Life insurance loans are a quick and easy way to get cash when you need it. They allow you to borrow against your life insurance policy if it has a cash value component and the value is high enough. This type of loan is not risk-free, however, as unpaid loans may reduce your death benefit or cost you your policy. There are also a number of other pros and cons to consider before taking out a life insurance loan.

| Characteristics | Values |

|---|---|

| Type of insurance | Permanent life insurance, including whole life, universal life, indexed universal life and variable life insurance |

| Borrowing limit | Up to 90-95% of the policy's cash value |

| Interest rates | 5-8% |

| Repayment schedule | Flexible, but interest accrues over time |

| Tax implications | Tax-free unless the policy lapses or the loan isn't repaid, in which case there may be income tax liability |

| Purpose | Emergency funds, major purchases, or to cover annual premiums |

| Advantages | Easy access to funds, no credit check, lower interest rates than personal loans, flexible repayment |

| Disadvantages | Reduced death benefit for beneficiaries, policy lapse if loan exceeds cash value, potential tax implications |

Explore related products

![Loans on Life Insurance Policies, by John M. Taylor, President the Connecticut Mutual Life Insurance Company 1913 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

What You'll Learn

![]()

Borrowing from permanent life insurance policies

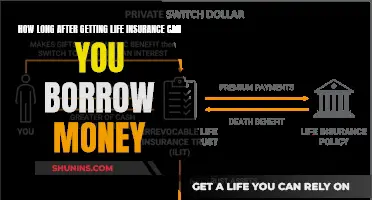

Permanent life insurance policies, such as whole life and universal life, are more expensive than term life insurance but have no predetermined expiration date. If sufficient premiums are paid, the policy is in force for the lifetime of the insured. While the monthly premiums are higher than term life insurance, money paid into the policy that exceeds the cost of insurance builds up a cash value that is part of the policy. This cash value can be borrowed against.

Permanent life insurance has several important values: the face value, the death benefit (which is often the same as the face value), and the cash value. One common misconception is that the cash value increases the death benefit. This is only true for certain types of permanent policies; on most policies, it does not increase the death benefit.

The cash value grows at a rate that depends on the type of policy. For example, in a regular universal life policy, it grows based on current interest rates, while in a variable universal life policy, the cash value is invested by the owner in the stock market and grows accordingly. It usually takes at least a few years for the cash value to build to sufficient levels to take out a loan.

Borrowing against your life insurance policy is a quick and easy way to get cash when you need it. There is no approval process or credit check since you are essentially borrowing from yourself. When borrowing on your policy, no explanation is required about how you plan to use the money, so it can be used for anything from bills to vacation expenses to a financial emergency. The loan is also not recognised by the IRS as income, so it remains tax-free as long as the policy stays active.

However, borrowing against your life insurance policy is not without risk. If you don't pay the loan back, it will be deducted from your death benefit. Worse, if the cash value dips too low and the loan remains unpaid, your policy could lapse, leaving you without coverage and potentially a tax bill.

Life Insurance Settlements: Taxable Income or Tax-Free Windfall?

You may want to see also

Explore related products

$6.99 $14.95

![]()

Pros of borrowing against life insurance

Borrowing against your life insurance policy can be a quick and convenient way to access funds when you need them. Here are some pros of borrowing against your life insurance:

Quick Access to Cash

If you've built up sufficient cash value in your permanent life insurance policy, you can easily borrow against it. There's no approval process or credit check required, making it a simple and fast way to get the money you need. This can be especially useful in emergencies or when you need quick access to cash.

Flexible Repayment Terms

Life insurance loans typically don't have a fixed repayment schedule like traditional loans. You can pay back the loan at your own pace and set your own repayment schedule. However, it's important to note that the longer the loan remains unpaid, the more interest you'll accrue.

Lower Interest Rates

Interest rates on life insurance loans are generally lower than those for personal loans or credit cards. According to MarketWatch, interest rates on life insurance loans range from 5% to 8%, making them a more affordable option for borrowers.

No Usage Restrictions

There are no restrictions on how you can spend the money borrowed from your life insurance policy. You can use it for anything from medical bills to home improvements or even a child's college tuition. This flexibility is a significant advantage over other types of loans that may have specific usage requirements.

No Impact on Credit Score

Taking out a life insurance loan won't affect your credit score, as insurers don't check your credit score before issuing the loan. This can be beneficial if you're concerned about maintaining a good credit rating.

While there are pros to borrowing against your life insurance policy, it's important to remember that there are also cons and potential risks involved. It's always a good idea to consult a financial advisor to weigh the pros and cons before making any decisions.

Irrevocable Life Insurance Trusts: Annuity Ownership Explained

You may want to see also

Explore related products

![America's Foreign Loan Policy: An Address Delivered Before the Annual Convention of the National Foreign Trade Council, Philadelphia, May 10, 1922 [1922]](https://m.media-amazon.com/images/I/61r-uzTrTqL._AC_UY218_.jpg)

![]()

Cons of borrowing against life insurance

Borrowing against your life insurance policy can be a quick and convenient way to access funds, but it's not without its drawbacks. Here are some cons of borrowing against life insurance:

Reduced Death Benefit

One significant disadvantage of borrowing against your life insurance is that it can result in a reduced death benefit for your beneficiaries. If you don't repay the loan and interest before your death, the insurance company will deduct the outstanding balance from the death benefit. As a result, your beneficiaries will receive a lower payout than they would have if you hadn't taken out the loan.

