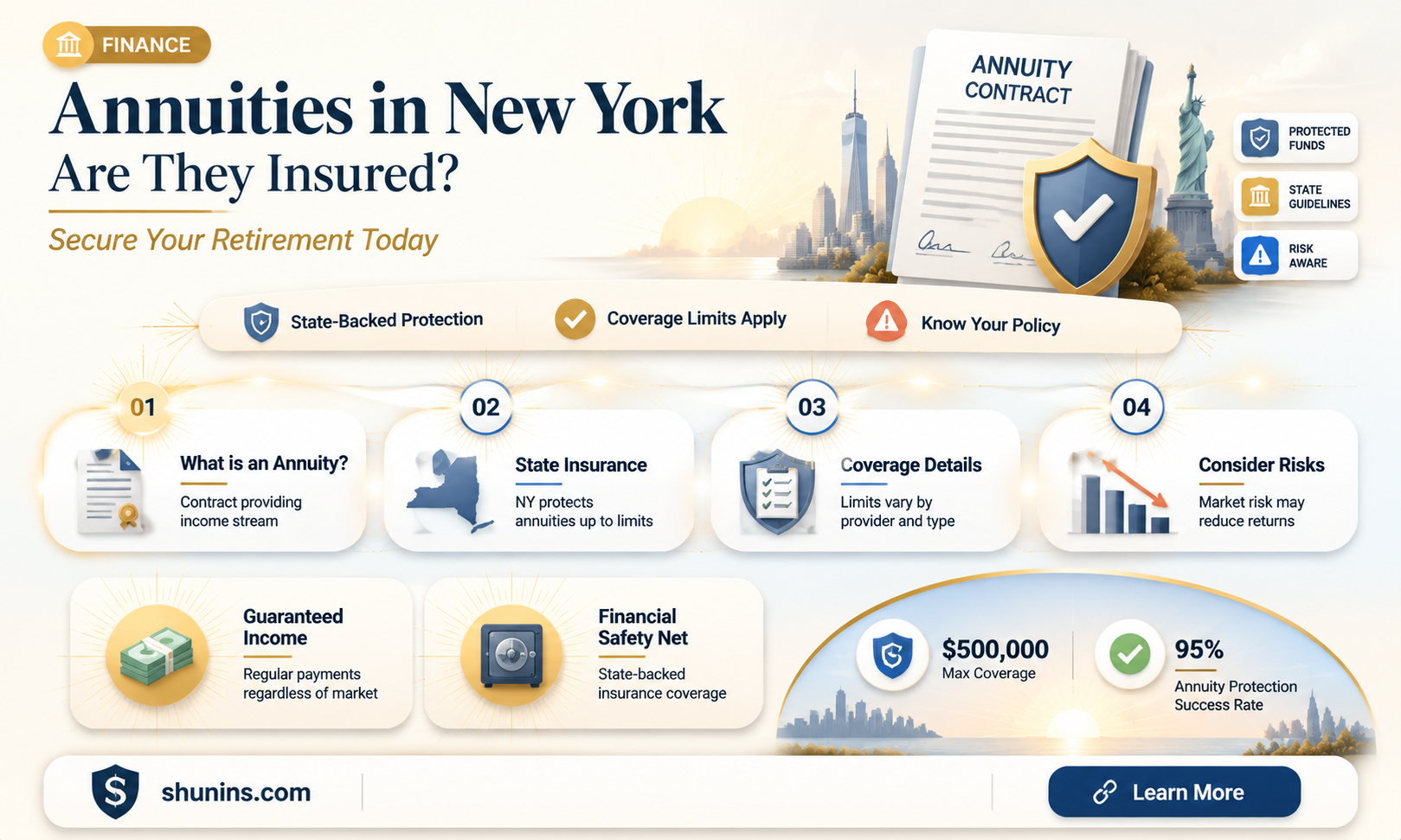

Annuities are long-term insurance contracts that convert retirement savings into a steady income stream. They are typically used for retirement planning and are purchased with a single premium. In New York, annuities are issued by New York Life Insurance and Annuity Corporation and its parent company, New York Life Insurance Company. Annuity customers are protected by insurance guaranty associations at the state level, which will pay out claims in the event that an insurance company becomes insolvent. In New York, the Guaranty Fund provides up to $500,000 of coverage for individual annuity contract holders.

