of life insurance can be used in different ways, depending on the type of policy. For example, with whole life insurance, the cash value grows through a fixed interest rate, while universal life policies' cash value growth is more dependent on the market but with a guaranteed minimum rate. Universal life insurance also allows the policyholder to adjust the value of premium payments and the death benefit. Variable life insurance provides greater access to investment tools, but the cash value fluctuates with the performance of those investments.

The cash value in permanent life insurance policies can generate substantial returns, but it also carries risks. It provides a mechanism for policyholders to accumulate funds and can be used as a savings option or to pay policy premiums. However, it's important to consider the potential impact on the death benefit when accessing the cash value.

Life Insurance: Investing in Peace of Mind

You may want to see also

Explore related products

![]()

Cash value as a savings option

Cash value life insurance is a savings option that allows policyholders to accumulate funds for future use. It is a feature included in permanent life insurance types like whole life insurance, universal life insurance, and variable life insurance. These policies do not expire after a specific number of years, unlike term life insurance, which provides coverage for a fixed period.

The cash value component of life insurance enables policyholders to build a nest egg over several decades. This can be particularly advantageous for those seeking long-term savings options alongside retirement plans such as an IRA or 401(k). The cash value in permanent life insurance policies can generate impressive returns, but it also carries certain risks.

One of the key advantages of cash value life insurance is the ability to access the funds while the policyholder is still alive. This can be done through partial withdrawals, loans, or by selling back the policy to the insurer. However, it is important to note that making withdrawals or borrowing against the cash value will typically reduce the death benefit. Additionally, withdrawing the entire cash value and surrendering the policy may result in termination of coverage and potential surrender fees.

The cash value in life insurance policies earns interest over time, and the taxes on the accumulated earnings are deferred. The growth of the cash value varies by policy type. Whole life policies, for example, grow their cash value through a fixed interest rate, while universal life policies are more dependent on market performance, albeit with a guaranteed minimum rate. Variable life insurance policies involve more risk, as the cash value fluctuates based on the performance of chosen investments.

Overall, cash value life insurance provides policyholders with a savings option that can be utilised during their lifetime. It offers flexibility in accessing funds, but it is important to carefully consider the potential impact on the death benefit and consult with financial professionals before making any decisions.

Life Insurance Apps: Why So Many Screens?

You may want to see also