If you're thinking of test-driving a car at a dealership, you might be wondering if you need your own insurance. The short answer is no—dealerships are legally required to insure their inventory, and this insurance covers accidents and any damage to their cars during test drives. This special coverage is called garage liability insurance, and it's designed for commercial sellers, including new and used automotive dealers. It covers customers as well as the dealer's employees. However, if you're at fault in an accident during a test drive, the dealership could hold you liable for damages, and they may try to collect from you or your insurer. While you don't need insurance to test drive a car, it's always a good idea to be mindful and drive with extra care and caution.

| Characteristics | Values |

|---|---|

| Is insurance needed to test-drive a car at a dealership? | No, the dealership's insurance covers the car. |

| Is insurance needed to buy a car? | Yes, in most states. |

| Is insurance needed to test-drive a car from a private seller? | No, you are covered by the owner's insurance. |

| Is insurance needed to test-drive a car bought from a private seller? | Yes, once the title is transferred, the insurance responsibility shifts to the new owner. |

| Is there a specific type of insurance for test drives? | No, but additional auto insurance for test drives is recommended. |

| What type of insurance do dealerships have? | Garage liability insurance, fleet insurance, and workers' compensation insurance. |

| What happens if an accident occurs during a test drive? | The dealership's insurance will cover the cost of damages, but they may hold you liable and try to collect from you or your insurer. |

Explore related products

What You'll Learn

![]()

