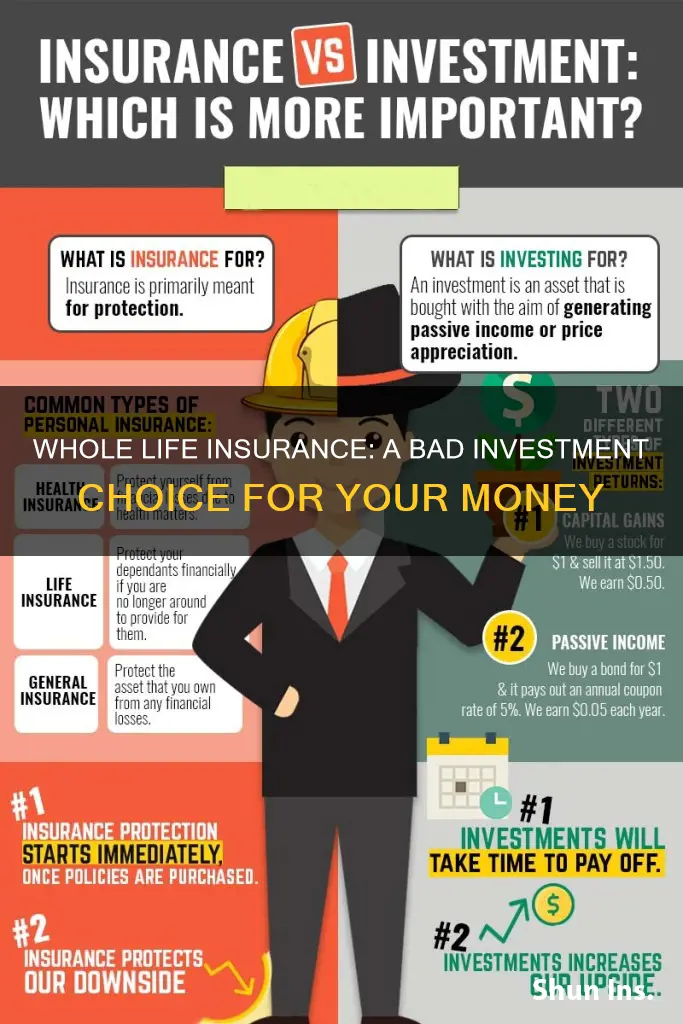

Whole life insurance is a type of permanent life insurance that offers coverage and accumulates a cash value over time. While it has its advantages, it may not be the best investment option for most people. The cost of whole life insurance is typically much higher than term life insurance, with low rates of return that may not offset the high premiums. Whole life insurance offers a fixed rate of return, which may result in lower returns compared to other investments such as stocks, bonds, and real estate. Additionally, the cash value component can be slow to grow, and the money is locked away, making it challenging to withdraw. For individuals with a high risk tolerance or those seeking control over their investments, whole life insurance may not be the ideal choice.

Explore related products

What You'll Learn

![]()

Whole life insurance is more expensive than term life insurance

For example, a healthy 40-year-old man can expect to pay an average annual premium of $6,408 for a $500,000 whole life insurance policy, while a woman of the same age might pay $5,654. In contrast, a term life policy for a healthy 40-year-old would cost $334 for a man and $282 for a woman, on average. The high premiums of whole life insurance may not be worth it if you only need life insurance coverage for a specific length of time, such as 10, 20, or 30 years. In such cases, a term life insurance policy is a better choice for pure life insurance at a good price.

Moreover, the interest and dividends earned with a whole life policy can be lower than the returns from other investments. The average annual rate of return on the cash value for whole life insurance is 1% to 3.5%, and you may earn higher returns with other investments. If you are a seasoned investor, you may not like the idea of relying on your insurer's investment managers to deliver returns for you.

Whole life insurance is a long-term investment that may be suitable for those who want a safe and guaranteed way to build cash value with a low-risk profile. It can be a powerful and highly customized asset that provides tax advantages, financial protection, and numerous guarantees and benefits. However, it is important to consider the high cost of whole life insurance compared to term life insurance and evaluate whether the benefits outweigh the expense.

