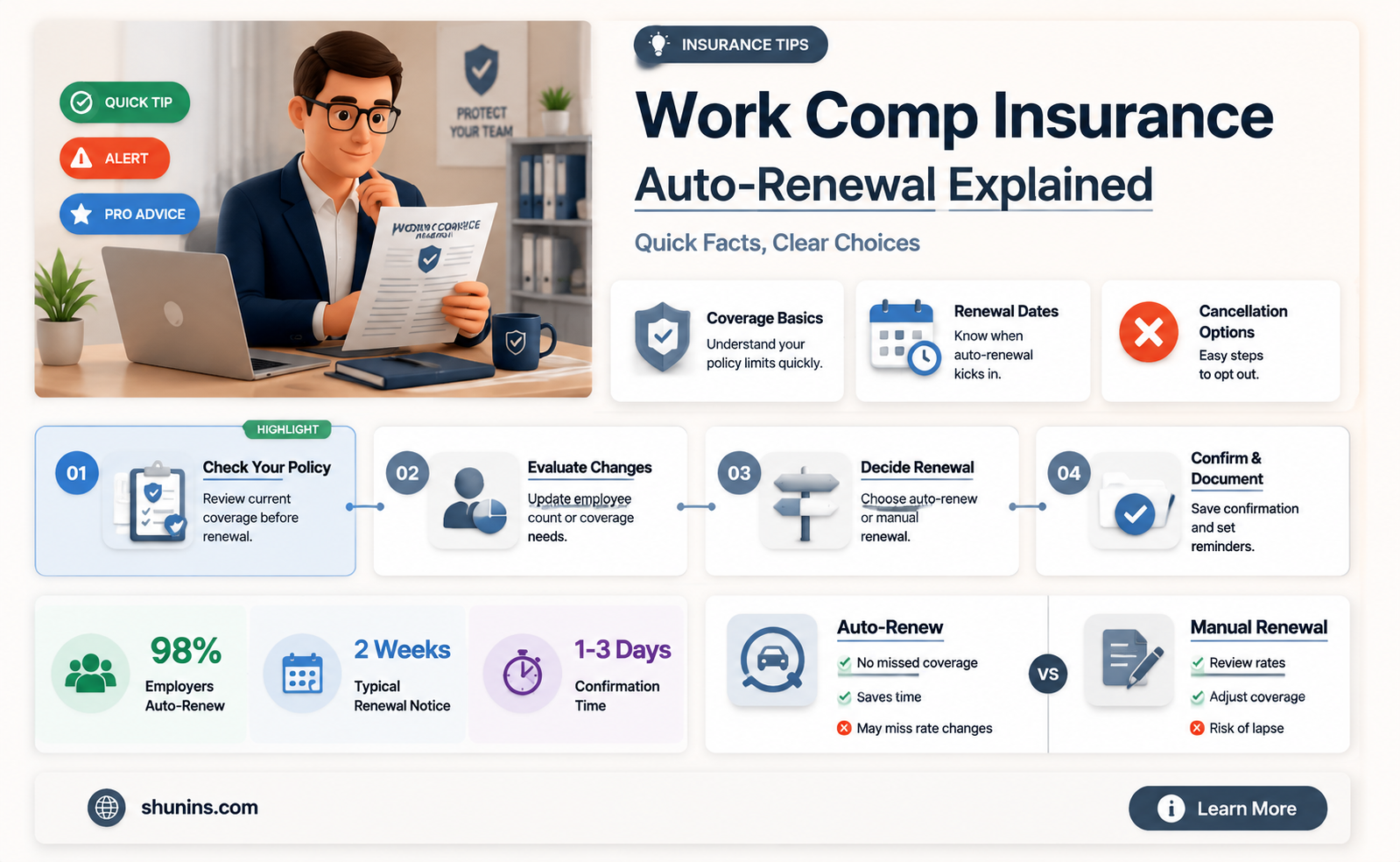

While it is unclear whether or not all work comp insurance policies are auto-renewal, it is important to understand the renewal process and the consequences of missing the renewal date. It is recommended that you ask your insurance agent to explain the steps involved in renewing the policy and if there is a grace period for doing so. Car insurance renewal is often automatic, but you should confirm it with your provider so you don't have a lapse in coverage once your policy term ends.

| Characteristics | Values |

|---|---|

| Auto-renewal | Depends on the insurance company |

| Renewal process | Ask your insurance agent to explain the steps involved in renewing the policy |

| Grace period | Ask your insurance agent if there is a grace period for renewing |

| Consequences of missing the renewal date | Ask your insurance agent to explain the consequences of missing the renewal date |

Explore related products

What You'll Learn

![]()

What is covered under work comp insurance?