Dealership insurance

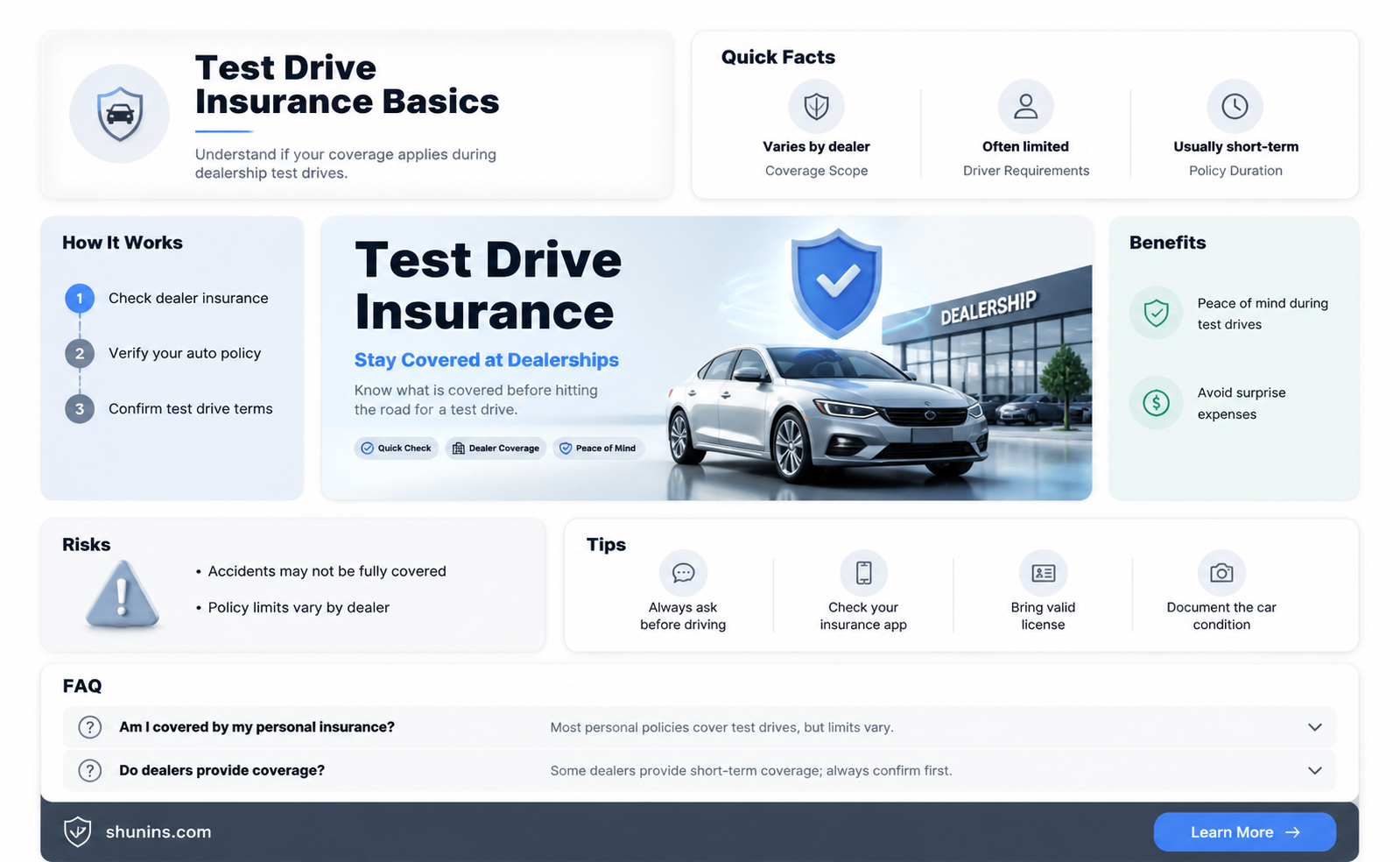

While dealership insurance will typically cover you during a test drive, it is important to note that you may still be held liable for any damages or injuries caused. The dealership may seek to recoup repair costs from you or your insurer, especially if the accident was caused by reckless driving or negligence. Therefore, it is recommended to drive with extra care and caution during a test drive. Some dealerships may also require you to sign a "`loaner/demo` agreement" or a waiver before allowing you to test drive a vehicle.

In most cases, your current insurance will cover the vehicle once you drive it off the dealership lot. However, it is important to verify coverage with your insurer and increase your liability insurance if necessary. Additionally, purchasing gap insurance can help cover the difference between what you owe on the vehicle and its actual value if it is totaled.

While insurance is not required for a test drive, it is always a good idea to have adequate insurance coverage when driving any vehicle. If you are concerned about the dealership's insurance coverage, you can consider purchasing separate insurance, such as temporary insurance or non-owner auto insurance, to protect yourself during the test drive. This will give you peace of mind and ensure that you are covered in the event of any accidents or incidents.

MetLife Auto Insurance: Understanding Their Rating System

You may want to see also

Explore related products

![]()

Your insurance

If you are planning to test drive a car at a dealership, you may be wondering whether your insurance will cover you. The good news is that, in most cases, you will be covered by the dealer's insurance policy. Dealerships are required to insure their inventory, and this insurance typically covers accidents and any damage to their cars that might occur during test drives. This type of policy is known as garage liability insurance and is designed specifically for commercial sellers and automotive dealers. It covers the dealer's employees and customers.

While the dealership's insurance will likely cover you in the event of an accident during a test drive, it's important to remember that you could still be held liable for damages if the accident was caused by reckless driving or negligence. In such cases, the dealership may initially pay to repair the car but could then seek to collect the costs from you or your insurer. Some dealerships may also ask you to sign a "loaner/demo" agreement or a waiver before allowing you to test drive a vehicle. This agreement may outline your responsibility for any damage that occurs during the test drive.

It is always a good idea to ask questions and understand the dealership's insurance policy and test drive protocol before getting behind the wheel. You can inquire about their insurance coverage, including the deductible amount and whether they have had any previous accidents during test drives. Additionally, you can confirm whether they require a copy of your driver's license, proof of insurance, or any other documentation.

While it is generally not necessary to have your own insurance policy in place before test-driving a car at a dealership, there are some additional insurance options you can consider for extra protection. For example, you could purchase temporary insurance coverage specifically for the test drive, which can last from one hour to six months. This type of policy can provide peace of mind and give you time to decide on the most appropriate auto insurance for your new vehicle.

Finally, keep in mind that once you have purchased the car, you will need to provide proof of insurance before driving it off the dealership lot. If you already have an active insurance policy for another vehicle, you can contact your insurance company to add your new car to the policy. Alternatively, you can purchase a new policy directly from an insurer or through an online marketplace.

Auto Accident Deductibles: Tax Write-off?

You may want to see also

Explore related products

![]()

No insurance

If you don't have car insurance and want to test drive a car at a dealership, you're in luck. In most cases, you do not need your own insurance to test drive a car at a dealership. Dealerships are legally required to insure the cars on their lot, and this insurance covers customers test-driving their vehicles. This insurance is called garage liability insurance, and it covers accidents, damage, and personal injuries sustained during a test drive. It is designed for commercial sellers, including new and used car dealers, and their employees.

However, it is important to note that dealership insurance may not always cover all damages or injuries incurred during a test drive. Some policies may have limitations or deductibles, so it is essential to carefully read and understand the terms of the dealership's insurance policy before assuming you are fully covered. In some cases, you may be held liable for any damage that exceeds the limits of their coverage, so having your own insurance policy as backup can be beneficial.

Additionally, some dealerships may ask you to sign a "loaner/demo" agreement before a test drive, especially if you plan to drive for an extended period or without a salesperson present. By signing this waiver, you accept liability for any damages you may cause to the vehicle during the test drive. Therefore, it is recommended to verify with your insurance agent that your policy will cover you in such instances.

