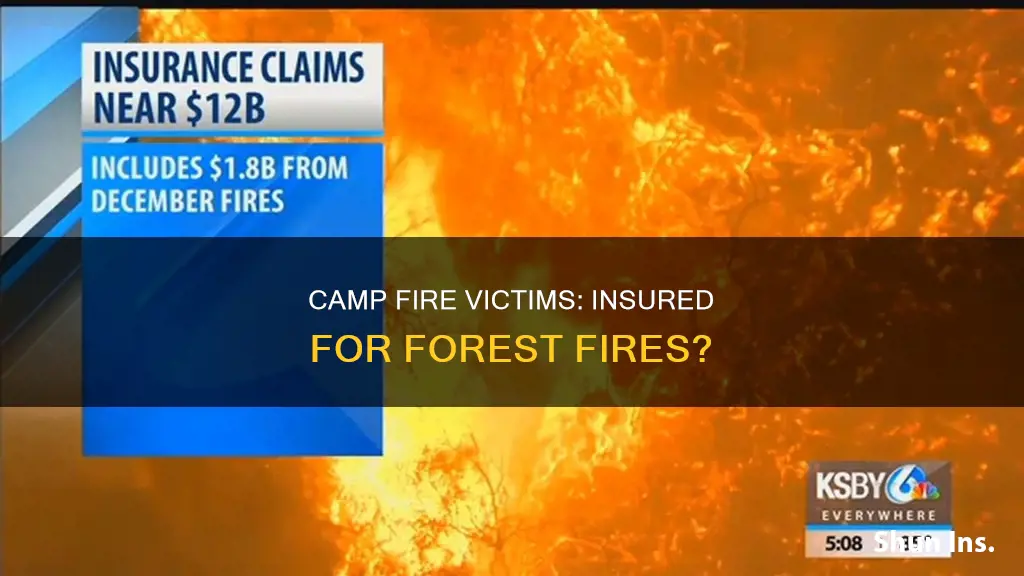

The Camp Fire was the deadliest and most destructive wildfire in California's history, causing over $16 billion in damage. While standard homeowners insurance policies typically cover fire damage to the structure of a home and belongings, insurance companies are reluctant to cover wildfires due to the high risk and astronomical costs associated with them. In the case of the Camp Fire, one-quarter of the damage, amounting to $4 billion, was uninsured. This highlights the importance of having adequate insurance coverage, especially in areas prone to wildfires, to protect against financial losses.

| Characteristics | Values |

|---|---|

| Insurance coverage for Camp Fire victims | $13.5 billion |

| Number of fatalities | 85 |

| Number of injuries | 17 |

| Number of structures destroyed | 18,000+ |

| Towns destroyed | Paradise, Concow, Magalia, and Butte Creek Canyon |

| Total damage estimate | $16.5 billion |

| Uninsured losses | $4 billion |

| Fire suppression cost | $150 million+ |

| Guilty pleas by Pacific Gas and Electric Company (PG&E) | 84 counts of involuntary manslaughter |

| PG&E bankruptcy filing | January 29, 2019 |

Explore related products

What You'll Learn

- Homeowners insurance typically covers damage to the home and belongings

- Standard policies generally protect against specific perils, including fire

- Some insurers don't sell policies in areas where wildfires are common

- People can take steps to mitigate wildfire risk, such as using noncombustible materials

- Insurance companies are working to protect themselves from liability due to wildfires

![]()

Homeowners insurance typically covers damage to the home and belongings

In the case of a wildfire, a standard homeowners insurance policy will cover the destruction and damage caused by the fire. This includes the main structure of the home, as well as outbuildings such as a garage or toolshed. The policy will also cover the cost of remediating smoke damage. Additionally, a homeowners insurance policy will also cover the loss of or damage to personal belongings, including theft or vandalism in the event of looting. Trees and shrubs are also covered under a homeowners insurance policy.

