There are many factors that influence insurance rates, and these vary depending on the type of insurance in question. Car insurance rates, for example, are influenced by age, gender, driving history, credit score, and address. Life insurance rates, on the other hand, are determined by factors such as age, health, and the desired term length. While it is difficult to generalize about insurance rates across different types of insurance, there are some common factors that can influence rates across the board, such as age and changes in personal circumstances. In the case of term life insurance, rates may increase when the term ends if the policyholder wishes to renew their coverage. This is because insurance companies assume more risk by providing coverage for a longer period of time.

| Characteristics | Values |

|---|---|

| N/A | N/A |

Explore related products

![End of Term [Blu-ray]](https://m.media-amazon.com/images/I/61C-da10mXL._AC_UL320_.jpg)

![End of Term [DVD]](https://m.media-amazon.com/images/I/61zb8XLHPXL._AC_UL320_.jpg)

What You'll Learn

![]()

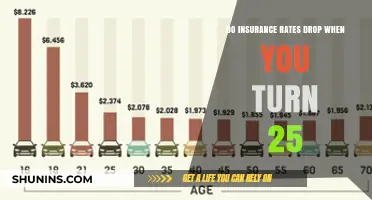

Car insurance rates and age

Age is one of the most important factors in determining your car insurance rate. While this may seem unfair, younger drivers are generally more likely to have accidents or take risks on the road. Inexperience also plays a factor, with drivers aged 16 to 19 getting into almost three times as many fatal car accidents as any other age group. As a result, insurers frequently charge more to insure teen drivers to offset the higher costs associated with teen driving claims.

The cost of auto insurance coverage generally begins to drop by the time a driver reaches their early 20s. By age 25, drivers are no longer considered "youthful operators" by insurance carriers and might notice a significant reduction in their premiums. Throughout adulthood, provided that drivers have a history of safe driving and no insurance claims, rates related to age generally level out and remain fairly consistent.

However, car insurance costs for seniors may increase, even for those with a great driving record. Older drivers can be more prone to car accidents due to physical, cognitive, or visual impairments. According to the Insurance Information Institute, accidents increase as drivers age further, and premiums gradually raise after age 70.

It is worth noting that not all states permit age as a rating factor. Hawaii and Massachusetts have banned its use, and Michigan only factors in years of driving experience. Additionally, six states do not allow gender to be used as a rating factor: California, Hawaii, Massachusetts, Michigan, North Carolina, and Pennsylvania.

While your car insurance rates won't automatically decrease once your car is paid off, your coverage requirements will change in ways that could result in premium savings. For example, you may no longer need comprehensive and collision coverage, which can save you several hundred dollars a year.

California's Driver-Based Insurance: Coverage on the Move

You may want to see also

Explore related products

![]()

How to reduce insurance rates

While insurance rates may not automatically drop when a hardship term ends, there are several ways to reduce your insurance rates. Here are some strategies to consider:

Shop Around for Better Rates

Compare insurance rates from different providers to find a more affordable policy. Each company has its own way of setting rates, so you may find a better deal elsewhere. Get quotes from at least three companies, and select the same coverages, limits, and deductibles for an accurate comparison. Your state insurance department may also provide useful information on price comparisons.

Increase Your Deductible

Raising your deductible can help lower your insurance premium. The deductible is the amount you pay out of pocket before your insurance policy kicks in. For example, increasing your deductible from $200 to $500 could reduce your collision and comprehensive coverage cost by 15 to 30%. Just remember that a higher deductible means higher out-of-pocket costs when filing a claim.

Drop Unnecessary Coverage

Review your insurance policy to identify any coverages you may no longer need. For instance, if you've paid off your car loan, you may no longer require comprehensive and collision coverage. Dropping these coverages can result in significant savings, especially if your car is an older model with a lower value.

Improve Your Driving Record

Maintaining a good driving record can help keep your insurance costs down. Avoid traffic violations, accidents, and tickets, as these can increase your rates. Consider taking a defensive driving course to improve your driving skills and qualify for a lower premium. Some insurers also offer discounts for safe driving habits, so using a company tracker program or app can help you save.

Bundle Insurance Policies

Consider bundling your insurance policies, such as combining your car insurance with renter's insurance, to obtain a more competitive rate.

Utilize Group Discounts

Inquire about group discounts through your employer, professional associations, alumni groups, or other affiliations. Many companies offer reduced rates for employees or members who purchase insurance through their group plans.

Choose a Car That's Cheaper to Insure

When purchasing a new or used car, factor in insurance costs. Choose a vehicle that is safer and cheaper to insure, as this can help reduce your premium.

Remember, while these strategies can help reduce your insurance rates, it's essential to carefully consider your specific needs and circumstances. Review your insurance policy regularly and make adjustments as necessary to ensure you have the most suitable coverage.