Policy Lapse

If the loan balance, including accrued interest, exceeds the cash value of your policy, your policy may lapse. This means that your coverage will be terminated, and your beneficiaries will not receive any death benefit. It's important to stay on top of your loan payments and ensure that the amount owed does not exceed the policy's cash value to avoid this situation.

Tax Consequences

In some cases, you may owe taxes on the money you borrow from your life insurance policy. If your policy lapses before the loan is fully repaid, you could owe income tax on the amount you haven't paid back. This is because you'll be able to recover the policy's "cost basis," which is usually the sum of the premiums paid on a tax-free basis. Any amount received over the cost basis may be subject to income tax.

Interest Accrual

While life insurance loans often have lower interest rates than personal loans or credit cards, interest still accrues on the borrowed amount. If you don't make regular payments, the interest can add up quickly and eat into the cash value of your policy. This can eventually lead to a policy lapse if the loan balance exceeds the cash value.

Limited Borrowing Options

Not all life insurance policies allow you to borrow against them. Life insurance loans are typically only available on permanent life insurance policies, such as whole life and universal life, which have a cash value component. Term life insurance policies, on the other hand, usually do not have a cash value, so you cannot borrow against them.

Life Insurance Usage: Assisted Living Eligibility and Conditions

You may want to see also

Explore related products

$28.45 $29.95

![]()

Interest on life insurance loans

- Interest rates for life insurance loans are generally lower than those for personal loans and credit cards, typically ranging from 5% to 8%.

- Interest on life insurance loans accrues over time, and it is important to make regular payments to prevent the loan balance from growing too large.

- The interest rate on a life insurance loan can be fixed or variable, depending on the policy.

- If the loan is not repaid before the death of the insured, the accumulated interest can reduce the death benefit paid to beneficiaries.

- In some cases, the interest on a life insurance loan may be deducted from the cash value of the policy.

- Life insurance loans do not have a fixed repayment schedule, but it is in the borrower's best interest to repay the loan as soon as possible to minimise the interest owed.

- Interest on life insurance loans is not reported to credit bureaus and therefore does not impact the borrower's credit score.

Trustage Life Insurance: Suicide Coverage and Exclusions

You may want to see also

Explore related products

![]()

Repaying life insurance loans

Repaying a life insurance loan is a crucial aspect of borrowing against your life insurance policy. While life insurance loans do not have a strict repayment schedule, it is in your best interest to repay them as soon as possible. Here are some key considerations and strategies for repaying life insurance loans:

Understanding the Importance of Repayment

It is important to recognize that if you don't repay the loan, the death benefit for your beneficiaries will be reduced. The insurance company will deduct the outstanding loan balance, including any accrued interest, from the death benefit. This means your beneficiaries will receive a lower payout.

Additionally, if the loan balance exceeds the cash value of your policy, your policy may lapse. This means you will lose coverage, and your beneficiaries will no longer be protected.

Strategies for Repaying Life Insurance Loans

- Periodic Payments: You can make periodic payments of the principal amount along with annual interest payments. This helps reduce the loan balance over time.

- Annual Interest Payments: If you are unable to make principal payments, you can opt to pay only the annual interest. However, this will result in a longer repayment period and more accrued interest.

- Deducting Interest from Cash Value: In some cases, you may be able to deduct the interest charges from the cash value of the policy. While this avoids out-of-pocket expenses, it further reduces the cash value and death benefit.

- Repay with Cash: Ideally, you would repay the loan with cash payments to the life insurance company. This increases both the policy's cash value and the death benefit by the amount repaid.

- Repay with "Excess" Cash Value: If the loan repayment amount is less than the policy's cost or tax basis, you may be able to repay the loan with "excess" cash value. However, if it exceeds this amount, it may trigger a taxable event.

- Repay with Death Benefit: If the loan balance remains outstanding upon your death, the insurance company will deduct the amount owed from the death benefit. While this option ensures repayment, it results in a reduced benefit for your beneficiaries.

Creating a Repayment Plan

When considering a life insurance loan, it is essential to create a repayment plan. Consult a financial advisor to weigh the pros and cons and ensure you understand the potential impact on your policy and beneficiaries. Additionally, you may want to set a personal repayment schedule to prevent significant interest accrual and maintain the value of your policy.

Social Security and Life Insurance: What's the Connection?

You may want to see also

Frequently asked questions

Life insurance loans allow you to borrow against your life insurance policy if it has a cash value component and the value is high enough. You can borrow from your insurance company using the cash value of your policy as collateral.

Borrowing against your life insurance policy can be a quick and easy way to get cash. There are no additional requirements, such as a credit check, and you can use the money for anything. The interest rates are also generally lower than those for personal loans and credit cards.

If you don't repay the loan with interest before you die, your beneficiaries will receive a reduced death benefit. The outstanding loan balance will also accrue interest, and if the amount you owe exceeds the cash value of your policy, it will lapse and you may be without coverage.