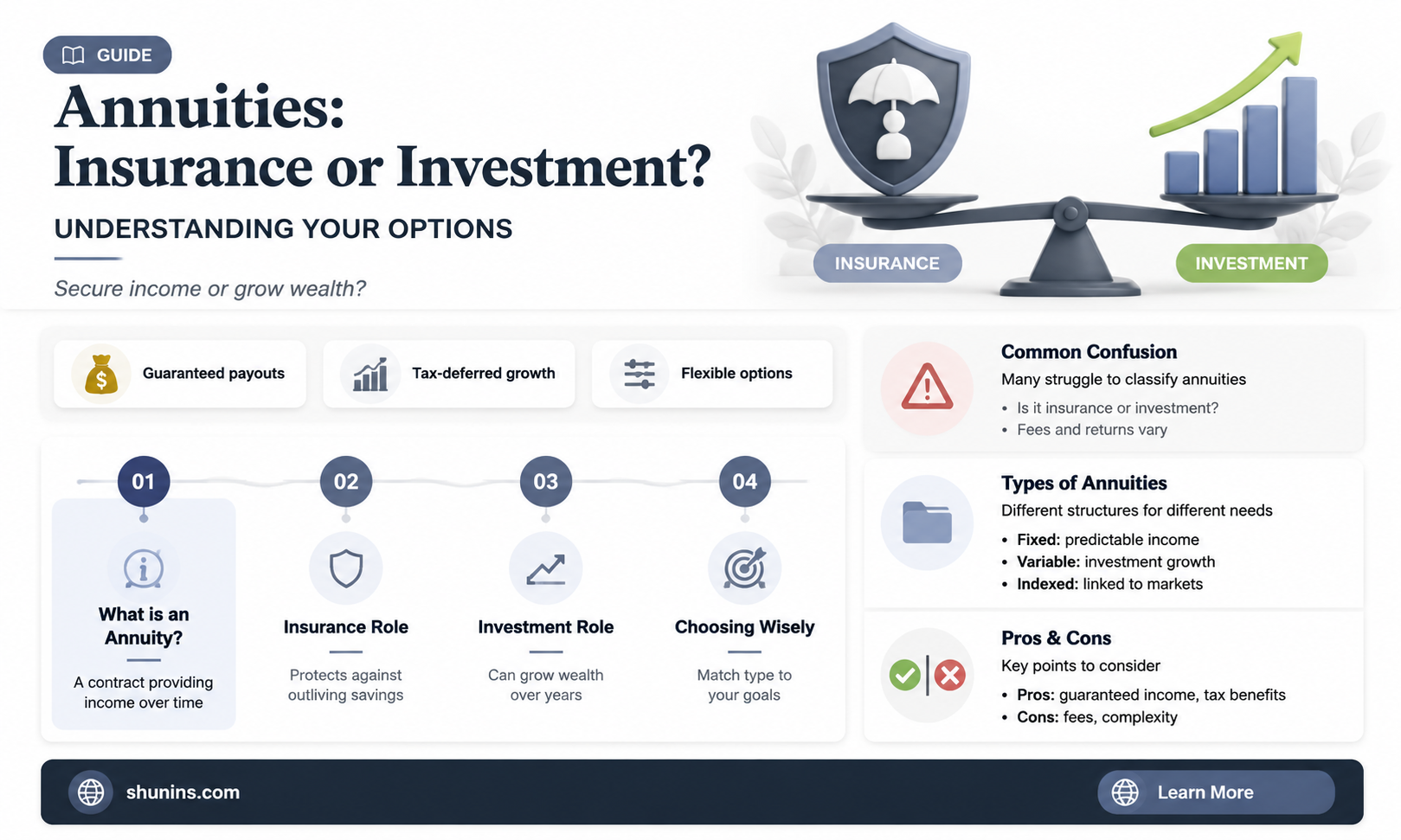

Annuities are not investments, but long-term policy contracts between an individual and an insurance company. They are financial products that offer a guaranteed income stream and are usually bought by retirees. Annuities can be immediate or deferred, fixed, variable, or indexed. They are highly customizable and can be adapted to match the buyer's needs. However, annuities are often criticised for their high fees and commissions.

