Getting a speeding ticket can be a costly mistake, and many drivers worry about how it will affect their insurance rates. In most cases, traffic tickets will increase your premiums and the amount you pay for car insurance, but this is not always the case. The impact on your insurance depends on several factors, including the state you live in, your insurance company's policies, your prior driving record, and the severity of the speeding ticket. Some insurance companies may even deny coverage if you have multiple offences.

| Characteristics | Values |

|---|---|

| Whether insurance companies are notified about a ticket | No, the DMV will not notify insurance companies about a ticket. However, insurance providers will run motor vehicle reports on their customers every 6 to 12 months and update their records and insurance policies accordingly. |

| How a ticket impacts insurance rates | A ticket may increase insurance rates, but this is not always the case. The impact depends on factors such as the insurance company, prior driving record, the nature and location of the ticket, and the number of miles over the speed limit. |

| Factors that influence insurance rates | Insurance companies consider the number of tickets, the type of conviction, and driving history. More serious offenses, such as drunken and reckless driving, will likely result in higher insurance rates. |

| Ways to mitigate the impact of a ticket | Completing a defensive driving course, contesting the ticket in court, or improving driving behavior by prioritizing safe driving can help reduce the cost of insurance over time. |

Explore related products

What You'll Learn

![]()

How does insurance find out about a ticket?

It is important to note that insurance companies do not receive direct notifications about your ticket from the Department of Motor Vehicles (DMV). Once your speeding ticket has been registered with the DMV, it will appear on your driving record, but the DMV will not proactively inform your insurance company of any tickets.

Insurance providers will typically run motor vehicle reports on their customers every 6 to 12 months. Once they have the report, they will update their records and, at the same time, update your insurance policy. If your auto insurance policy has just been renewed, then any impact that the speeding ticket has on your car insurance rate will only happen on your next renewal.

The impact of a ticket on your insurance premiums will depend on the state you live in, the company that insures you, and the severity of your ticket. For example, a traffic ticket that includes convictions such as drunken and reckless driving will immediately increase your car insurance rates. In addition, speeding in a school zone will increase your premium by an average of $342 in your first year, or $1,026 in total compounded car insurance premiums.

Most states participate in the Driver's License Compact (DLC), where they share violation information between a driver's home state and the state in which the violation occurred. Because not all states participate or share information, the impact of an out-of-state ticket may vary depending on where you receive your ticket.

Lowering Michigan Auto Insurance: How Long Does It Take?

You may want to see also

Explore related products

![]()

Will a ticket increase my insurance premium?

The impact of a ticket on your insurance premium can vary depending on several factors, including the type of violation, your driving record, and the state in which you live. While a single ticket may not always result in an immediate increase in your insurance premium, multiple tickets or more serious violations can have a significant impact.

In general, minor traffic violations, such as speeding or failing to use a turn signal, may not affect your insurance rates, especially if it is your first offence. However, if you receive multiple tickets within a short period, typically two or more speeding tickets in three years, your insurance rates are likely to increase. The increase in insurance rates can be substantial, with an average increase of $540+ per year for three years after a speeding ticket. Additionally, certain states, like Arizona, California, and Oregon, issue demerit points for traffic tickets, which can further impact your insurance rates.

More serious violations, such as driving under the influence (DUI) or reckless driving, can result in a significant increase in your insurance premium, with potential rates rising by 93% or even a refusal to insure you. These violations are considered riskier by insurance companies, and the impact on your insurance can last for several years. For example, a DUI in California can increase rates by 160% or $3500+, and the impact on your insurance rate can last for ten years.

It is worth noting that insurance companies may have different policies regarding how they treat traffic tickets. Some companies may offer lower rates for drivers with speeding convictions, while others may increase rates by only a small amount for minor violations. Therefore, it is advisable to compare insurance quotes and ask insurance providers about their policies regarding driving violations before committing to a policy.

Furthermore, there are ways to mitigate the impact of a ticket on your insurance. Many states offer the option to attend a driving safety course or traffic school to prevent the violation from appearing on your driving record, which can help maintain lower insurance rates. Maintaining a good credit score can also positively impact your insurance rates, as some states allow insurers to consider credit-based insurance scores when calculating premiums.

Gap Insurance: Ohio's Essential Coverage

You may want to see also

Explore related products

![]()

How to reduce insurance costs after a ticket

While getting a ticket can be a frustrating experience, there are several ways to reduce insurance costs. Firstly, it is important to note that not all tickets will result in increased insurance costs. Minor offences or first-time violations may not lead to higher premiums, as some insurance companies may waive any increase for first-time offenders. Additionally, some states may not charge higher insurance premiums for speeding tickets.

