The Mitsubishi Mirage is a budget-friendly car with a base price of $14,325 for the 2022 model. However, insurance rates for the Mirage are notably high compared to other vehicles in its class, with some owners reporting insurance premiums of up to $1000 per year. Various factors contribute to the high insurance costs, including the car's safety profile, repair costs, location, and driver demographics. While the 2024 Mirage has a 4-star crash-test rating, its lightweight construction may result in higher repair costs and increased risk of injury in collisions. Additionally, insurance companies consider the demographics of typical Mirage owners, who may be newer drivers or younger drivers with higher crash risks, leading to elevated insurance rates. Location-specific factors, such as crime rates and natural disasters, can also impact insurance premiums. Ultimately, insurance companies assess a multitude of variables to determine rates, and shopping around for quotes can help Mirage owners find more affordable coverage options.

| Characteristics | Values |

|---|---|

| Repair costs | High |

| Risk assessment | High |

| Natural disasters | Floods, fires |

| Mitsubishi's market presence | No longer sells new cars in the UK |

| Insurance company | Lemonade offers rates from $48 to $67 a month |

| Insurance type | Liability insurance is cheaper than full coverage |

| Driving record | Accidents and speeding tickets increase rates |

| Location | Insurance rates vary by state |

Explore related products

What You'll Learn

![]()

Repair costs

The safety rating of a vehicle also plays a crucial role in insurance costs. A car with a lower safety rating may be deemed more likely to sustain severe damage in an accident, resulting in higher repair costs for insurance companies. The Mirage, being a smaller and more compact car, may fall into this category. Additionally, advanced technology features in modern vehicles can increase repair or replacement costs, further impacting insurance premiums.

The age and model year of a Mirage can also influence repair costs. Older models may have cheaper parts and labour costs compared to newer models, which often feature more advanced technology. However, as Mitsubishi no longer operates in certain regions, such as the UK, sourcing parts for repairs may be more challenging and expensive, regardless of the model year.

It is worth noting that insurance companies also consider the risk of writing off a vehicle when calculating premiums. In the case of the Mirage, some insurance agents have stated that even a minor accident could result in the car being written off, whereas a larger vehicle might only require a bumper replacement. This write-off risk is likely to be influenced by the perceived value of the vehicle and the potential for more extensive damage in an accident.

Furthermore, economic factors, such as the rising cost of living, can contribute to increasing repair costs. As a result, insurance companies may need to adjust their premiums to recoup costs, especially in the context of natural disasters, fires, and floods, which have become more frequent. These factors collectively contribute to the potentially higher insurance premiums associated with the Mitsubishi Mirage.

Georgia's Written Cancellation Clause: Auto Insurance and the Fine Print

You may want to see also

Explore related products

![]()

Risk assessment

One of the key considerations in risk assessment is the cost of repairs. If a car is deemed expensive to fix in the event of damage, insurance providers will often set higher premiums to mitigate the potential costs of repairs. This appears to be a significant factor in the case of the Mitsubishi Mirage, with some insurance companies citing the high cost of repairs as a reason for increased premiums. This is despite some owners reporting that they have not experienced significant repair issues with their Mirages.

The safety profile of a vehicle is another crucial factor in risk assessment. A car with a higher likelihood of causing serious injuries or fatalities in crashes will generally be more expensive to insure. The Mitsubishi Mirage has a four-star crash-test rating from the National Highway Traffic Safety Administration, indicating that it may pose a higher safety risk than some other vehicles on the road. This could contribute to higher insurance rates.

Additionally, insurance companies often consider the demographics of typical owners of a particular car model. If a car is more likely to be driven by younger or less experienced drivers, who statistically have a higher risk of accidents, insurance rates may be adjusted accordingly. The Mitsubishi Mirage, being a budget-friendly option, may attract a younger demographic, which could influence the risk assessment and result in higher premiums.

It is worth noting that insurance rates can vary significantly between different insurance companies and locations. External factors, such as natural disasters or economic conditions, can also impact insurance rates across the board. Therefore, it is always advisable for consumers to shop around and compare rates from multiple providers before making a decision.

High School Ring Insurance: What's Covered?

You may want to see also

Explore related products

![Mirage (Special Edition) [Blu-ray]](https://m.media-amazon.com/images/I/81AI9NxjHLL._AC_UY218_.jpg)

![]()

Safety ratings

The Mitsubishi Mirage has received a range of safety ratings from different organizations. The Insurance Institute for Highway Safety (IIHS) gave the Mirage ratings of Good, Good, Good, Acceptable (side crash), and Marginal (in the small overlap front driver-side crash test). The IIHS ratings range from Poor to Good, with Good being the top grade. The National Highway Traffic Safety Administration (NHTSA) gave the Mirage an overall safety rating of 4 out of 5 stars. The NHTSA ratings are based on specific categories, such as the Front Driver Side, Front Passenger Side, Combined Side Barrier, and Pole Ratings for the Front and Rear Seats. The Side Barrier is one of the Mirage's strongest aspects, receiving 5 stars. The Mirage also received 4 stars in the rollover star rating test, which assesses the risk of rollover in a single-vehicle, loss-of-control scenario.

The safety ratings of a vehicle can impact the cost of auto insurance. A higher safety rating can lead to lower premiums as it indicates a lower risk of injury or damage. On the other hand, advanced tech features can increase premiums because they are more costly to repair or replace if damaged. The cost of insurance for the Mirage may also be influenced by other factors, such as the high cost of parts, body shop prices, and labour rates. Additionally, insurance companies may consider the demographics of Mirage owners, as the vehicle is often bought by people living in impoverished areas, which can contribute to higher insurance rates.

