Life insurance is a legally binding contract between an insurance company and a policy owner, where the insurer guarantees to pay a sum of money to the beneficiaries when the insured person dies. There are five main types of life insurance: term life insurance, whole life insurance, universal life insurance, variable life insurance, and final expense life insurance. Each type of life insurance is designed to fill a specific coverage need. For example, term life insurance is geared toward those who only need coverage for a certain number of years, while whole life insurance is designed for those who need straightforward, lifelong coverage.

| Characteristics | Values |

|---|---|

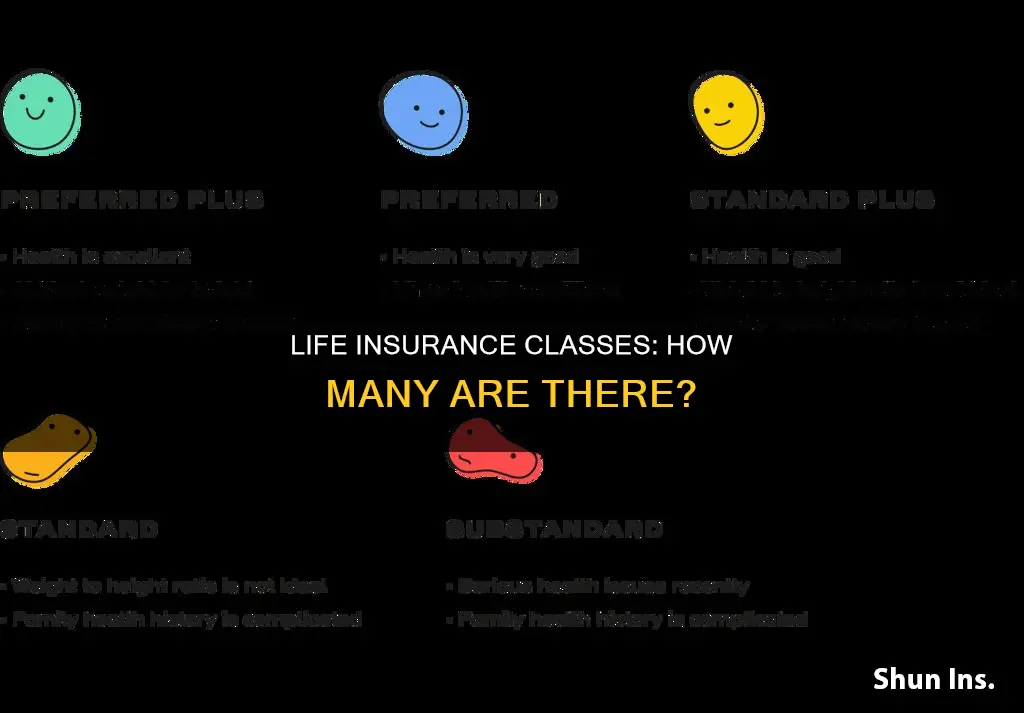

| Number of classes | 5 |

| Examples | Term life insurance, Whole life insurance, Universal life insurance, Variable life insurance, Final expense life insurance |

| Term length | Temporary (10, 20, 30 years) or permanent |

| Best for | Most people, Those who want a straightforward permanent policy, People who want permanent life insurance that can flex to future needs, Those with a higher risk tolerance who want greater control over their cash value investments, People who want to cover their own funeral, burial and other end-of-life expenses |

| Pros | Often the cheapest life insurance, Sufficient for most people, Relatively simple, Can adjust premiums and has a cash value component, Potential for considerable gains if investment choices do well, No medical exam typically required |

| Cons | If you outlive your policy, your beneficiaries won't receive a payout, More expensive than term life, Death benefit and cash value growth are not guaranteed, Requires you to be hands-on in managing your policy, Coverage is capped at low amounts |

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UY218_.jpg)

What You'll Learn

![]()

Term life insurance

There are four types of term life insurance:

- Fixed Term: The most popular choice, this is the most basic version and lasts 10, 20, or 30 years. The premiums remain static in this plan.

- Increasing Term: This type of policy allows you to scale up the value of your death benefit throughout the term. Your premiums will slightly increase over time, but these types of policies tend to cost more and deliver a larger payout.