To reduce insurance costs after receiving a ticket, consider the following strategies:

- Shop around and compare rates from different insurance providers. Different companies may view your situation differently, and you may find more affordable premiums with another insurer.

- Increase your deductible, which is the amount you pay out of pocket before insurance coverage begins. Raising your deductible can lower your premiums, but keep in mind that you will have to pay more upfront if an accident occurs.

- Take advantage of a comparison website to obtain quotes from multiple insurers at once. This can help you find the most cost-effective option for your specific circumstances.

- If eligible, consider attending a state-approved driver improvement clinic. Completing this course may result in the removal of points from your driving record and could convince your insurance company to maintain your current rates.

- Maintain a good credit score. Insurance companies consider individuals with good credit scores to be lower-risk, which can result in lower insurance rates.

- Choose your vehicle wisely. Sports cars and high-performance vehicles are often classified as higher-risk due to their appeal to thieves and the tendency of their owners to drive more aggressively. Opting for a lower-risk vehicle may help reduce your insurance costs.

Remember, it is always important to drive safely and follow the rules of the road to avoid receiving tickets in the first place. Safe driving can help you maintain lower insurance costs over time.

Auto Insurance Agents: The Human Connection

You may want to see also

Explore related products

![]()

What to do if I get a ticket

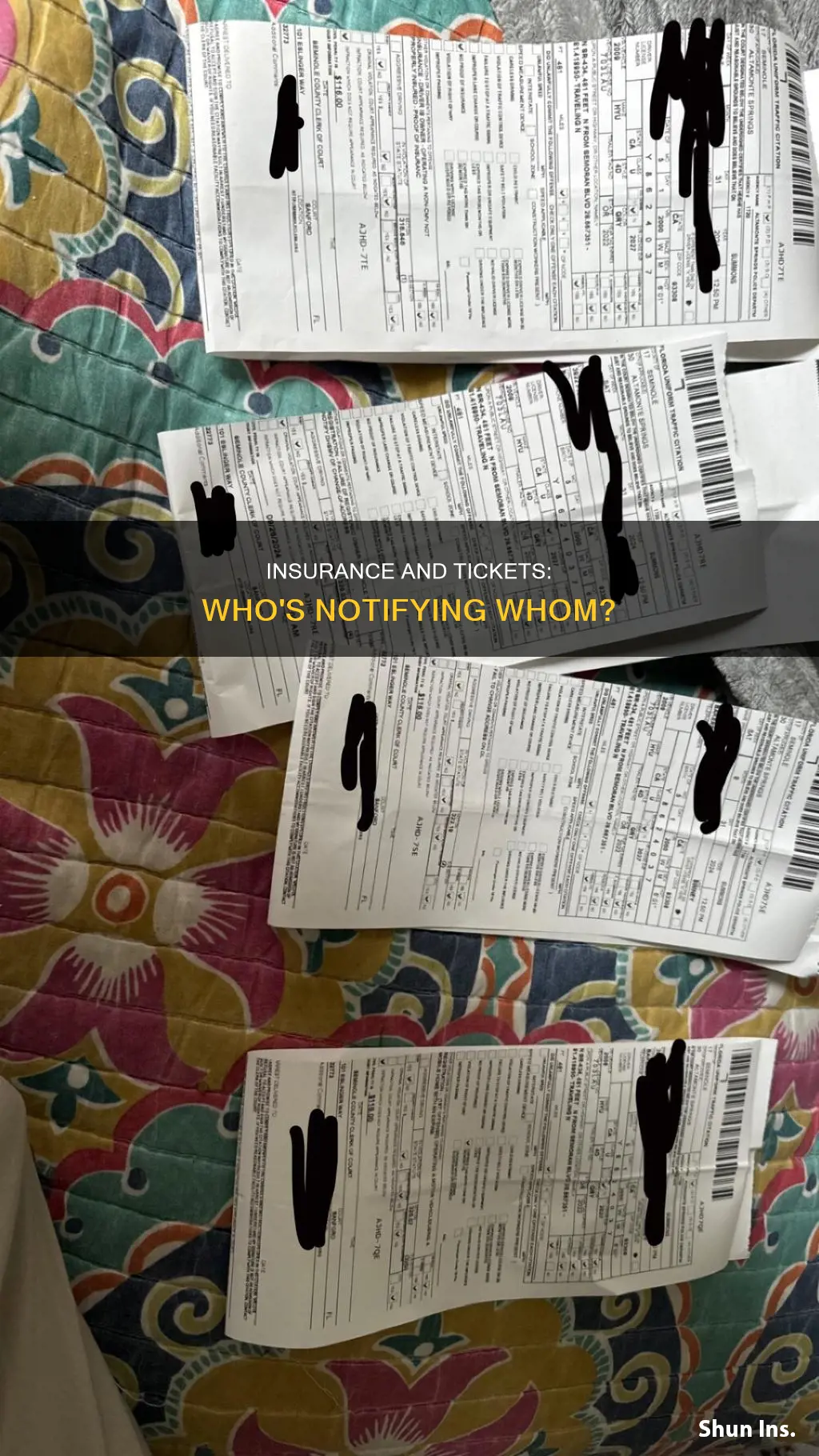

If you get a ticket, the first thing to do is to carefully read through it. The ticket will have information about how to take care of it and which county court is handling the ticket. The court's name is listed on the ticket and the notice. The ticket will also have information about the scheduled appearance in court, where you will enter your plea. You can plead guilty, not guilty, or no contest. If you plead guilty or are found guilty by a judge, it is a conviction, and this conviction goes on your driving record. These are "points" and can stay on your record for 3 to 7 years, impacting your car insurance. Your car insurance company may ask you to pay more for insurance or they may cancel your policy. If you are eligible, you can ask to go to traffic school so you don't get a point on your record. If you have a commercial driver's license, the rules are different.

If you plead not guilty, you will need to ask for a trial. If you cannot afford to pay the ticket, you can ask the court to lower the amount. You can do this at the court or on their website. You will need to answer some questions about why you cannot afford the fine. If you had a fix-it ticket, you need to pay the fine and send in proof that you fixed the problem.

It is worth noting that your insurance company may not necessarily increase your rates after a speeding ticket. If this is your first ticket, your insurance company may waive any increase in your premium. Additionally, if you have only slightly exceeded the speed limit, your insurer may not consider this reckless driving and may keep your insurance premiums the same.