Roadside Assistance Auto Insurance: What You Need to Know

You may want to see also

Explore related products

![Universal Hollywood Icons Collection: Gregory Peck (Arabesque / Mirage / Captain Newman, M.D. / The World in His Arms) [DVD]](https://m.media-amazon.com/images/I/91XDTEVPjFL._AC_UY218_.jpg)

![]()

Location

State and Local Regulations: Different states and localities have different regulations and requirements for car insurance. Some states may have higher minimum coverage requirements, which can drive up the cost of insurance. Additionally, insurance regulations can vary, and some states may have more consumer-friendly policies that result in lower rates.

Population Density and Traffic: Living in a densely populated urban area, such as downtown Minneapolis, can result in higher insurance rates compared to rural areas with lighter traffic. Urban areas often have higher rates of accidents, theft, and vandalism, which can increase the likelihood of insurance claims.

Natural Disasters: In some regions, natural disasters such as fires, floods, and hurricanes can impact insurance rates. Insurers may need to recoup costs for payouts related to these disasters, which can result in higher premiums for all policyholders.

Crime Rates: Areas with high crime rates, including car theft and vandalism, can lead to increased insurance rates. Insurance companies may consider these areas as higher-risk and, therefore, charge higher premiums.

Insurance Company Presence: The availability and competition among insurance companies in a particular region can also affect rates. In some states, certain insurance companies may offer more competitive rates due to their larger market share or specific underwriting guidelines.

Economic Factors: The local and state economy can influence insurance rates. In some cases, economic factors, such as unemployment rates or the cost of living, may impact insurance pricing. Additionally, insurance companies may adjust their rates based on the local cost of repairs, labour rates, and the price of replacement parts for the Mirage in a specific region.

Billing Auto Insurance: What Can You Claim?

You may want to see also

Explore related products

![]()

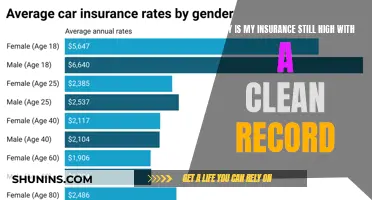

Driver profile

The cost of car insurance is influenced by a variety of factors, including the driver's profile. The driver's profile encompasses various factors such as age, gender, marital status, driving history, and location. Let's take a closer look at how these factors can impact the insurance cost for a Mitsubishi Mirage:

Age:

Age is a significant factor in determining insurance rates, especially for younger drivers. Insurance companies consider teenage drivers to be high-risk, resulting in higher insurance premiums. For instance, the average annual cost of full-coverage insurance for a 16-year-old driver of a Mitsubishi Mirage is $7,607, while it decreases to $6,315 for an 18-year-old driver. On the other hand, older drivers with more experience on the road may benefit from lower insurance rates.

Gender:

Insurance companies also consider gender when calculating insurance premiums. While the practice of gender-based pricing has been challenged and banned in some places, it still exists in others. In certain regions, women may find themselves paying higher insurance rates for the Mitsubishi Mirage due to assumptions about their driving skills or accident risk.

Marital Status:

Marital status can also impact insurance rates. Married individuals are often considered more stable and responsible, resulting in lower insurance premiums. For example, a 40-year-old married male driver with a clean driving record can expect to pay around $2,008 per year for insurance on a 2024 Mitsubishi Mirage.

Driving History:

A driver's history, including accidents, violations, and claims, plays a crucial role in determining insurance rates. Insurance companies view drivers with a history of accidents or violations as higher risks, leading to increased premiums. Conversely, maintaining a clean driving record can help lower insurance costs.

Location:

Location is another critical factor in insurance pricing. Insurance rates can vary significantly depending on the state, city, or even ZIP code. Factors such as population density and crime rates can influence the insurance rates for a Mitsubishi Mirage in a particular location. For example, insurance in crowded downtown areas or states with high repair costs may be more expensive.

While the driver's profile is a significant factor in determining insurance rates, it's important to remember that insurance companies consider various other factors as well, such as the car's make, model, year, and safety features. Additionally, shopping around and comparing quotes from different insurance providers can help drivers find the most affordable rates for their Mitsubishi Mirage insurance.

Full Coverage Auto Insurance in Georgia: What's Included?

You may want to see also

Frequently asked questions

There are several factors that could contribute to high insurance costs for a Mirage. Firstly, insurance companies consider the cost of repairs when calculating premiums, and some users have suggested that Mitsubishi cars may be expensive to fix. Additionally, insurance rates can vary depending on the driver's age, location, driving record, and other factors. It's worth noting that insurance rates can differ significantly between companies, so shopping around for the best rate is recommended.

According to some sources, the Mitsubishi Mirage insurance rates are around average compared to other vehicles. However, others have noted that the insurance for a Mirage can be significantly higher than that of other cars, such as the Kia Rio, even though the Mirage has a lower purchase price.

There are a few strategies you can employ to lower your insurance premiums. Firstly, consider the insurance company and shop around for quotes to find the most competitive rates. Additionally, insurance companies may offer discounts for safety features, good driving records, and bundling policies. Maintaining a clean driving record and taking advantage of available discounts can help keep your insurance costs down.