Work comp insurance provides coverage for employees who fall ill or get injured while performing their job duties. It covers medical expenses and lost wages, and also provides death benefits in the event of a fatal incident. In some states, it can also protect businesses from lawsuits.

There are five basic types of workers' compensation benefits:

- Medical care: Injured workers are entitled to receive all necessary medical treatment to cure or relieve the effects of a work-related injury or illness. This can include physician services, hospitalization, physical restoration, physical therapy, chiropractic treatment, dental care, prescriptions, x-rays, and laboratory services.

- Temporary disability benefits: When a worker is unable to return to work within three days of their injury or illness, they are entitled to temporary disability benefits to partially replace lost wages. These benefits are generally payable every two weeks until the employee is able to return to work or until their condition becomes permanent.

- Permanent disability benefits: If a work-related injury or illness results in permanent impairment, the employee may become eligible for permanent disability benefits. The amount received is based on a formula that considers the extent of the physical injury or disfigurement, the age of the employee, their occupation, and the date of injury.

- Supplemental job displacement benefits: This benefit provides a voucher for education-related retraining and/or skill enhancement. It can be used to pay for tuition, fees, books, tools, or other expenses at approved schools or training providers.

- Death benefits: When a worker is fatally injured on the job, reasonable burial expenses are paid, and qualified surviving dependents may receive support payments.

In addition to these five basic types of benefits, workers' compensation insurance may also cover:

- Rehabilitation costs: This includes vocational rehabilitation to help employees return to work, as well as physical rehabilitation to aid in their recovery.

- Partial reimbursement of lost wages: Many workers' compensation incidents provide partial reimbursement of lost wages.

- Survivor benefits: In the event that a worker is killed while on the job, their survivors may be entitled to benefits such as support payments.

It is important to note that the specific benefits covered under workers' compensation insurance can vary by state and by the individual insurance policy.

Gap Insurance: When to Notify Your Provider

You may want to see also

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

![]()

How is the premium calculated?

The premium for workers' compensation insurance is calculated based on three elements: payroll, classification code, and experience modification factor (e-mod).

Payroll

Insurers will typically underwrite policies at premiums based on projected payroll. Once the fiscal year is over, the insurer will reassess the incurred payroll expenses and either credit your account (refund premiums) or debit your account (charge you more in premiums). Wages, overtime, bonuses, incentive plans, holiday and sick leave payments will all be included in this payroll projection. However, tips, group insurance and pension plans, severance pay, and expense reimbursement will not be taken into account when calculating your workers' comp premium.

Classification Code

In the world of workers' comp insurance, a four-digit number known as a class code is used to explain your entire job. These codes are classified and maintained by the National Council for Compensation Insurance (NCCI) or a state-sponsored classification. The NCCI is the insurance industry's primary source for analyzing the risk profiles of various forms of employment to effectively underwrite workers' compensation insurance. The class code rate is the amount per $100 of wages that should be paid in workers' compensation insurance premiums per employee. For example, the class code "8832" represents a chiropractor and has a class code rate of $0.14.

Experience Modification Factor (e-mod)

The Experience Modification Rate (EMR), also known as X-Mod or E-Mod, is used by the insurance industry to compare your company's workers' compensation history against industry averages to predict the risk of future claims. EMRs typically fall in the range of 0.75–1.25. An EMR above 1.0 will increase workers' compensation costs, and an EMR below 1.0 decreases costs. New businesses typically start out at 1.0 for their first three years of business. Both the severity and frequency of claims can contribute to an increase or decrease in EMR.

The formula for calculating workers' compensation insurance premiums, introduced by Embroker, is as follows: Premium = (Payroll/$100) x Class Code Rate x Experience Rate Modification.

Engine Failure: Is Your Car Insurance Useless?

You may want to see also

Explore related products

![]()

How does the claims process work?

The workers' compensation claims process can be complex and may vary from state to state. However, here is a general overview of how the claims process works:

Reporting the Injury

The first step in the claims process is for the employee to report the injury to their employer as soon as possible. While there may be no legal requirement to report a work-related injury to the employer, failing to do so promptly can cast doubt on where the injury occurred and whether it is work-related. Most companies have a written policy requiring employees to report injuries immediately, and the employer may produce documents signed by the employee confirming their awareness of this policy. Employees should provide a written report of the injury and keep copies for their records.