Explore Commercial Auto Insurance: Companies and Their Offers

You may want to see also

Explore related products

![]()

Comprehensive and collision coverage

While neither collision nor comprehensive insurance is required by law in any state, they are often required if you have a car loan or lease to protect the lender's or leasing company's assets. Once your car is paid off, you can choose to drop these coverages, but it's important to carefully weigh the pros and cons before making a decision. One rule of thumb, or the "ten rule," is to consider dropping collision and comprehensive coverage if your vehicle is worth less than ten times the annual cost of both types of coverage combined. This means that if your annual premium for collision and comprehensive insurance is $550, and your car is worth less than $5,500, it may make sense to drop this coverage.

Another factor to consider is the risk of accidents or natural disasters in your area. For example, if you live in an area with severe weather, frequent hurricanes, or wildlife strikes, maintaining collision and comprehensive coverage could be beneficial. Additionally, if you live in an area with high crime rates or frequently park on the street, comprehensive coverage can provide valuable protection against theft and vandalism.

It's also important to assess your financial situation and whether you could afford to pay for repairs or replacement of your vehicle in the event of an accident. If you have a hefty emergency fund and could cover unexpected costs without financial hardship, you may be in a better position to drop comprehensive and collision coverage. However, if your car is new or expensive to repair, dropping this coverage could leave you with significant out-of-pocket expenses.

Ultimately, the decision to keep or drop comprehensive and collision coverage depends on various factors, including your vehicle's age and value, your state's regulations and weather patterns, and your financial situation. It's essential to carefully consider your options and choose the coverage that best suits your needs and provides adequate protection.

Auto Insurance Statements: How Long to Keep?

You may want to see also

Explore related products

![]()

Policy changes and their impact

Policy changes can have a significant impact on insurance rates, and understanding these changes can help individuals make informed decisions about their coverage. While some policy changes may result in increased rates, others may lead to cost savings. Here are some key aspects to consider:

Term Life Insurance:

Term life insurance is a popular choice for individuals and families due to its affordability. This type of insurance provides coverage for a specific period, typically between five and 30 years. While it offers temporary protection, it is important to note that it might not cover individuals for their entire lives. The purpose of term life insurance is to provide financial protection during years of high expenses, such as mortgages, car payments, or childcare. Once these temporary expenses decrease, individuals may no longer need the same level of coverage.

Impact of Policy Changes:

During the policy term, insurance rates generally remain fixed unless specific changes are made to the coverage or personal circumstances. For example, adding optional services like roadside assistance or rental reimbursement can increase premiums. Similarly, increasing the dollar limits for bodily injury and property damage liability coverage will likely result in higher rates. On the other hand, removing comprehensive and collision coverage after paying off a car loan can lead to significant savings.

Age and Gender Factors:

Age is a critical factor in determining insurance rates, with rates typically decreasing as individuals get older and gain more driving experience. The most significant rate reductions occur between the ages of 18 and 19, with insurers perceiving lower risk among older teens. Rates continue to decline gradually until around age 50. Additionally, males tend to have higher rates in their teens and early 20s, but these rates drop significantly in their mid-20s as the risk difference between genders narrows.

Credit Score and Driving Record:

Improving credit scores can lead to substantial savings on insurance premiums. Moving from "poor" to "very good" credit rating can result in average monthly savings of $100. Maintaining a clean driving record is also essential, as rates usually decrease three to five years after a violation if no new incidents occur. Minor violations can impact rates for three years, while major violations can affect premiums for up to ten years.

Shopping for Better Rates:

Individuals are not bound to stick with the same high rates throughout their policy term. Shopping around and comparing quotes from different insurance companies can help find more affordable options. Tools like Experian's auto insurance comparison tool allow individuals to input their information once and receive quotes from multiple carriers. Additionally, switching to pay-per-mile coverage can be more cost-effective for those who drive infrequently.

Understanding the impact of policy changes and personal factors on insurance rates empowers individuals to make informed choices, optimize their coverage, and potentially reduce their insurance expenses.

Chevy Volt Insurance: Higher Rates, Higher Costs?

You may want to see also

Explore related products

![]()

Shopping for better rates

Shopping for better insurance rates can be a great way to save money. Every insurance company has a different way of setting rates, so it is worth comparing quotes from at least three companies to find the best deal. Online tools can help you compare rates from multiple companies at once, saving you time and money.

When shopping for better rates, it is important to consider your coverage needs. If you have paid off your car loan, you may no longer need comprehensive and collision coverage, which could save you money. Similarly, if you have an older vehicle, dropping down to liability coverage only might be a smart financial move. However, make sure that you do not put yourself at risk by becoming underinsured.

Another way to lower your insurance rates is to increase your deductible. This is the amount you pay out of pocket before insurance kicks in when filing a claim. While increasing your deductible can lower your rate, it also means you will have higher out-of-pocket costs if you need to file a claim.

Other factors that can impact your insurance rates include your age, driving history, gender, and credit score. Rates generally decrease as you get older, with the most significant decreases happening in your late teens and early 20s. Keeping a clean driving record and improving your credit score can also help lower your insurance rates.

Finally, consider combining policies and getting multi-car insurance if you are married or have a family. Insurers often offer discounts for multiple policies, and data shows that married drivers are less likely to get into accidents. By shopping around, comparing rates, and considering your coverage needs, you can find better insurance rates and save money.

Farmers Auto Insurance Claims: The Inside Story

You may want to see also