If a wildfire renders your home uninhabitable, your homeowners insurance will provide reimbursement for additional living expenses (ALE) incurred as a result, such as hotel rooms or meals. This coverage is known as "loss of use" coverage and is included in most homeowners insurance policies. It is important to note that the amount of the insurance payout will depend on the terms and limits of your specific policy.

To ensure you have adequate coverage in the event of a wildfire, it is recommended to regularly review your policy and make any necessary updates to your insurer. You may also want to consider purchasing additional coverage for specific valuables, such as jewelry or fine art, which may have limited coverage under a standard policy.

Insurance Settlements: Income or Not?

You may want to see also

Explore related products

![]()

Standard policies generally protect against specific perils, including fire

Standard fire insurance policies generally protect against specific perils, including fire. This means that the policyholder is covered in the event of fire, whether it originates inside or outside the home. Fire insurance is a form of property insurance that covers damage and losses caused by fire. It is often included as part of homeowners, condo, or renters insurance.

A standard fire insurance policy may cover the following:

- Damage caused by fire, including wildfires.

- Repair or reconstruction of the property.

- Replacement of damaged belongings.

- Additional living expenses if the home becomes uninhabitable due to a fire.

- Smoke or water damage due to a fire.

- Injuries sustained by someone on the property.

It's important to note that fire insurance policies typically have general exclusions, such as war, nuclear risks, and deliberate fires. Additionally, there may be limits to the coverage provided, and it's important to review your policy regularly to ensure adequate protection.

In some cases, homeowners may want more extensive coverage, especially if their property contains valuable items. Separate fire insurance can be purchased as a stand-alone policy, providing additional protection against fire-related risks. This can be especially useful in areas prone to natural disasters or wildfires.

Injuries Insurance: What Counts as 'Major'?

You may want to see also

Explore related products

![]()

Some insurers don't sell policies in areas where wildfires are common

Wildfires have burned nearly 10 million acres of forest and destroyed 39,000 homes in California over the last five years. In the face of this climate crisis, many insurance companies have decided to no longer insure homes in certain parts of the state, while others have left the home insurance market altogether. This has left many Californians with little to no options for homeowners insurance, particularly those in areas most at risk of wildfire damage.

Insurers are pulling back coverage in wildfire-prone areas or exiting the state entirely. For example, Allstate, California's fourth-largest home insurer, has stopped writing new policies in the state, though they will continue to renew existing ones. State Farm, California's largest home insurance provider, has also ceased writing new policies but will continue to issue renewals to existing customers. Other companies, like Farmers Insurance, have placed a cap on new policies.

If you live in an area where wildfires are common, damage caused by wildfires may not be covered by your homeowners insurance, or you may pay a higher rate and/or carry a separate deductible for wildfire claims. Many insurers don't offer coverage in fire-prone areas or exclude coverage for wildfire damage. This is because insurers need to remain profitable enough to comply with state law and pay out the claims of their existing customers, which has proven difficult in recent years due to wildfire losses and other factors.

If you're unable to obtain coverage from a private company, you may be able to get insurance from your state's Fair Access to Insurance Requirements (FAIR) Plan. These plans are designed to give homeowners with high exposure to events beyond their control, such as wildfires and windstorms, access to insurance when they can't get protection under a standard homeowners policy. However, FAIR plans are usually more expensive and have lower coverage limits than standard policies, so it's recommended to explore all other options first.

Unraveling the Mystery of Return-on-Payment Term Insurance Plans

You may want to see also

Explore related products

![]()

People can take steps to mitigate wildfire risk, such as using noncombustible materials

People can take several steps to reduce the risk of damage to their homes from wildfires. One key strategy is to create a "defensible space" or "home ignition zone" around the home, which acts as a buffer to slow or stop the spread of fire and prevent spot fires caused by flying embers. This involves strategic vegetation management and the use of fire-safe landscaping materials.

For the area within 0-5 feet of the home, it is recommended to use noncombustible materials such as gravel, rocks, concrete, and low-growing plants. This zone should be kept clear of debris, yard waste, and combustible items like outdoor furniture, playsets, and firewood. The exterior walls, fences, and gutters in this area should also be regularly cleaned to remove any combustible materials.