Filing the Claim

After the injury has been reported, the employer or the employee can file a claim with the appropriate state agency, such as the Ohio Bureau of Workers' Compensation (BWC) or the Division of Workers' Compensation (DWC) in California. The claim typically starts with completing a First Report of Injury (FROI) form, which can be submitted online or by mail. In some cases, a managed care organization (MCO) selected by the employer may file the claim after being notified by a healthcare provider. It is important to inform healthcare providers that the injury is work-related when seeking treatment.

Claim Review and Response

Once the claim has been submitted, the state agency will review it and respond within a certain timeframe, typically around 28 days. During this time, they may request additional information or documentation regarding the claim. It is important to respond promptly and provide all the necessary information to increase the likelihood of the claim being approved. An experienced workers' compensation attorney can assist in gathering evidence and supporting the claim.

Approval or Denial of the Claim

After reviewing the claim, the state agency will either approve or deny it. If approved, the employee will receive medical care and wage replacement benefits. If the claim is denied, there is usually an appeals process that the employee can follow. This typically involves filing an appeal in writing within a specified timeframe and attending a hearing to present their case. An attorney can provide valuable guidance and support during the appeals process.

Receiving Benefits

If the claim is approved, the employee will receive benefits to cover their medical expenses and replace lost wages. These benefits may include medical care, temporary disability benefits, permanent disability benefits, supplemental job displacement benefits, and death benefits. The specific benefits available may vary depending on the state and the circumstances of the injury.

It is important to note that the claims process can be intricate, and there may be variations depending on the state and the specific insurance provider. It is always advisable to consult with a knowledgeable insurance agent or attorney to understand the specific requirements and procedures for filing a workers' compensation claim.

Auto Insurance: Hit and Run Protection

You may want to see also

Explore related products

![]()

What is the role of the insurance agent?

An insurance agent is a person employed to sell insurance policies to clients. They can work for an insurance company, refer clients to independent brokers, or work as an independent broker.

The role of an insurance agent is to sell and negotiate insurance policies to match the needs of their clients. They must evaluate the needs of their clients and propose plans that meet the criteria and the client's financial status. This involves understanding the client's financial capacity by scheduling meetings, determining the extent of their present coverage and investments, and building long-term goals.

Insurance agents also have a role in maintaining relationships with existing clients. They are a reliable first point of contact when a client needs to file a claim, increase their coverage, or has any other insurance-related questions or issues.

In the context of workers' compensation insurance, an insurance agent can explain the types of injuries or illnesses covered under the policy and guide the client through the claims process. They can also assist in filing a claim, which involves timely reporting and connecting injured workers with the right care.

Additionally, insurance agents can provide information about the renewal process and any consequences of missing the renewal date. They can explain the steps involved in renewing the policy and inform the client about any grace periods applicable.

Overall, the role of an insurance agent is to sell insurance policies, build and maintain client relationships, and provide guidance and assistance throughout the insurance process, including claims and renewals.

Return-to-Invoice GAP Insurance: What's Covered?

You may want to see also

Explore related products

![]()

Are there any exclusions in the policy?

While workers' compensation insurance is a requirement for almost all employers, there are some exemptions. These vary from state to state, but generally, sole proprietors, independent contractors, and members of limited liability companies (LLCs) are exempt from coverage.

In some states, certain types of workers are also exempt. For example, in Arkansas, farm labourers, real estate agents, and domestic workers are not covered by workers' compensation insurance. In California, independent contractors are not required to be covered.

Executive officers and owners of businesses are typically not included in workers' compensation insurance, but they can choose to be. Each state has different rules regarding the inclusion of officers and owners, and some states provide exceptions for certain owners and officers to be automatically covered or to elect exclusion from the policy.

It is important to note that even when workers' compensation coverage is not required, it may still be in the employer's best interest to provide it. If an employee is injured on the job, the employer could be held liable for medical expenses, ongoing therapy, and lost wages.

Capital One: Gap Insurance Coverage

You may want to see also

Frequently asked questions

It is essential to understand the renewal process and the consequences of missing the renewal date. Ask your insurance agent to explain the steps involved in renewing the policy and if there is a grace period for renewing.

Auto-renewal is when an insurance company automatically renews a policyholder's insurance policy at the end of the policy period.

No, not all insurance companies auto-renew. It is important to check with your insurance company to see if they auto-renew.

If your insurance company doesn't auto-renew, you will need to renew your policy manually. You can do this by contacting your insurance agent or company and following the steps they provide.

If you miss the renewal date, your policy may lapse and you may be subject to a penalty or increased rates when you renew your policy. It is important to renew your policy as soon as possible to avoid a lapse in coverage.