| Characteristics | Values |

|---|---|

| Definition | A contract between an individual and an insurance company |

| Payment | The investor contributes a sum of money—either all upfront or in payments over time |

| Returns | The insurer promises to pay a regular stream of income in return |

| Types | Immediate, deferred, fixed, variable, indexed |

| Tax | Tax-sheltered |

| Purpose | To provide a reliable income stream in retirement |

| Criticism | High fees, high commissions, illiquidity, complexity, costly |

Explore related products

What You'll Learn

- Annuities are not investments, but long-term policy contracts between individuals and insurance companies

- Annuities can be immediate or deferred, fixed or variable, and indexed

- Annuities are tax-deferred, but withdrawals before the age of 59 1/2 may be taxed

- Annuities may have early withdrawal penalties and surrender charges

- Annuities are regulated by state insurance commissioners, but variable annuities are also regulated by the SEC and FINRA

![]()

Annuities are not investments, but long-term policy contracts between individuals and insurance companies

Annuities are long-term policy contracts between individuals and insurance companies, not investments. They are designed to provide a guaranteed income stream, usually for retirees.

Annuities are a contract between an individual and an insurance company, where the individual pays either a single payment or a series of payments, and in return, the insurance company makes regular payments to the individual, either immediately or in the future. Annuities can be structured in different ways, depending on the needs of the individual. For example, they can be immediate or deferred, and they can be fixed, variable, or indexed.

While annuities are not considered investments, some annuities do have investment-like characteristics. Accumulation annuities, for instance, are a long-term savings option that offers either fixed or variable performance. With a fixed annuity, the annuity will grow at a fixed rate over time, whereas a variable annuity allows individuals to invest their funds into sub-accounts tied to market-based investments.

Annuities are often used for retirement planning, as they can provide a guaranteed income stream for life. They can also be used to accumulate funds for retirement, offering tax advantages and a range of options based on an individual's risk tolerance.

It's important to note that annuities are complex financial products and can be costly, with various fees, charges, and potential penalties for early withdrawal. As such, it's recommended that individuals consult a financial advisor before purchasing an annuity to ensure they understand the contract, fees, and conditions.

Navigating the Complex World of Insurance: Strategies for Negotiating Hospital Bills

You may want to see also

Explore related products

![]()

Annuities can be immediate or deferred, fixed or variable, and indexed

Annuities are contracts with insurance companies that provide investors with a future payout in regular instalments, usually monthly and often for life. They are typically used to supplement other sources of retirement income, such as pensions and Social Security benefits. Annuities can be immediate or deferred, fixed or variable, and indexed.

Immediate or Deferred

Immediate annuities begin paying out soon after the buyer makes a lump-sum payment to the insurer. Deferred annuities, on the other hand, begin payments on a future date set by the buyer.

Fixed or Variable

Fixed annuities guarantee the buyer a specific payment at some future date. Variable annuities, on the other hand, fluctuate based on the returns on the mutual funds the annuity is invested in.

Indexed

Indexed annuities, also known as fixed-index annuities or equity-indexed annuities, are a hybrid of fixed and variable annuities. They typically offer a minimum guaranteed interest rate combined with an interest rate linked to a market index.

Hospital Surcharge Billing: Understanding Insurance Coverage for New Yorkers

You may want to see also

Explore related products

![]()

Annuities are tax-deferred, but withdrawals before the age of 59 1/2 may be taxed

Annuities are tax-deferred, meaning you don't pay taxes on the money in the annuity while it grows. However, if you withdraw money from a non-qualified annuity before the age of 59 and a half, you may be subject to a 10% tax penalty on top of the taxes you owe on the income. This is because non-qualified annuities are funded with after-tax dollars, so only the earnings are taxed when you withdraw. On the other hand, qualified annuities are funded with pre-tax dollars, so the entire withdrawal amount is taxed.