Human Life Value Approach: Maximizing Life Insurance Benefits

You may want to see also

Explore related products

![Short Term 12 [Blu-ray]](https://m.media-amazon.com/images/I/71Lb114AFoL._AC_UY218_.jpg)

![]()

It offers a low rate of return on investment

Whole life insurance is a type of permanent life insurance that provides coverage for your entire lifetime, as long as you continue paying your premiums. It offers a cash value component that grows at a guaranteed rate of return, but the rate of return is often low compared to other investments.

The average annual rate of return on the cash value for whole life insurance is typically quoted as being between 1% to 3.5%. This is a relatively low rate of return compared to other investments such as stocks, bonds, mutual funds, and real estate. The cash value in a whole life insurance policy grows slowly over time and is not designed to compete with traditional investments in terms of returns. Instead, its primary benefit is the lifelong coverage and security it provides.

While whole life insurance offers guaranteed returns, these returns may not always be positive or quick. The cash value can take several years to grow, and if you withdraw money or take out a policy loan, it will reduce the death benefit and the value available to pay insurance costs. Additionally, any interest earned on the cash value is typically taxed, further reducing the overall return.

Compared to other low-risk investments, such as a Certificate of Deposit (CD), whole life insurance may also underperform due to the added fees, insurance costs, and commissions associated with the policy. As a result, whole life insurance may not be a good investment for those seeking higher or quicker returns. It is important to consider the low rate of return and the long-term nature of whole life insurance policies when deciding if it is the right choice for your financial goals and investment strategy.

Life Insurance and Taxes: Where to File on Your Return

You may want to see also

Explore related products

![Short Term 12 [DVD] [2013] [Region 1] [US Import] [NTSC]](https://m.media-amazon.com/images/I/51jC+xMaCBL._AC_UY218_.jpg)

![End of Term [Blu-ray]](https://m.media-amazon.com/images/I/61C-da10mXL._AC_UY218_.jpg)

![End of Term [DVD]](https://m.media-amazon.com/images/I/61zb8XLHPXL._AC_UY218_.jpg)

![]()

It is not suitable for those with a high-risk tolerance

Whole life insurance is not suitable for those with a high-risk tolerance due to its low-risk and low-return nature. While it offers a guaranteed, modest return, it may not be appealing to those seeking higher returns through riskier investments.

Whole life insurance is a type of permanent life insurance that provides coverage for an individual's entire life, as opposed to term life insurance, which only covers a specified period. One of its key features is the accumulation of cash value over time, in addition to the death benefit. This cash value grows at a fixed rate, guaranteed by the insurer, and is tax-deferred, resulting in a slow but steady increase.

However, for those with a high-risk tolerance, the low rates of return may not be appealing. The average annual rate of return on the cash value is typically between 1% and 3.5%, which is significantly lower than what could be achieved through investments in stocks, bonds, or real estate. High-risk investors may prefer the potential for higher returns that come with riskier investments, even if it means accepting greater volatility and uncertainty.

Additionally, whole life insurance policies offer limited control over investment choices. The insurance company declares the dividend or interest rate, and the investments are professionally managed by the insurer. This lack of control may be unappealing to seasoned investors who prefer to make their own investment decisions and actively manage their portfolio.

Furthermore, the cash value accumulation in whole life insurance can be slow, and it may take several years of paying premiums before a significant amount of cash value is accrued. This slow growth may not align with the expectations of those with a high-risk tolerance, who often seek faster and more substantial returns.

In summary, while whole life insurance offers stability and guaranteed returns, it may not be suitable for individuals with a high-risk tolerance due to its low rates of return, limited investment control, and slow cash value accumulation. High-risk investors may prefer alternative investment options that offer the potential for higher returns, even if it means accepting a higher level of risk.