| Characteristics | Values |

|---|---|

| Annuity definition | A contract between a purchaser and an insurance company in which the purchaser agrees to make a lump-sum payment or series of payments in return for regular disbursements, beginning either immediately (within 12 months) or at a future date. |

| Types of annuity contracts | Immediate annuity, deferred annuity (paid-up deferred annuity/DIA), fixed annuity, fixed index annuity, variable annuity, mutual income annuity |

| Annuity payments | Dependent on the type of annuity contract; immediate annuity payments begin within 12 months of the purchase date, while deferred annuity payments are scheduled to commence after at least 12 months or on a specified date, such as retirement. |

| Annuity benefits | Provides a steady stream of income during retirement, with the option to leave remaining money to loved ones upon death. |

| Annuity protection | The Guaranty Fund, a non-profit New York corporation, provides protection for annuity owners in the event of insurer insolvency. The fund provides up to $500,000 in coverage for individual annuity contracts. |

| State guaranty associations | All 50 states, including New York, have insurance guaranty associations that protect annuity owners. The typical statutory limit for annuity contracts is $250,000. |

| Annuity risks | Variable annuities with market risk may result in losing money. Fixed annuities, fixed index annuities, and deferred income annuities are considered safer options as they do not lose value. |

Explore related products

What You'll Learn

![]()

Annuities are long-term insurance contracts

An annuity is a contract between a purchaser and an insurance company. The purchaser agrees to make a lump-sum payment or a series of payments in exchange for regular disbursements, beginning either immediately (within 12 months) or at a future date. The goal of most annuities is to provide a steady stream of income during retirement for a specified period or for the remainder of the annuitant's life. Annuities are long-term insurance contracts designed to provide a steady cash flow for people during their retirement years, ensuring they do not outlive their assets.

There are two basic kinds of annuity contracts: immediate and deferred. Immediate annuities are contracts in which payments start within 12 months of the purchase date. The purchaser buys the contract with a single premium, and periodic payments are generally equal and made monthly, quarterly, semi-annually, or annually. Deferred annuities, on the other hand, are contracts where income payments are not scheduled to begin for at least 12 months. The payments are deferred until a maturity date stated in the contract or a date chosen by the contract owner.

In New York, annuity products are regulated by the Department of Financial Services. The state also offers protection for annuity owners through the Guaranty Fund, a non-profit corporation that provides funds in the event of the insolvency of a licensed life insurer, health insurer, or property/casualty insurer. The Guaranty Fund provides up to $500,000 in coverage for individual annuity contract holders. Additionally, group annuity contracts, including guaranteed interest contracts, are covered by the Guaranty Fund with a limit of up to $1 million in coverage.

Understanding W-9 Forms for Life Insurance

You may want to see also

Explore related products

![]()

Annuities provide a guaranteed income stream

Annuities are a contract between a purchaser and an insurance company, where the purchaser agrees to make a lump-sum payment or a series of payments in return for regular disbursements. The goal of most annuities is to provide a steady stream of income during retirement, which is guaranteed for life. This income is not impacted by economic conditions or market performance and continues for as long as the annuitant lives.

Annuities are a popular option for those who want to ensure they do not outlive their income. The purchaser is often the annuitant and the person to whom the periodic payments are made. There are two basic types of annuity contracts: immediate and deferred. An immediate annuity starts making payments within 12 months of the date of purchase, whereas a deferred annuity defers payments for at least 12 months or until a maturity date stated in the contract.

Immediate annuities can be further categorized into lifetime annuities, which provide income for the rest of the annuitant's life, and short-term annuities, which provide income for a fixed period. Deferred annuities include fixed annuities, which offer growth at a guaranteed interest rate, and variable annuities, which invest payments into mutual funds and are subject to market risks.

In New York, annuities are insured by the Guaranty Fund, a non-profit corporation that provides funds to residents and certain non-resident policy owners in the event of the insolvency of a licensed life, health, or property/casualty insurer. The Guaranty Fund provides up to $500,000 in coverage for individual annuity contract holders, with a total invested coverage of up to $1 million for group annuity contracts.

Bank of America: Life Insurance for Account Holders?

You may want to see also

Explore related products

![]()

Annuities are tax-deferred

There are two types of annuities: qualified and non-qualified. Qualified annuities are purchased with pre-tax money, and all payouts are taxed. Non-qualified annuities are purchased with after-tax money, and only the earnings are taxed.

If you withdraw money from a qualified annuity, you will pay taxes on the entire distribution amount. With a non-qualified annuity, you will pay taxes on the distributions of interest or earnings, but not on distributions of the premium or principal you initially deposited.

It's important to note that if you take money out of an annuity before you are 59 and a half years old, you may have to pay an extra 10% IRS penalty on the amount withdrawn. This is known as an early distribution penalty.

Annuities can be a valuable tool for deferring and managing taxes, but it's always a good idea to talk to a professional before making any decisions about your financial strategy. A financial advisor can help you understand the tax implications of annuities and how they fit into your overall retirement plan.