For the intermediate zone, extending from 5-30 feet from the home, combustible structures like trellises, fences, fuel tanks, and wood piles should be removed. Mature trees should be spaced at least 30 feet apart, and any tree canopy should be farther than 30 feet from the home.

In the extended zone, from 30-100 feet or more, it is important to thin and separate trees, regularly prune branches, and clear dead plant materials. Spacing plants out and pruning low-hanging branches can help reduce the fuel available for a fire and block wind-blown embers from reaching the home.

In addition to creating defensible space, people can also take steps to protect their homes by using fire-resistant building materials. This includes using fire-resistant roofing materials, such as those with a Class A fire rating, and building or remodelling exterior walls and decks with fire-resistant materials. Ignition-resistant building materials include stucco, fibre cement siding, fire-resistant composite decking, and fire-retardant-treated wood.

Windows can also be made more fire-resistant by replacing old windows with multi-paned windows that have at least one pane of tempered glass. Fencing attached to the home, within the first 5 feet, should be made of noncombustible materials such as metal or aluminium.

Understanding Contracted Discounts in Insurance Billing: Unraveling the Complexities

You may want to see also

![]()

Insurance companies are working to protect themselves from liability due to wildfires

Standard homeowners, renters, and condo insurance policies typically cover damage from fires, including wildfires. However, insurance companies are increasingly concerned about the liability posed by wildfires due to their unpredictable and destructive nature. As a result, they have implemented various strategies to mitigate their risk and protect themselves from potential financial losses.

One common strategy is to exclude coverage for wildfires in high-risk areas. Insurance companies may refuse to provide coverage in wildfire-prone regions they deem too risky, specifically excluding wildfires when writing policies. They may also deny renewals or pull out of these areas entirely. This approach allows insurance companies to limit their exposure to the high costs associated with wildfire damage.

In addition, insurance companies may require higher premiums, deductibles, or separate wildfire deductibles for properties located in high-risk areas. By increasing the cost of coverage, insurance companies can deter some customers from purchasing policies or shift more of the financial burden onto policyholders.

Another strategy employed by insurance companies is to offer specialised coverage options for high-value properties. These policies often include benefits such as private firefighters, loss prevention measures, and more robust coverage limits. By targeting high-value properties, insurance companies can generate higher premiums while also providing enhanced protection for these at-risk homes.

Some insurance companies are also advocating for legislative changes that would allow them to increase rates on renewed policies more rapidly. They argue that this, paired with efforts to improve fire safety, could help stabilise the insurance market in areas prone to wildfires.

Overall, insurance companies are actively working to protect themselves from the financial liabilities associated with wildfires. By excluding coverage, increasing costs, offering specialised policies, and advocating for legislative changes, they aim to mitigate their risk and ensure their financial stability in the face of increasing wildfire activity.

Workers' Comp Loss: A Qualifying Event?

You may want to see also

Frequently asked questions

A standard homeowners insurance policy covers the structure of your home, your belongings, and any additional living expenses incurred if your home is rendered uninhabitable. The standard policy also covers outbuildings on your property, such as a garage or toolshed.

If you live in an area that is especially vulnerable to wildfires, such as brush-filled canyons and forested areas, insurance companies may refuse coverage. Some insurers may require a separate wildfire deductible, so it is important to understand what is covered and what is not.

The Insurance Information Institute recommends having preventative features such as non-combustible siding, decking, and roofing materials, covered vents, and fences that are not connected to your home. Playground equipment and vegetation should also be kept at a safe distance from your home.

Contact your insurance provider as soon as possible. They may send an insurance adjuster to assess the damage, and you will likely need to provide a completed "proof of loss" form. It is important to keep any damaged items until an insurance company representative has assessed the damage.

Review your policy regularly and let your insurer know if you have made any updates to your home. You may also want to consider buying special coverage to protect specific valuables, such as jewelry or fine art, that may have limited coverage under your homeowner's policy.