Changing Life Insurance Beneficiaries During Divorce

You may want to see also

![]()

It offers no investment choices

Whole life insurance is a type of permanent life insurance that offers coverage and accumulates a cash value over time. While it provides stable returns and guaranteed growth, it may not be suitable for those seeking investment choices and higher returns. Here are some reasons why whole life insurance offers no investment choices:

Limited Investment Options

Whole life insurance offers a fixed rate of return on the cash value, but it does not provide any investment choices. The insurance company declares the dividend or interest rate, and professionally manages the investments on behalf of the policyholders. This lack of investment discretion means that seasoned investors may find it restrictive and prefer alternative investment vehicles that offer higher potential returns.

Insulation from Market Volatility

Whole life insurance provides guaranteed and stable returns, as the cash value grows at a fixed rate set by the insurer. While this insulation from market volatility offers predictability and peace of mind, it also limits the potential for higher returns associated with market-linked investments. The modest cash value growth in whole life insurance policies may not align with the expectations of those seeking higher investment returns.

Comparison to Other Investments

The average annual rate of return on the cash value for whole life insurance is typically between 1% and 3.5%. In comparison, other investments such as stocks, bonds, and real estate have the potential to generate significantly higher returns. For individuals with a high-risk tolerance and a desire for greater control over their investments, whole life insurance may not align with their investment objectives.

Long-term Nature of the Investment

Whole life insurance is designed to be a long-term investment, and it may take several years of paying premiums to accumulate a substantial cash value. The slow growth of cash value in whole life insurance policies may not appeal to those seeking faster or more immediate investment returns. Alternative investments often provide the opportunity for more dynamic and short-term returns, catering to diverse investment horizons.

Limited Flexibility for Policyholders

Whole life insurance policies offer limited flexibility in terms of investment choices. The cash value is tied to the performance of the insurance company, and policyholders have minimal influence over the specific investment decisions made by the insurer. This lack of customization may be a drawback for individuals who prefer to actively manage their investments and make choices aligned with their personal financial goals and risk tolerance.

AXA Life Insurance: Is It Worth the Hype?

You may want to see also

![]()

It is not suitable for those who only need insurance for a specific length of time

Whole life insurance is not a suitable option for those who only need insurance for a specific length of time, for several reasons. Firstly, it is a permanent insurance policy, meaning it is designed to provide a death benefit that lasts a lifetime. As a result, the cost of whole life insurance tends to be much higher than term life insurance. For example, a healthy 40-year-old man can expect to pay an average annual premium of $6,408 for a $500,000 whole life insurance policy, while the same man would pay an average of $334 per year for a term life insurance policy.

Whole life insurance also accumulates a cash value over time, which grows slowly and can be modest. This means that it can take several years of paying premiums to begin accruing a significant amount of cash value, and the cash value may be less than the premiums paid into the contract in a given year. In contrast, term life insurance does not have a wealth-building component, so the cost can be significantly lower than whole life insurance.

Additionally, whole life insurance offers a fixed rate of return on cash value, with no investment choices. This means that individuals who are looking for a higher rate of return or want control over their investments may be better off with other investment options, such as stocks, bonds, or real estate, which can offer the potential for higher returns.

Finally, whole life insurance may not be a good choice for those who only need insurance for a specific length of time because it is a long-term investment. It is designed for individuals who are willing to play the long game and are looking for stable, predictable returns over time. If an individual only needs insurance for a short period, they may be better off with a term life insurance policy, which can provide pure life insurance at a good price for a specified amount of time.

Life Insurance Payouts: Quick Access for Beneficiaries

You may want to see also

Frequently asked questions

Whole life insurance is not a one-size-fits-all product and is not suitable for most people. It is more expensive and complex than term life insurance, with higher premiums. The cash value can be slow to grow, and you may earn higher returns with other investments.

The cash value of whole life insurance can be modest and slow to grow. It may take several years of paying premiums to accrue a significant amount of cash value. Whole life insurance also offers a fixed rate of return, with no investment choices, so you won't benefit from the potential highs of the stock market.

Term life insurance is a popular alternative to whole life insurance. It is a better choice for pure life insurance at a good price. It only lasts for a specified amount of time but can be converted to a permanent policy before expiration. Other alternatives include universal life insurance and variable universal life insurance, which offer more flexibility and the ability to choose investments.