The tax-deferred status of annuities is one of the reasons why they are popular for retirement planning. During the accumulation phase, your money grows tax-free, and you only pay taxes when you start receiving payments, i.e., during the payout phase. This allows you to maximise the growth of your retirement savings.

However, it's important to keep in mind that annuities are complex financial products with various fees and charges, including surrender charges, mortality and expense risk charges, and administrative fees. These fees can eat into your returns, so it's crucial to understand all the costs involved before purchasing an annuity.

Additionally, annuities are not suitable for everyone. They are designed to provide a guaranteed income stream for retirees and are typically illiquid, with penalties for early withdrawals. Therefore, they may not be appropriate for younger individuals or those with liquidity needs.

Juggling Act: Understanding the Art of Balancing Bills and Insurance

You may want to see also

Explore related products

![]()

Annuities may have early withdrawal penalties and surrender charges

Annuities are long-term contracts between an individual and an insurance company, designed to provide a guaranteed income stream during retirement. They are not considered investments, but some annuities have investment-like characteristics.

The surrender charge is intended to compensate the insurance company for potential losses if you withdraw early. It also discourages annuity owners from using deferred annuities as short-term investments for quick cash. In addition to the surrender charge, the Internal Revenue Service (IRS) may assess a 10% penalty and income tax on the withdrawn funds if the annuity holder is under 59 1/2 years old.

Some annuities, such as fixed, indexed, long-term care, and variable annuities, allow for withdrawals. However, annuitized contracts, deferred income annuities, immediate annuities, and Medicaid annuities do not usually permit withdrawals.

It is important to carefully review the annuity contract to understand the specific terms and conditions governing withdrawals, including any surrender charges or early withdrawal penalties.

Accessing and Understanding Your AAA Insurance Bill Online

You may want to see also

Explore related products

![]()

Annuities are regulated by state insurance commissioners, but variable annuities are also regulated by the SEC and FINRA

Annuities are a type of insurance contract issued by financial institutions, typically insurance companies. They are designed to meet retirement and other long-term goals, providing a fixed or variable income stream to the purchaser. The purchaser buys an annuity by making either a single payment or a series of payments. In return, the insurance company makes periodic payments to the purchaser, either immediately or in the future.

Annuities are regulated at the state level by state insurance commissioners. However, variable annuities and registered indexed-linked annuities (RILAs) are also regulated at the national level by the U.S. Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA). This is because variable annuities are considered securities, while fixed annuities are not.

The SEC regulates variable annuities under policies established by the Securities and Exchange Act of 1933 and the Investment Company Act of 1940. These policies protect investors from fraud, conflict of interest, and misrepresentation. Before being offered for sale, a variable annuity must file a registration statement with the SEC, which includes a prospectus containing important information for the consumer. The SEC approves this registration statement but does not approve or disapprove the annuity itself.

FINRA, an industry self-regulating organization overseen by the SEC, supervises all registered broker dealers and their representatives. FINRA creates the rules for how broker dealers conduct their business and oversees the licensing of registered representatives.

At the state level, the National Association of Insurance Commissioners (NAIC) is the standard-setting organization for insurance regulations. The NAIC develops model state regulations for annuities and other insurance products, which states can adopt, modify, or reject. The NAIC's Suitability in Annuity Transactions Model Regulation sets standards for recommending annuity products to consumers, ensuring that their financial needs and objectives are met.

In summary, annuities are regulated by state insurance commissioners, but variable annuities are also regulated by the SEC and FINRA at the national level. This dual regulation helps protect consumers by ensuring that insurance companies and their products meet financial and operational standards.

Unraveling the Rental Insurance Billing Process: A Comprehensive Guide

You may want to see also

Frequently asked questions

What is an annuity?

What are the different types of annuities?

What are the benefits of annuities?

What are the drawbacks of annuities?