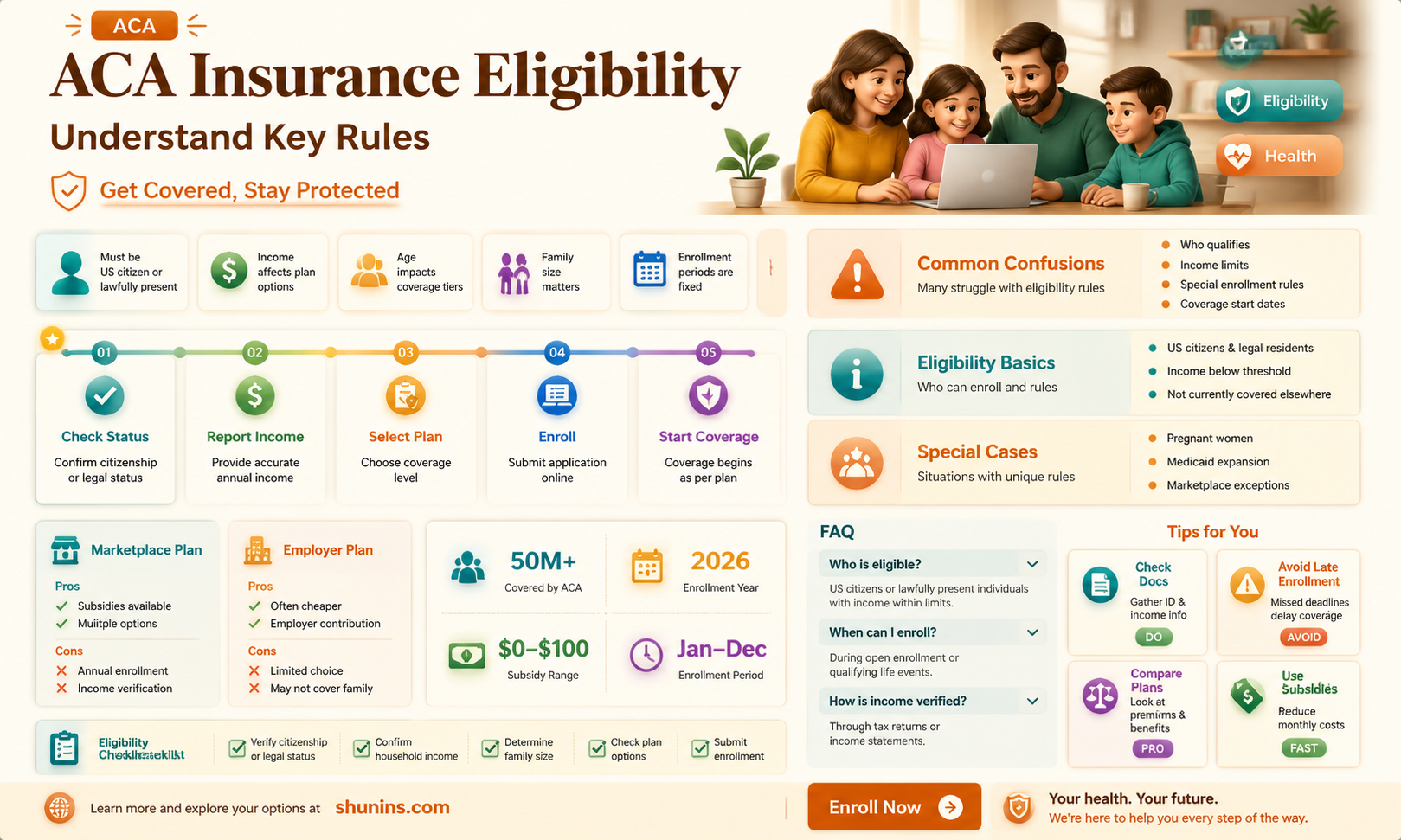

The Affordable Care Act (ACA), also known as Obamacare, is a 2010 health reform law that makes affordable insurance more widely available to everyone in the U.S., including those who do not qualify for Medicaid. Each state's Marketplace has its own enrollment instructions and eligibility requirements. To be eligible for ACA insurance, you must be a U.S. resident for tax purposes, be living in the U.S. lawfully, and not be incarcerated or covered by Medicare. Your eligibility may also depend on your income, household size, and other factors.