Insurance Simplified: AW Insurance Ltd Airdrie, AB

You may want to see also

Explore related products

$14.87 $19.99

![]()

Annuity contracts: immediate vs. deferred

When choosing an annuity contract, you can select between an immediate annuity and a deferred annuity. Both types are available in fixed, variable, or indexed forms, but they differ in terms of timing and flexibility.

An immediate annuity is designed for individuals in or near retirement who want to convert their retirement savings into a steady and secure cash flow. It does not include an accumulation period, and you can start receiving payments within one year of purchasing the contract. This quick conversion into retirement income makes immediate annuities less flexible than deferred annuities.

Immediate annuities can be purchased with a single premium payment, providing income for life. They are similar to pension plans in this regard. Most immediate annuities also offer a death benefit, allowing beneficiaries to receive the remainder of the scheduled payouts if the contract owner passes away before the contract is annuitized or during the annuitization period.

On the other hand, a deferred annuity is a long-term insurance contract that allows you to accumulate wealth over time before withdrawals begin. It provides tax-deferred growth, meaning you won't pay income taxes on your annuity gains until you receive the payouts. This helps your money grow and accumulate value over time. Deferred annuities can be purchased using a lump-sum payment or premium payments made over time. Once the accumulation phase is complete, the contract owner can choose from various distribution options, such as annuitization into monthly payments or lump sums, depending on the contract terms.

One of the primary disadvantages of deferred annuities is their complexity. Each annuity contract is customized to the owner's needs and may include numerous terms and conditions that can be challenging to understand without the assistance of a financial professional. Additionally, deferred annuities often carry higher charges and fees compared to other investment options, including surrender charges. These charges apply if you want to access your money before a certain period, making deferred annuities less liquid than other investments.

Life and Health Insurance Licenses: Ohio's Career Gateway

You may want to see also

Explore related products

![]()

Annuity protections in New York State

Annuities approved for sale in New York must adhere to specific financial protections for buyers. These protections are designed to safeguard consumers and ensure they receive fair treatment when purchasing annuity products.

Firstly, New York mandates heightened protections and enhanced benefits for those who buy state-approved annuities. This includes a minimum "free-look" period of 10 days and a maximum of 30 days, allowing annuity buyers to review their contracts thoroughly and cancel without penalty if needed. This provision ensures that consumers have sufficient time to understand the terms of their annuity contracts and make informed decisions.

Secondly, the state has adopted the Suitability and Best Interests in Life Insurance and Annuity Transactions Regulation. This regulation requires brokers, agents, and insurers to act in the best interest of the consumer when recommending annuities. By law, they must consider the buyer's needs, objectives, risk tolerance, financial situation, and other relevant factors. They must also disclose any conflicts of interest or compensation arrangements, ensuring transparency in their recommendations.

Thirdly, New York provides protection for annuity contract proceeds in the event of insolvency or creditor claims. The Guaranty Fund, a non-profit corporation, offers coverage of up to $500,000 for individual annuity contract holders in case their insurance company becomes insolvent. Additionally, under the New York State Insurance Law, certain annuity contract proceeds are protected from creditors and cannot be interfered with.

Finally, the Department of Financial Services in New York requires agents and brokers to be licensed and in good standing. They have adopted rules mandating that agents and brokers act in the best interests of their clients when recommending life insurance and annuity products. This ensures that the financial well-being of consumers is prioritised over personal gains for agents or brokers.

While these protections provide a safety net for annuity purchasers in New York, it is still essential to thoroughly research and understand the terms and conditions of any annuity product before making a purchase.

Life Insurance Agents: A US Overview and Insights

You may want to see also

Frequently asked questions

An annuity is a long-term insurance contract between a purchaser and an insurance company. The purchaser makes a lump-sum payment or series of payments in exchange for regular disbursements, providing a steady income stream during retirement.

There are two basic kinds of annuity contracts: immediate and deferred. Immediate annuities begin disbursements within 12 months of the purchase date, while deferred annuities schedule payments to start at a later date, typically after 12 months.

Annuities are insured in New York through the Guaranty Fund, a non-profit corporation. The fund provides protection for New York residents and certain non-residents in the event of the insolvency of a licensed life insurer, health insurer, or property/casualty insurer. The coverage limit is typically $500,000 per insurer.

If your insurance company becomes insolvent, the Guaranty Fund will step in to provide financial protection. The fund is managed by a board of directors, including representatives of member insurers and the Superintendent of Financial Services. The fund's primary purpose is to ensure that valid claims and administrative expenses are paid.

To minimize the risk of losing money, consider choosing a fixed annuity, fixed index annuity, or deferred income annuity, as these options do not carry the same risk of loss as variable annuities. Additionally, research the financial strength and ratings of the annuity company before purchasing a contract.