- Decreasing Term: Decreasing term life insurance reduces the premium payments over time, which can result in a smaller death benefit. This type of insurance makes sense for those who predict they will have fewer financial obligations as they age.

- Annual Renewable: This provides coverage on a yearly basis and must be renewed by the policy end date to continue coverage. The premiums usually increase each time the plan is renewed. This option is best for those in need of short-term coverage, but it can be more expensive.

Canceling Life Insurance: A Simple Guide to Navigate Termination

You may want to see also

Explore related products

![]()

Whole life insurance

A portion of your premiums is usually put into an investment account to grow throughout the life of the plan. When the plan ends, the accrued cash value of the plan will be paid out to the beneficiary. If you name your beneficiary as an irrevocable life insurance trust, you may lower the tax liability. You can also broaden the number of beneficiaries on your policy.

There are several benefits to having a whole life insurance plan. Firstly, premiums are consistent unless you want to raise the cash value of your plan. Secondly, the death benefit will be paid to the beneficiary when the coverage ends. Thirdly, your policy builds cash at a constant rate, tax-free in a secure account. Finally, you do not need to choose a term length – your life insurance coverage lasts your whole life.

There are also some disadvantages to whole life insurance. Premiums are typically higher than term life insurance, maximising your payout in the long term. The death benefit is guaranteed, but part of your premiums will grow into a tax-deferred account. Additionally, you may be able to access the cash value of your plan before it expires.

Life Insurance: Child Coverage and Your Options

You may want to see also

Explore related products

![]()

Universal life insurance

- The interest rate for a universal life policy's cash value is not fixed. You'll have a guaranteed minimum interest rate, but in general, the rate at which your cash value builds can change over time based on market conditions.

- Your universal life policy's cash value can eventually grow and result in a zero-cost policy, in which all premiums are paid from the built-up value.

The pros of universal life insurance include:

- It is typically less expensive than whole life insurance.

- It can adapt to your needs as life changes.

- It has a savings component that grows and allows for borrowing.

The cons of universal life insurance include:

- The death benefit and cash value growth are not guaranteed.

- If cash value is your main interest, not all universal life policies guarantee you'll make gains.

- If you're interested in flexible premium payments, you have to stay on top of your policy's status to make sure that the policy's fees and charges don't deplete your cash value and cause it to lapse.

Calculating Life Insurance: The Right Coverage for Peace of Mind

You may want to see also

Explore related products

![Property and Casualty Insurance License Exam Study Guide: Property Casualty Insurance Book and Practice Test Questions [3rd Edition]](https://m.media-amazon.com/images/I/71MhA+5nDML._AC_UY218_.jpg)

![]()

Variable life insurance

When considering variable life insurance, it is important to review all the costs, including fees, and determine whether you can afford this type of policy. You should also consider how much coverage you need to meet your goals and how long you will need the insurance. Additionally, it is essential to ensure that the insurance company providing the policy is reputable and financially sound.

Life Insurance and FAFSA: What You Need to Know

You may want to see also

Explore related products

$40.11 $245.95

![]()

Final expense life insurance

Final expense insurance policies generally do not require a medical exam for approval, making them more accessible to older individuals or those with pre-existing health conditions. The application process is usually quick and easy, and coverage can be issued in days or even on the same day as the application. Once approved, coverage begins immediately and remains in place as long as the premiums are paid.

The death benefit of final expense insurance policies typically ranges from $5,000 to $40,000, with the average funeral costing around $8,300 to $10,000. This type of insurance is an affordable way to ease the financial burden on family members, providing funds for funeral, medical, and other end-of-life expenses. Final expense policies can also build cash value over time, which can be used to borrow against, withdraw, or pay premiums.

Overall, final expense life insurance is a valuable option for individuals who want to ensure their loved ones are financially protected during the final stage of life, without incurring the high costs of traditional whole life insurance policies.

Life Insurance: Am I Covered?

You may want to see also

Frequently asked questions

There are two main types of life insurance: term life insurance and permanent life insurance.

Term life insurance is designed to last a certain number of years, then end. You choose the term when you take out the policy. Common terms are 10, 20, or 30 years.

Permanent life insurance is more expensive than term life insurance, but it stays in force throughout the insured’s entire life unless the policyholder stops paying the premiums or surrenders the policy.