| Characteristics | Values |

|---|---|

| Residency | Must be a U.S. resident for tax purposes |

| Citizenship | Must be a U.S. citizen or have permanent allegiance to the U.S. |

| Incarceration Status | Must not be incarcerated |

| Medicare Coverage | Must not be covered by Medicare |

| Income | Varies based on household income and family size |

| Medical History | Medical history does not affect eligibility or premiums |

| Gender | Gender does not affect eligibility or premiums |

Explore related products

![]()

US residency

To be eligible for ACA insurance, you must be a US citizen, a US national, or be lawfully present in the US. Lawfully present immigrants can get ACA coverage and may qualify for the Premium Tax Credit, which lowers monthly insurance payments. The term “lawfully present” includes immigrants with “qualified non-citizen" immigration status, humanitarian statuses, or legal status conferred by other laws. Refugees, asylees, and victims of trafficking are also considered "lawfully present".

If you are a US citizen or a US national, you are eligible for ACA insurance. A US national is someone who is a US citizen or owes permanent allegiance to the US. In nearly all cases, non-citizen US nationals are people born in American Samoa or born abroad with one or more American Samoan parents. If you live in a US territory, you cannot get health coverage through the ACA unless you also qualify as a resident in any of the 50 states or Washington, DC.

If you are a legal US resident but not a citizen, you still have the same eligibility as citizens to receive subsidies for health insurance purchased in the exchange. Eligibility for subsidies is based on your household income. Although there is normally an upper-income threshold of 400% of the poverty level, above which premium subsidies are not available, this upper income limit was eliminated from 2021 through 2025. This means that households with income above 400% of the federal poverty level can qualify for a premium tax credit if the cost of the benchmark plan would otherwise be more than 8.5% of their household income.

If you are a recent immigrant with a household income below the federal poverty level, you may not be eligible for premium subsidies or Medicaid. However, the ACA includes a provision to assist lawfully present recent immigrants who have incomes below the poverty level. Lawmakers included a provision in the ACA that allows recent immigrants with household incomes under 100% of the poverty level to receive exchange subsidies at the level they would if their income was equal to 100% of the poverty level.

Alex Honnold: Life Insurance for a Daredevil?

You may want to see also

Explore related products

![]()

Income

To be eligible for ACA insurance, an individual's household income must meet certain criteria. For tax years 2021 and 2022, the American Rescue Plan of 2021 (ARPA) temporarily eliminated the income limit of 400% of the Federal Poverty Line (FPL) for qualifying for premium tax credits. In general, for other tax years, an individual's household income must be at least 100% and no more than 400% of the FPL for their family size to be eligible for the premium tax credit. However, there are exceptions for individuals with incomes below 100% of the FPL, such as those who are eligible for Medicaid or meet state eligibility criteria.

The amount of financial assistance provided under the ACA is based on a sliding scale, with greater subsidies available to those with lower incomes. This means that as income decreases, the amount of financial help increases, and vice versa. The savings and subsidies are calculated based on an individual's estimated income for the year in which they want health insurance coverage. It's important to note that changes in income should be reported promptly to ensure accurate savings and avoid owing money back when filing tax returns.

To determine eligibility for premium tax credits and savings, the Marketplace uses a figure called "modified adjusted gross income (MAGI)." MAGI is calculated by taking the adjusted gross income (AGI) from an individual's tax return and adding any untaxed foreign income, non-taxable Social Security benefits, and tax-exempt interest. This figure helps assess an individual's eligibility for savings and subsidies on their health insurance premiums.

In addition to income, other factors that affect eligibility for ACA insurance include citizenship or legal residency status, age, household size, and access to employer-sponsored coverage. These factors collectively determine an individual's eligibility for ACA insurance and the amount of financial assistance they may receive.

Life Insurance: A Safety Net for Disability Income Loss

You may want to see also

Explore related products

$82.51 $92.95

![]()

Family size

When considering family size, it is important to note that eligibility for ACA insurance and subsidies is determined based on the number of individuals in your household. This includes yourself, your spouse (if filing jointly), and any dependents you claim on your federal tax return. Even if some members of your household are eligible for Medicare or other government health coverage, you should still include them when calculating your family size.

The federal poverty level (FPL) guidelines play a significant role in determining eligibility for ACA insurance and subsidies. These guidelines vary based on family size, with higher income limits for larger families. For instance, the poverty level for a single adult is $15,060, while for a family of four, it is $31,200. However, it is important to note that the federal poverty level is higher in Alaska and Hawaii.