While not mandatory, having your own car insurance is always a good idea. It can provide secondary coverage if the dealership's insurance has limitations and protect you from liability if you cause an accident while test-driving a car. You can also purchase temporary insurance coverage specifically for test drives, giving you a grace period to consider your options.

In summary, while you typically do not need your own insurance to test drive a car at a dealership, it is essential to understand the dealership's insurance policy and the extent of its coverage. Having your own insurance can provide additional protection and peace of mind during the test drive.

Auto Adjusters: An Endangered Species?

You may want to see also

Explore related products

![]()

Fault and no-fault states

If you are test-driving a car at a dealership, you do not need to have your own car insurance policy. Dealerships are legally required to insure the cars on their lot, and this insurance covers accidents and any damage to their cars that might occur during test drives. This insurance is called garage liability insurance, and it covers customers as well as the dealer's employees. In most states, the dealership's insurance policy will cover you in the event of an accident, but the dealer might still hold you liable for damages, depending on the cause of the accident. In such cases, the dealership may initially pay to repair the car, and then seek to recoup the costs from you or your insurer.

Now, when it comes to fault and no-fault states in the US, there are some important distinctions to be aware of. No-fault insurance, also known as personal injury protection insurance (PIP), is a type of coverage that helps pay for you and your passengers' medical expenses, loss of income, and more in the event of an accident, regardless of who is at fault. In a "tort state", on the other hand, the insurance company of the individual found to be at fault pays for all damage costs in the event of an accident. As of 2016, there were 18 states that required drivers to purchase no-fault/PIP coverage, while the remaining states used a tort system. However, it's important to note that these laws can change, so it's always a good idea to check with a local agent to confirm the specific requirements of your state.

Currently, there are 12 true no-fault states, and some states, like Kentucky, New Jersey, and Pennsylvania, are known as "optional no-fault" or "choice no-fault" states, where drivers can choose whether they want to be part of a no-fault system. In no-fault states, drivers must file a claim with their own insurance company for medical-related costs, regardless of who caused the accident. This can lead to higher insurance premiums in no-fault states, as insurers have to pay out claims regardless of fault, and there is a higher risk of insurance fraud or exaggerated injury claims.

The fault system was created to reduce the number of small lawsuits resulting from car accidents and to help lower insurance costs. In a fault state, if you are found to be at fault, you can still be sued by the other driver, but only if their medical bills meet a certain monetary threshold. No-fault insurance laws vary from state to state, so it's always a good idea to understand the specific rules and requirements of your state when it comes to car insurance.

Auto Insurance Basics: What Every Driver Should Know

You may want to see also

Explore related products

![]()

Additional insurance

While insurance is not required to test-drive a car at a dealership, you may want to consider purchasing additional insurance for peace of mind. Dealerships are legally required to insure the vehicles on their lot, and this insurance will cover you in the event of an accident. However, if you are found to be at fault, the dealership may subrogate and try to collect from you or your insurer for the cost of repairs.

There are a few options for additional insurance when test-driving a car. One option is to purchase temporary insurance coverage, which can last anywhere from one hour to six months and will provide you with a grace period to decide on the best long-term auto insurance for your new car. Another option is to get non-owner auto insurance, which will protect you from liability if you cause an accident while driving someone else's car. This type of insurance is designed for rental or borrowed vehicles, which technically includes dealership cars that you test-drive.

If you already have an active car insurance policy for another vehicle, you can call your insurance company and have them add your new car to your current policy before the test drive. Alternatively, you can purchase a new policy online or over the phone, but you will need the vehicle identification number (VIN) of the car you are buying. It is important to note that requirements may vary between dealerships and states, so it is always a good idea to discuss insurance with the dealership beforehand and review your policy documents to understand what is and isn't covered.

State Farm Auto Insurance in California

You may want to see also

Frequently asked questions

No, you don't need insurance to test drive a car at a dealership. Dealerships are legally required to insure their inventory, and this insurance covers accidents and any damage to their cars that might occur during test drives.

If you crash the car during a test drive, the dealership's insurance will cover the cost of damages to the car. However, whether the accident goes on your record depends on who is at fault. If you are at fault, the dealership could hold you liable for damages and medical costs.

No, you don't need to show proof of insurance before test driving a car at a dealership. However, the dealership may ask for a copy of your driver's license and proof of insurance.

Yes, you can usually test drive a car without insurance. However, it is better to get separate insurance, such as a policy for one-day car insurance or temporary insurance, to cover you during the test drive.