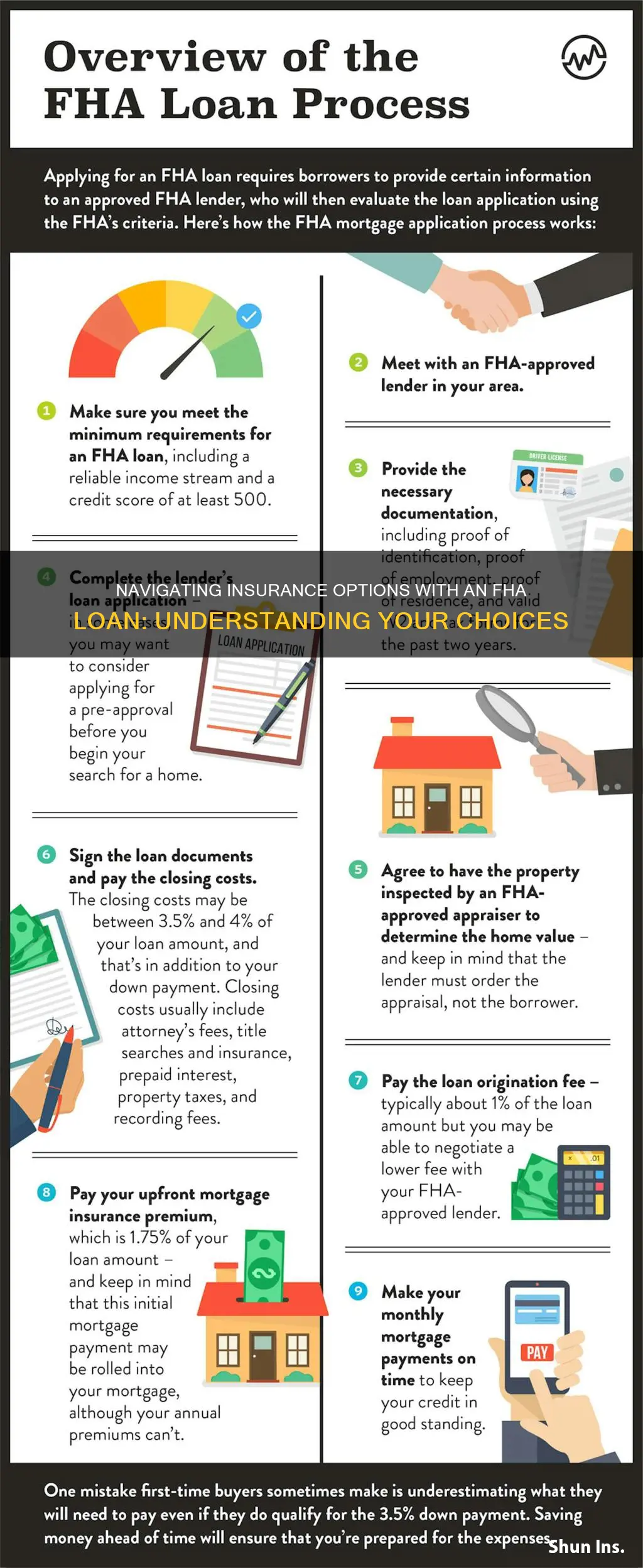

FHA loans are a popular option for homebuyers, especially first-time buyers, as they offer competitive mortgage rates and lenient standards for borrowers, such as lower credit score and down payment requirements. However, one trade-off of FHA loans is the requirement to pay mortgage insurance premiums (MIP), which can add a significant cost to the life of the loan. The good news is that it may be possible to remove or reduce FHA mortgage insurance, depending on factors such as the origination date of the loan, the size of the down payment, and the loan-to-value (LTV) ratio.

There are two main ways to eliminate FHA mortgage insurance: natural lapsing of the insurance or refinancing to a conventional loan. For loans originated after June 3, 2013, MIP will automatically lapse after 11 years if the down payment was at least 10%. For loans originated between January 2001 and June 3, 2013, MIP will lapse when the LTV ratio reaches 78%. For older loans, MIP may be cancelled once the borrower has gained sufficient equity (usually 20%).