Your household income, in relation to the federal poverty level for your family size, determines your eligibility for ACA insurance and potential financial assistance. Generally, households with lower incomes will qualify for greater credit amounts and financial assistance. For example, a family of three with an income between $25,820 and $103,280 may qualify for ACA insurance and subsidies.

Additionally, life events such as moving or having a baby can impact your eligibility for ACA insurance. These events may allow you to change your coverage during a special enrollment period, even outside of the ACA's open enrollment period. Therefore, it is recommended to consider your family size and any anticipated life changes when determining your eligibility for ACA insurance.

Life Assured vs Insured: What's the Difference?

You may want to see also

Explore related products

![]()

Incarceration status

If you are incarcerated, you can use the Marketplace to apply for an Insurance program that provides free or low-cost health coverage to some low-income people, families and children, pregnant women, the elderly, and people with disabilities. However, Medicaid won't pay for your medical care while you're in prison or jail. But if you qualify and enroll in Medicaid while incarcerated, you may be able to get care more quickly after your release. If you're in jail or prison waiting for the outcome of charges, or "pending disposition," you can create an account or log in to apply for and, if otherwise eligible, enroll in a Marketplace plan. If convicted, you'll no longer be eligible for Marketplace coverage while serving time.

If you are a formerly incarcerated individual, you are eligible for ACA insurance as long as you are living in the U.S. lawfully and are not covered by Medicare. Many formerly incarcerated individuals in the U.S. are eligible for public health insurance programs, such as Medicaid. This is especially true in states participating in the ACA Medicaid expansion, where estimates suggest that eligibility among formerly incarcerated populations is as high as 80–90%.

In states without ACA expansion, the probability of being on public health insurance is 8.8% for those without a history of incarceration and 7.3% for those with a history of incarceration. However, in states with ACA expansion, the predicted probability of being on public insurance is 16.3% for those without a history of incarceration and 23.7% for those with a history of incarceration.

If you are incarcerated and have Medicaid, you can keep it while you are in jail or prison.

Universal Life Insurance: Permanent or Temporary Solution?

You may want to see also

Explore related products

![]()

Pre-existing medical conditions

Under the Affordable Care Act (ACA), health insurance companies cannot refuse to cover you or charge you more just because you have a pre-existing condition. A pre-existing condition is a health problem you had before the date that new health coverage starts. Insurers also cannot charge women more than men. Before the ACA, Americans could be charged higher premiums, denied coverage, or dropped from their health insurance due to a pre-existing condition or serious illness.

The ACA prohibits the use of pre-existing conditions to deny coverage, increase premiums, or impose waiting periods for health insurance. This includes conditions such as heart disease, cancer, asthma, diabetes, and pregnancy. Once you have insurance, your insurer cannot refuse to cover treatment for your pre-existing condition.

The only exception to the pre-existing coverage rule is for "grandfathered" individual health insurance plans purchased before March 23, 2010. These plans were bought directly from insurance companies, agents, or brokers, rather than through an employer. Grandfathered plans are not required to cover pre-existing conditions and may have other restrictions. However, if you have a grandfathered plan and want pre-existing conditions covered, you can switch to a Marketplace plan during Open Enrollment or buy a Marketplace plan outside of Open Enrollment and qualify for a Special Enrollment Period.

The ACA has provided protections for millions of Americans with pre-existing conditions, particularly children. Before the ACA, children with pre-existing conditions could be blocked from purchasing individual market insurance. Now, insurers cannot deny coverage to children under the age of 19 based on a pre-existing condition.

In summary, if you have a pre-existing medical condition, you are eligible for ACA insurance, and your insurer cannot discriminate against you or deny you coverage because of your condition.

Irrevocable Life Insurance Trusts: Protecting Your Wealth and Legacy

You may want to see also

Frequently asked questions

Anyone living in the US can enroll in an ACA insurance plan as long as they are a US resident for tax purposes and are not incarcerated or covered by Medicare.

ACA stands for the Affordable Care Act, also known as Obamacare. It is a 2010 health reform law that makes affordable insurance widely available to everyone, including those who do not qualify for Medicaid.

You can apply for ACA insurance through your state's Health Insurance Marketplace. Each state's marketplace has its own enrollment instructions.

Your ACA insurance plan will depend on where you live, your income, your household size, and the type of plan you choose.