Finally, it is important to be aware that your insurance provider will likely find out about the ticket. While the DMV will not directly notify your insurance company, insurance providers run motor vehicle reports on their customers every 6 to 12 months. Once they have the report, they will update your records and your insurance policy.

Get Auto Insurance in California: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

How long does a ticket stay on my record?

The duration of a ticket on your record varies depending on the type and severity of the offence. For instance, in Washington, accidents involving non-commercial vehicles remain on your record for five years from the collision date, while accidents involving commercial vehicles stay on your record for ten years. Alcohol-related convictions, such as DUIs, remain on your driving record for life.

In Texas, traffic tickets can be categorised into two main types: moving violations and non-moving violations. Moving violations, such as speeding or running a red light, are committed by a vehicle in motion and carry citations that negatively impact your driving record. Non-moving violations, like parking tickets or improper vehicle equipment, do not add any points to your driving record.

The more speeding tickets you accumulate, the more likely your car insurance rates will increase. The price of insurance after a speeding ticket depends on your state. For example, car insurance increases by about 13% on average in Texas, whereas in Michigan, drivers can expect a 52% increase. Even if the points on your license have expired, a speeding ticket may still raise your insurance costs.

Insurance companies use your driving record to assess risk, and multiple violations can classify you as a high-risk driver, leading to higher premiums and difficulty finding affordable insurance. Severe traffic offenses can lead to license suspensions, affecting your ability to commute, work, and fulfill daily responsibilities.

In Washington, revocation of a driver's license occurs if someone becomes a habitual traffic offender (HTO). This can happen if someone receives criminal convictions for three or more specified offenses within five years or is convicted of 20 or more moving violations within the same period. Once revoked, an individual's driver's license is generally not eligible for reinstatement for at least four years.

Same Household, Same Auto Insurance?

You may want to see also

Frequently asked questions

Your insurance company will not be notified about your ticket by the DMV. However, they will eventually find out about it when they run a motor vehicle report, which they do every 6 to 12 months.

Your insurance premium will likely increase after a ticket, but not necessarily. The increase depends on the type of violation, your driving record, and the policies of your insurance company. If this is your first ticket, your insurance company may waive any increase in your premium.

To prevent your insurance premium from increasing, you can contest the ticket in court or take a defensive driving course to get the ticket dismissed. If you are unable to get the ticket dismissed, you can prioritize safe driving to avoid further violations and adjust your insurance coverage to reduce costs.