If the borrower doesn't qualify for natural lapsing of MIP, refinancing to a conventional loan is an option. This requires meeting certain criteria, such as having a credit score of at least 620, a debt-to-income ratio of no more than 50%, and having built at least 20% equity in the home. It's important to consider the costs and benefits of refinancing, as it may result in higher interest rates or additional closing costs.

In summary, while FHA loans offer attractive features for homebuyers, the requirement to pay MIP can be a significant ongoing cost. Borrowers have options to remove or reduce MIP, but it's important to carefully evaluate eligibility and the potential benefits and drawbacks of each option.

Explore related products

What You'll Learn

![]()

Cancelling FHA mortgage insurance

The Federal Housing Administration (FHA) insures loans for borrowers who may not qualify for traditional mortgage loans. This insurance protects lenders from losing money if the borrower defaults on the loan.

FHA loans require two types of mortgage insurance premiums (MIP): an upfront premium and an annual premium. The upfront premium is typically 1.75% of the total loan amount, and the annual premium is typically 0.85% of the loan balance. These premiums can add thousands of dollars to the cost of the loan over time.

- Check your eligibility: The ability to cancel FHA mortgage insurance depends on the origination date of the loan and the size of the down payment. Loans originated between July 1991 and December 2000 are not eligible for cancellation. For loans originated between January 2001 and June 3, 2013, the annual MIP will be cancelled when the loan-to-value ratio (LTV) reaches 78%. For loans originated after June 3, 2013, a down payment of at least 10% is required for MIP to be cancelled after 11 years.

- Refinance to a conventional loan: If you have at least 20% equity in your home, you may be able to refinance your FHA loan to a conventional loan, which does not require mortgage insurance if the LTV is 80% or less. However, you will need to meet the lender's minimum credit score and debt-to-income ratio requirements.

- Wait for MIP to expire: If you made a down payment of at least 10% on a loan originated after June 3, 2013, your MIP will expire after 11 years of on-time payments.

- Refinance to a different government loan: If you are a current or former member of the military, you may be eligible for a VA loan, which does not require monthly mortgage insurance. Another option is a USDA loan, which does not require a down payment and has a lower monthly insurance premium than FHA loans.

- Reduce your MIP: If you are not eligible to cancel your MIP, you may be able to reduce it by refinancing to another FHA loan at a lower LTV ratio. The U.S. Department of Housing and Urban Development (HUD), which oversees FHA loans, lowered the MIP rates in 2023.

It is important to carefully consider the costs and benefits of each option before making a decision. Cancelling or reducing FHA mortgage insurance can lower your monthly payments, but it may also require you to pay closing costs or accept a higher interest rate.

The Intricacies of Insurance Endorsements: Unraveling the Added Layer of Protection

You may want to see also

Explore related products

![]()

FHA mortgage insurance removal eligibility

If your FHA loan was taken out after the year 2000, you may be able to cancel your FHA mortgage insurance in certain cases. If your loan was taken out before 2000, you’ll continue to pay the premiums in most cases.

Loan origination date

If your origination date was between July 1991 and December 2000, you can’t cancel your FHA mortgage insurance premiums. You’ll need to keep paying them for the life of the loan, unless you refinance.

If your origination date was between January 2001 and June 3, 2013, your MIP will be canceled when you reach a loan-to-value ratio (LTV) of 78%.

If your origination date was after June 3, 2013, and you made a down payment of at least 10%, your MIP will be canceled after 11 years. For down payments of less than 10%, you’ll pay MIPs for the life of the loan, unless you refinance.

Down payment amount

If you put at least 10% down on an FHA loan, your MIP will go away on its own after you’ve made payments for 11 years.

If you closed your FHA loan before June 3, 2013, your annual MIP will be canceled once you’ve paid your loan down to 78% of your home’s value.

If you put less than 10% down on a loan closed on or after June 3, 2013, your MIP will remain for the life of the loan. You’d need to refinance or pay off the loan completely to stop paying MIP.

Other options

If you’re not eligible to remove MIP based on the loan origination date and down payment amount, you may still be able to reduce your FHA mortgage insurance costs. FHA MIP rates have decreased since 2015, so you may be able to get a lower rate by refinancing.

Another option is to refinance your FHA loan into a conventional loan or a government-backed loan such as a VA or USDA loan. By refinancing into a conventional loan, you can eliminate MIP and potentially get a lower interest rate. However, you’ll need to meet the eligibility requirements for a conventional loan, which include a higher credit score and a higher down payment compared to an FHA loan.

The Hidden Hazards of Adverse Selection: Unraveling Insurance's Dark Secret

You may want to see also

Explore related products

![Loans on Life Insurance Policies, by John M. Taylor, President the Connecticut Mutual Life Insurance Company 1913 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

Refinancing to a conventional loan

Homeowners who refinance from an FHA loan to a conventional home loan may reap financial benefits, such as lower monthly payments and savings. However, there are some important steps to take and requirements to consider before making the switch.

Step 1: Research rates and prepare documentation

Before switching from an FHA loan to a conventional loan, it is important to research different lenders and compare their rates and fees for refinancing. It is also a good idea to research different types of refinancing, such as a cash-out refinance or a rate-and-term refinance. Gather important financial documents, such as pay stubs, tax forms, and bank statements, to show the loan officer that you have been responsible with your existing loan.

Step 2: Meet refinancing requirements

The specific requirements to refinance to a conventional loan may vary depending on the lender, but in general, a credit score of at least 620, a debt-to-income ratio of no more than 50%, homeowners insurance verification, and an appraisal of the home will be needed.

Step 3: Submit an application and go through underwriting

Once the basic eligibility qualifications have been met and the necessary documentation has been submitted, the next step is to go through the underwriting process. This involves a thorough evaluation of the applicant's financial status and the property being refinanced.

Step 4: Finish the closing process

The final step is to complete the refinancing closing, which involves reviewing and signing various loan documents and other pertinent paperwork related to the new conventional loan.

Pros of refinancing to a conventional loan

Refinancing from an FHA to a conventional loan can offer financial benefits such as:

- The ability to get rid of mortgage insurance, which is required for FHA loans and can add a significant cost to monthly payments.

- Lower interest rates, which can result in significant savings over the life of the loan.

- The ability to tap into home equity to fund other expenses.

- Higher loan limits, allowing borrowers to take out larger loan amounts.

Cons of refinancing to a conventional loan

There are also some potential drawbacks to consider when refinancing from an FHA to a conventional loan:

- Closing costs, which can range from 2% to 6% of the loan balance, can be significant and may outweigh the savings gained from refinancing.

- The repeat loan approval process can be time-consuming and involve a lot of paperwork.

- If the borrower has less than 20% equity in the property, they may still need to pay private mortgage insurance (PMI) on a conventional loan, which can be more expensive than FHA mortgage insurance.

Prescribed Medication Privacy: Understanding Insurance Bills

You may want to see also

Explore related products

![]()

FHA Streamline Refinance

The FHA Streamline Refinance is a mortgage refinancing program specifically designed for homeowners with existing FHA mortgages. It allows borrowers to refinance an existing FHA-insured mortgage requiring limited borrower credit documentation and underwriting. The basic requirements of a streamline refinance are:

- The mortgage to be refinanced must already be FHA-insured.

- The mortgage to be refinanced must be current (not delinquent).

- The refinance must result in a net tangible benefit to the borrower.

- Cash in excess of $500 may not be taken out on mortgages.

- Investment properties are only eligible for FHA insurance if the borrower is a HUD-approved nonprofit borrower, a state or local government agency, or an instrumentality of the government.

There are two types of FHA Streamline Refinance loans: credit-qualifying and non-credit qualifying. The latter doesn't typically require an appraisal, credit check, or income verification. However, the lender you work with might still pull your credit report. The non-credit qualifying option is the most common.

The FHA Streamline Refinance has pros and cons. On the positive side, it offers a potential lower monthly payment, access to today's lower interest rates, no home appraisal, and faster closing. On the negative side, it requires closing costs, limited cash back, and mortgage insurance requirements.

To be eligible for an FHA Streamline Refinance, you must already have an FHA-insured mortgage, receive a net tangible benefit, apply after a waiting period, and have a history of on-time payments. You must also pay mortgage insurance premiums.

Maximizing Vision Insurance Benefits for Eyeglasses

You may want to see also

Explore related products

![]()

Comparing FHA and conventional loans

The Federal Housing Administration (FHA) loan is a mortgage option that is ideal for buyers looking for low down payment options, flexible income, and credit guidelines. On the other hand, conventional loans are not insured or guaranteed by government agencies and usually require higher credit scores and down payments than FHA loans. Here is a detailed comparison of the two loan types:

Credit Score Requirements:

FHA loans are suitable for borrowers with lower credit scores, with a minimum score requirement of 500, while conventional loans typically require a credit score of at least 620.

Down Payment Requirements:

FHA loans offer flexible down payment options, with a minimum requirement of 3.5% for credit scores above 580 and 10% for scores between 500 and 579. In contrast, conventional loans usually require a minimum down payment of 3%, but this may vary depending on the lender.

Debt-to-Income Ratio (DTI):

FHA loans are more lenient when it comes to DTI, with a maximum DTI of 43% to 57%, while conventional loans prefer borrowers with DTIs of 36% or less, and typically not above 50%.

Mortgage Insurance:

FHA loans require mortgage insurance premiums (MIP), which include an upfront payment of 1.75% of the loan amount and monthly payments. The monthly MIP varies depending on the loan term, down payment, and other factors. Conventional loans require private mortgage insurance (PMI) if the down payment is less than 20%, but it can be removed once the borrower reaches 20% equity.

Loan Limits:

Both FHA and conventional loans have limits on the maximum loan amount, which vary by county and are typically adjusted annually. FHA loan limits tend to be lower than conventional loan limits.

Property Standards:

FHA loans can only be used for primary residences and have stricter appraisal standards. In contrast, conventional loans can be used for various property types, including private homes, investment properties, and vacation houses.

Interest Rates:

FHA loans often offer competitive and flexible interest rates, while conventional loan rates depend on the borrower's qualifications, such as credit score and occupancy.

Refinancing Options:

FHA loans offer the FHA Streamline Program, which allows borrowers to refinance without a complete credit check or income verification. Conventional loans also offer refinancing options, such as rate-and-term refinances, but they typically require an appraisal.

Occupancy Options:

FHA loans can only be used for primary residences, while conventional loans provide more flexibility, allowing borrowers to purchase a secondary home or investment property.

In summary, FHA loans are generally more accessible to borrowers with lower credit scores, smaller down payments, and higher DTIs. On the other hand, conventional loans may offer more favourable terms for borrowers with strong credit profiles and larger down payments, providing more flexibility in terms of property usage and refinancing options. Ultimately, the best loan option depends on the borrower's financial situation and goals.

COBRA Coverage: Understanding Your Insurance Continuation Rights

You may want to see also

Frequently asked questions

The ability to cancel your FHA mortgage insurance premium depends on your loan origination date and the size of your down payment. If your FHA loan was taken out after 2000, you may be able to cancel your FHA mortgage insurance in certain cases. If your loan was taken out before 2000, you will likely continue to pay the premiums. You can cancel FHA MIP by meeting the eligibility criteria or refinancing.

A Federal Housing Administration-backed loan requires an upfront premium, or fee, of 1.75% of the loan amount. You can include this premium in your FHA closing costs or roll it into your loan amount, which will increase your monthly payments slightly. In addition to the upfront premium, you’ll pay a monthly mortgage insurance premium (MIP) that is added to your mortgage payments.

To get rid of FHA MIP with a mortgage refinance, you can apply with a mortgage lender and let your loan officer know that you want to refinance into a conventional loan and cancel FHA MIP. You can also add the closing costs to your new loan balance to avoid paying them immediately, but this will increase your overall loan amount.